Micron (MU) Stock Surges After Earnings: Did AI Memory Demand Just Extend the Semiconductor Super Cycle?

2026/06/25 14:10:00

Introduction

One earnings report rarely changes sentiment across multiple asset classes in a single night — but Micron’s latest quarterly results appeared to do exactly that. Following the release, MU share price surged sharply in after-hours trading, while storage peers also rallied and even risk assets showed signs of recovering sentiment.

The reason was not simply that Micron beat expectations. The reported numbers suggested something larger: AI infrastructure demand may still be accelerating, and memory chips could be entering a stronger and longer cycle than many investors expected.

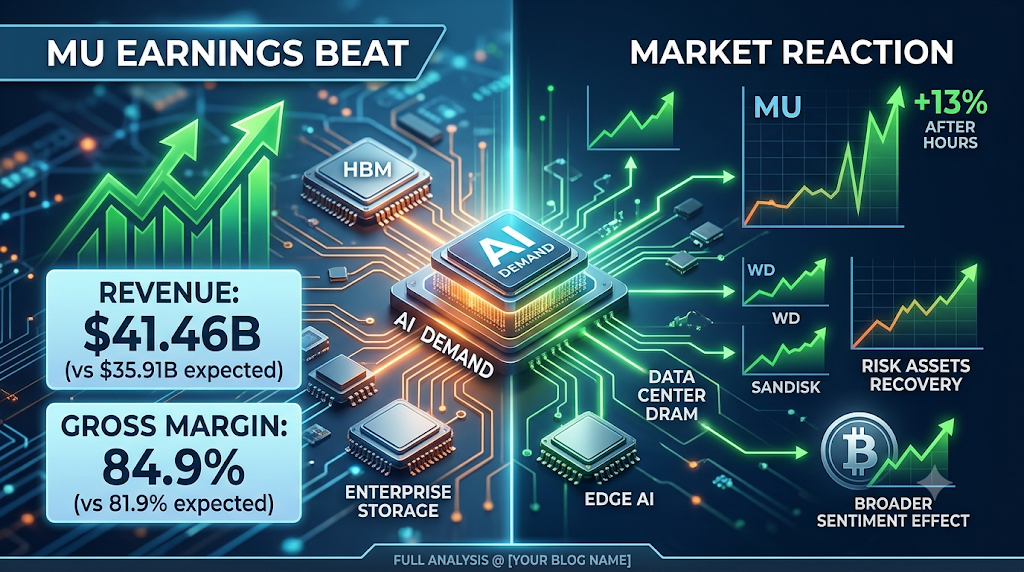

Based on the company’s reported figures, adjusted gross margin reached 84.9% versus market expectations of 81.9%, while quarterly revenue reached $41.46 billion compared with expectations of $35.91 billion. Management further indicated margins could continue expanding next quarter.

The market reaction raises a bigger question: Is Micron leading another leg of the US equity rally, or are investors witnessing the peak phase of the AI memory boom?

Micron’s earnings triggered a broad market re-rating because investors interpreted the report as evidence that AI infrastructure spending remains stronger than expected.

The immediate market response was aggressive. MU rose roughly 13% in after-hours trading following the release. At the same time, memory and storage-related names including Western Digital and SanDisk also advanced by more than 10%.

This reaction reflected more than short-term enthusiasm. Investors had spent months debating whether AI spending had begun slowing after enormous capital expenditures from cloud providers and AI developers. Micron’s results challenged that concern directly.

The market focused on three numbers:

| Metric | Reported | Market Expectation |

| Adjusted Gross Margin | 84.90% | 81.90% |

| Revenue | $41.46B | $35.91B |

| Next Quarter Margin Outlook | Up to 86% | Not expected |

The magnitude of the beat mattered because semiconductor cycles are usually judged not by revenue alone, but by pricing power and profitability.

Revenue can rise temporarily through inventory normalization. Margins expanding at the same time often indicate genuine supply-demand imbalance. That distinction became the central reason behind MU’s rally.

Why Did Investors Focus So Much on Gross Margin?

The most important signal from Micron’s earnings was not revenue — it was margin expansion. Gross margin of 84.9% suggested unusually strong pricing conditions inside the memory market.

For context, investors often compare semiconductor gross margins because they reveal who controls pricing and who is absorbing cost pressure. The market narrative following the report emphasized that Micron’s reported margin exceeded the most recent quarterly margin reported by Nvidia at approximately 75%.

That comparison attracted attention because Nvidia has become the benchmark for AI monetization. When a memory supplier begins approaching or exceeding those economics, investors naturally ask whether the value chain is expanding beyond compute chips.

High margins usually imply one or more of the following:

-

Demand growth exceeds production expansion.

-

Customers prioritize supply availability over pricing.

-

Product mix shifts toward premium products.

-

Industry capacity remains disciplined.

In Micron’s case, investors interpreted the results as evidence that AI memory demand remains supply constrained. That is why the stock move quickly spilled into adjacent sectors.

Is AI Creating a New Memory Chip Super Cycle?

The market increasingly believes AI is creating a structural memory expansion cycle rather than a traditional semiconductor rebound. Historically, memory businesses have been highly cyclical. Periods of high prices encouraged producers to add supply aggressively, eventually leading to oversupply and margin collapse.

This time, investors argue the structure looks different. AI workloads consume dramatically larger memory resources than conventional computing. Training large models requires massive bandwidth. Inference at scale also requires fast memory access and higher density configurations. As AI adoption expands, demand may rise across multiple layers simultaneously:

High-Bandwidth Memory

HBM became one of the fastest-growing semiconductor categories because advanced AI accelerators require massive data throughput.

Data Center DRAM

AI servers consume significantly more memory per rack than traditional cloud deployments.

Enterprise Storage

Inference workloads increasingly generate persistent storage requirements.

Edge AI Devices

Consumer hardware and enterprise devices are beginning to require more local memory resources. Micron’s results reinforced the argument that AI demand is no longer isolated to GPU vendors.

Instead, the entire infrastructure stack may be participating. That interpretation explains why storage-related equities moved together.

Did Micron’s Earnings Affect Crypto Markets Too?

Micron’s earnings appeared to influence broader risk sentiment — including crypto. Following the release, market participants observed Bitcoin recovering rapidly after briefly falling toward the $59,000 area before rebounding toward approximately $61,000.

This reaction should not be interpreted as Micron directly driving Bitcoin prices. Instead, both assets likely responded to changing expectations around growth, liquidity, and AI-related optimism. Crypto markets increasingly trade alongside technology risk assets because institutional capital now overlaps across both sectors.

When investors become more confident in growth sectors, capital often rotates back into higher-beta assets.

Can Micron Continue Driving the US Stock Rally?

Micron alone cannot sustain a market rally indefinitely — but it can extend momentum if earnings validate AI investment returns. The market now faces a difficult question.

If memory profitability continues expanding, investors may conclude that AI spending remains in an early monetization phase. That would support higher valuations across technology. However, semiconductor leadership historically weakens when one of three conditions appears:

Demand Normalization

Customers begin delaying purchases after rapid deployment periods.

Capacity Expansion

Competitors increase supply aggressively.

Multiple Compression

Strong earnings become insufficient to justify already elevated valuations.

For now, Micron’s guidance suggests supply constraints may still exist. Management’s indication that gross margin could potentially rise further suggests pricing pressure has not disappeared. That is unusual late-cycle behavior.

Investors therefore increasingly debate whether this is not simply a semiconductor cycle but an infrastructure cycle tied to AI adoption. If correct, the duration may be longer than historical memory booms.

How Long Could the Memory Super Cycle Last?

The answer depends less on Micron and more on AI investment durability. The bullish case argues that AI remains in the infrastructure buildout phase.

If enterprises continue deploying AI systems globally, demand for memory and storage could remain elevated for years. Supporters of this view point to several structural drivers:

-

AI training capacity still expanding.

-

Inference deployment accelerating.

-

Enterprise adoption remaining early.

-

Hardware refresh cycles beginning.

The bearish case is equally important. History shows semiconductor shortages eventually attract supply.

Margins at extreme levels rarely persist indefinitely. Once supply catches demand, pricing power typically weakens.

The most realistic scenario may sit between those extremes. Rather than expecting perpetual margin expansion, investors may watch for slowing acceleration.

If margins stabilize at elevated levels while volumes continue growing, the cycle could remain healthy even without further explosive upside. The market’s current challenge is distinguishing structural demand from temporary scarcity.

What Risks Could End the Bullish Narrative?

The largest risk is not weaker earnings — it is expectations becoming too optimistic. When markets price perfection, even strong results can disappoint. Several risks deserve monitoring:

AI Spending Efficiency

Customers may eventually demand measurable returns from infrastructure spending.

Competitive Capacity

Additional memory production could reduce pricing leverage.

Macro Conditions

Higher rates or slower economic growth could reduce technology investment.

Inventory Rebalancing

Temporary shortages may normalize faster than expected. Investors should also remember that semiconductor cycles historically reverse before consensus expectations change.

That does not mean the thesis is broken. It means timing matters. Strong fundamentals and strong stock performance do not always move together.

Should You Trade Semiconductor and AI Momentum Themes on KuCoin?

Investors looking to position around technology momentum increasingly monitor both traditional equities and digital asset markets together. Micron’s earnings highlighted how developments in one sector can rapidly influence sentiment across others.

KuCoin provides access to a broad range of not only crypto markets, but also stock markets, including MU stock. Now users can also participate in KuCoin's Campaign of Trading US Stock Perps:

-

After complete simple trading missions, users may unlock 100,000 USDT prize pool rewards in TSLA, AAPL, or GOOGL.

Conclusion

Micron’s earnings became more than a company-specific event because investors interpreted the results as evidence that AI infrastructure demand remains unusually strong. The reported revenue and gross margin figures suggested a market environment where pricing power continues improving rather than normalizing. That challenged expectations that AI spending was beginning to cool.

The reaction spread quickly across semiconductors, storage companies, and broader risk assets. MU rallied sharply, peers followed, and market participants even connected the event to improved sentiment in crypto markets.

The bigger question now is no longer whether AI demand exists. The real debate is whether memory chips have entered a longer-duration super cycle or whether current profitability reflects temporary supply constraints.

For investors and traders, the next few quarters may matter more than the headline rally itself. If margins remain elevated while demand continues expanding, Micron may become one of the clearest indicators of whether the AI investment cycle still has room to run.

FAQs

1. Why did MU stock rise more than other semiconductor stocks?

Investors viewed Micron’s earnings as evidence of improving industry economics rather than company-specific execution, which increased optimism across the sector.

2. Does high gross margin automatically mean a stock will continue rising?

Not necessarily. High margins indicate strong current conditions but do not guarantee future returns because expectations and valuation also matter.

3. Why are memory chips important for AI?

AI systems require large amounts of memory bandwidth and storage to train and deploy models efficiently.