Why Chip Stocks Are Pulling Back in July 2026 But the AI Cycle Is Far From Over?

2026/07/09 11:24:00

Introduction

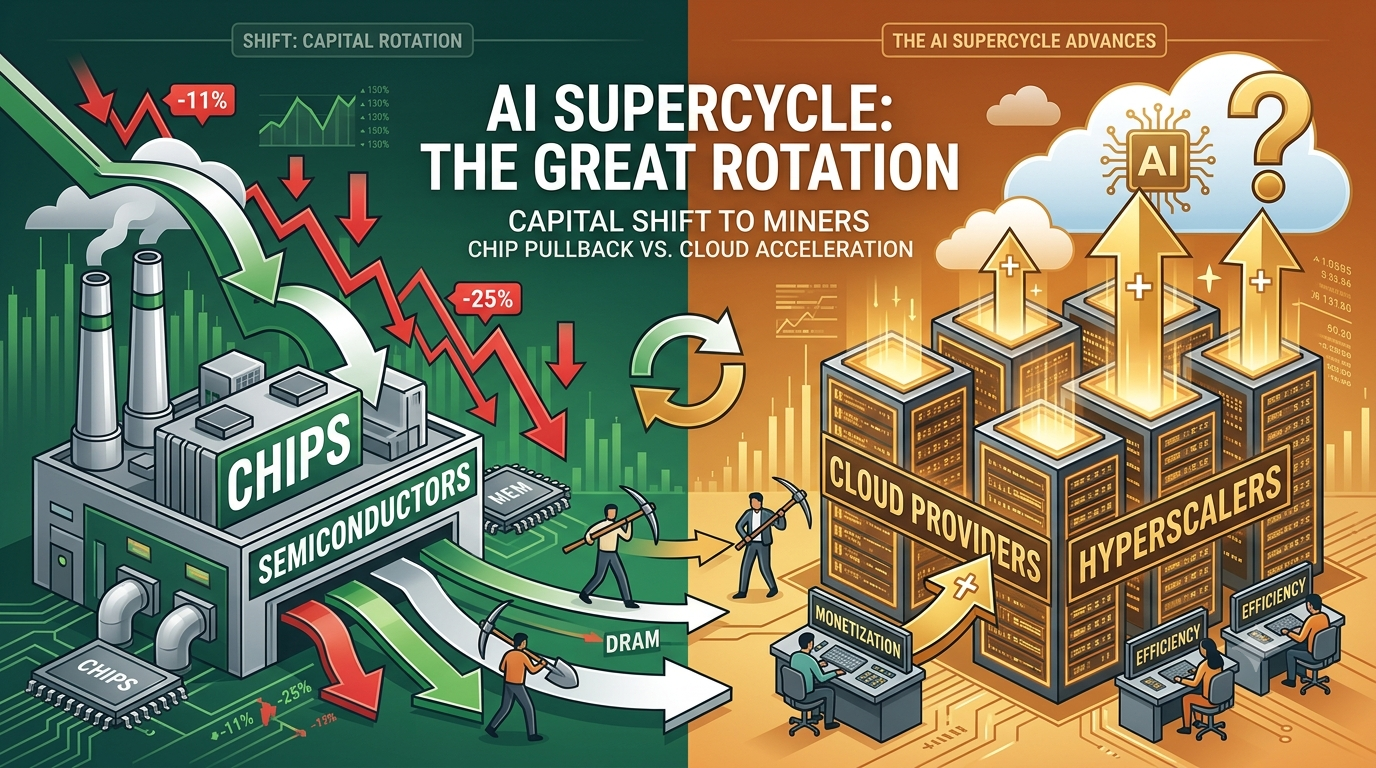

Chip stocks have faced sharp pullbacks in recent weeks, with the Philadelphia Semiconductor Index dropping over 11% in two weeks and memory-focused ETFs like DRAM retreating around 25% from June 22 highs. Yet the AI supercycle is not ending—it is rotating. Capital is shifting from “shovel sellers” (chipmakers) to “miners” (hyperscalers and cloud providers) as the industry digests massive prior investments while underlying AI demand accelerates.

Meta’s early July announcement to sell excess AI computing power acted as a catalyst, signaling hyperscalers are optimizing capacity rather than endlessly expanding. Samsung’s record Q2 2026 earnings followed, yet shares fell nearly 7% on cycle-top fears. Micron delivered explosive Q3 results with $41.46 billion revenue—up 346% year-over-year—but still saw post-earnings pressure.

This correction reflects a healthy rate-of-change slowdown and profit rotation within a multi-year AI capital expenditure (capex) cycle that analysts expect to extend through 2027–2028. JPMorgan calls the dip a buying opportunity, citing limited new supply before 2028.

What’s Driving the Recent Chip Stock Pullback?

The pullback stems from digestion signals after years of aggressive hyperscaler spending. Meta’s plan to monetize excess compute via a new cloud business highlights that even leading AI investors are pausing raw expansion to improve returns.

Samsung’s preliminary Q2 results showed operating profit surging 19-fold to about 89.4 trillion won ($58.4 billion) on AI-driven memory demand, yet shares slumped as investors worried about peak-cycle dynamics and heavy future capex. Micron’s blowout Q3—$41.46 billion revenue and $50 billion guidance—triggered “sell the news” reactions typical at perceived tops.

Broader market data confirms the move: SMH fell about 12% in two weeks, while memory stocks faced concentrated selling. High valuations, stretched positioning, and rotation out of 2026 winners amplified the decline.

However, these are tactical signals, not structural breaks. AI infrastructure demand remains insatiable, with HBM sold out through 2026 and prepayments supporting visibility.

Meta’s Excess Capacity Sale: Digestion, Not Demand Destruction

Meta’s move to sell surplus AI compute marks a logical evolution. After rapid data center buildouts, the company now seeks returns on overbuilt capacity by competing with AWS, Azure, and Google Cloud.

This does not indicate weakening AI appetite. Instead, it shows hyperscalers shifting from pure capex acceleration to efficiency and monetization. Similar moves, like xAI-related plans, reinforce that winners will optimize existing assets. Chip demand ties directly to cloud capex willingness—current actions suggest optimization within an ongoing buildout, not cancellation.

Samsung and Micron Earnings Highlight Cycle Strength

Samsung’s Q2 guidance delivered record profits driven by DRAM and NAND pricing strength from AI servers. Revenue roughly doubled year-over-year, with memory fundamentals intact.

Micron’s fiscal Q3 2026 results were even stronger: $41.46 billion revenue (346% YoY) and data center revenue exceeding $25 billion quarterly. HBM remains capacity-constrained, with strong guidance underscoring sustained demand.

“Sell the news” reactions reflect profit-taking and rotation fears rather than weak fundamentals. Analysts note AI memory demand supports margins and growth into 2027+, with new supply limited.

Morgan Stanley’s Michael Wilson on Semiconductor Rotation

Morgan Stanley’s Mike Wilson explicitly advised reducing semiconductor exposure in favor of hyperscalers. He views this as a “rate of change” peak within the capex cycle—not its end. Profits are rotating from chipmakers to cloud operators monetizing AI.

This aligns with market action: Chinese AI-related stocks like Alibaba surged over 11% amid U.S. chip weakness, reflecting global rotation and intensifying U.S.-China AI competition.

Why AI Demand and Capex Remain Robust Long-Term

Multiple factors support continuation:

-

Supply Constraints: HBM sold out through 2026; meaningful new capacity unlikely before 2028.

-

Hyperscaler Commitments: Microsoft, Google, Amazon, and others maintain massive AI infrastructure plans despite near-term optimization.

-

Geopolitical Acceleration: U.S.-China AI rivalry drives parallel investments, boosting global demand.

-

Monetization Phase: As models deploy, cloud providers generate revenue to fund further spend, creating a self-reinforcing loop.

JPMorgan and others see the AI-driven chip cycle lasting strongly through 2027.

Should You Trade AI Exposure on KuCoin?

KuCoin offers diverse ways to participate in the AI ecosystem beyond traditional stocks. Traders can access crypto assets tied to AI infrastructure, decentralized compute, and blockchain-AI intersections that benefit from the same demand drivers.

KuCoin provides access to a broad range of not only crypto markets, but also stock markets. Now users can also participate in KuCoin's Campaign of Trading US Stock Perps:

-

After complete simple trading missions, users may unlock 100,000 USDT prize pool rewards in TSLA, AAPL, or GOOGL.

Conclusion

The 2026 chip stock pullback represents a healthy reset and capital rotation within the AI supercycle, not its demise. Triggers like Meta’s capacity sales and strong-but-priced-in earnings from Samsung and Micron highlight digestion after explosive growth. Yet core drivers—constrained supply, insatiable AI demand, and multi-year capex—remain firmly intact.

Michael Wilson’s call for rotation to hyperscalers and positive outlooks from JPMorgan underscore that this is a stage shift, not an end. Global competition, particularly U.S.-China dynamics, further bolsters long-term prospects.

Investors should view volatility as opportunity. The AI cycle’s next leg favors efficient monetizers and sustained infrastructure builders. With limited new supply through 2028, the structural bull case for semiconductors and AI remains compelling despite near-term noise. Position thoughtfully, focus on fundamentals, and recognize that corrections within powerful secular trends often create the best entry points for long-term gains.

FAQs

Is the AI chip boom over after the 2026 pullback?

No. The pullback reflects rotation and digestion, not end of demand. Analysts project the cycle continuing strongly through 2027–2028 with limited new supply.

Why did Samsung and Micron stocks fall despite record earnings?

“Sell the news” reactions and rotation fears triggered selling. Fundamentals—surging AI memory demand and sold-out capacity—remain robust.

What does Meta selling compute mean for chip demand?

It signals optimization and monetization of existing assets, not reduced spending. Hyperscalers continue AI buildouts while improving returns.

Should investors buy the chip dip in 2026?

Many analysts, including JPMorgan, view it as a buying opportunity given strong long-term AI drivers and supply constraints.

How does U.S.-China AI competition affect the cycle?

It accelerates parallel investments globally, supporting demand for chips and related technologies beyond U.S. hyperscalers.