KuCoin Ventures Weekly Report: SpaceX Mega IPO Triggers RWA Stress Test, Resonating with AI Capital Anxiety and Cross-Asset Deleveraging

2026/06/15 18:29:00

1. Weekly Market Highlights

SpaceX Completes the Largest IPO in History, Putting Tokenized Equity Products Through Their First Real Stress Test

Last week, SpaceX’s Nasdaq listing became a shared focal point for traditional capital markets and the crypto RWA narrative. As a mega-cap technology asset that had long remained in the private market, with relatively high barriers for public investors, SpaceX combines several powerful narratives at once: space infrastructure, Starlink’s satellite internet network, Elon Musk’s personal brand, and high-growth technology exposure. Its IPO therefore drew immediate attention from global capital. The company priced its shares at $135, raising $75 billion. On its first day of trading, the stock opened at $150, briefly touched around $176 intraday, and closed at $160.95, pushing its market capitalization above $2 trillion. For the broader market, this was not only a landmark mega-cap technology IPO, but also a symbolic event driven by recovering risk appetite, the public-market opening of high-quality private assets, and retail investor FOMO.

Data Source: Yahoo Finance

For the crypto industry, the core significance of SpaceX’s IPO lies in how crypto trading platforms and wallet front ends attempted to turn a major traditional finance event into an asset entry point accessible to crypto-native users. SpaceX did not exclude retail participation this time, and traditional brokerages also opened subscription channels to U.S. retail investors. However, actual participation still depended on account eligibility, regional compliance, brokerage thresholds, and final allocation results, while certain jurisdictions were excluded due to compliance restrictions. Therefore, what crypto platforms offered was not a complete replacement for the traditional IPO distribution system, but rather a repackaging of a highly demanded equity exposure—previously constrained by geography, account infrastructure, and market hours—into a front-end product more understandable and usable for global crypto users.

Crypto market participation mainly unfolded across two directions. The first was Pre-IPO / IPO Access subscription. Platforms such as Kraken, Bybit, Binance Wallet, Bitget Wallet, and MEXC primarily opened subscription or indication-of-interest channels around SPCXx launched via xStocks. Users locked USDC or USDT before the IPO and submitted subscription interest at a price close to the IPO price, with an additional spread or underwriting service fee of around 5%. Whether users ultimately received allocation depended on upstream underwriters and the supply of underlying shares. Gate also participated in the SpaceX subscription through Direct IPO Access and connected IPO allocation with subsequent U.S. equity trading accounts, showing that trading platforms are experimenting with different paths into traditional IPO distribution. The second category was pre-market, perpetual, or other synthetic trading exposure, mainly designed to meet demand for expressing views on SpaceX’s valuation and price volatility before and after the official listing. These products are closer to price discovery and derivatives trading in nature and do not provide actual share delivery. Together, the two categories show that crypto platforms’ participation in SpaceX was not merely about “listing a tokenized stock,” but about capturing a traditional finance hotspot through both IPO Access and trading-oriented exposure.

The real issue exposed by this round of products is that front-end subscription demand can be rapidly amplified by crypto platforms, while the supply of real underlying assets cannot expand at the same pace. Demand for the SpaceX IPO itself was extremely strong. After multiple platforms opened subscription channels at the same time, front-end subscription volume accumulated quickly. However, some platforms ultimately failed to obtain sufficient underlying share allocations, leading Bybit, Binance Wallet, Bitget Wallet, and others to cancel related subscriptions or issue full refunds. In other words, tokenized equity products can lower user participation barriers, improve capital coordination efficiency, and accelerate market attention, but they cannot bypass the core constraints of traditional IPOs: initial allocation of high-quality assets still depends on underwriting systems, custody arrangements, compliance eligibility, and genuine upstream supply.

A deeper issue is that Pre-IPO tokenized products can easily be simplified in users’ minds as “buying SpaceX on-chain,” while their actual structure is not equivalent to directly holding Nasdaq-listed shares. What users submit may only be a subscription indication, with no certainty of final allocation. What they receive may be a tokenized stock or price exposure rather than full shareholder rights. Pre-market and perpetual products are even more oriented toward trading and price discovery and do not provide actual share delivery. Post-listing secondary trading through bStocks or xStocks may become a later extension, but the core stress test had already emerged at the IPO Access stage: users need to clearly distinguish whether they are buying real shares, tokenized certificates, subscription eligibility, or a more derivative-like price exposure.

Overall, the SpaceX IPO served as a two-way validation for crypto RWA and tokenized equities. On one hand, it proved that crypto trading platforms and wallet front ends can quickly capture global financial events, converting cross-border demand that traditional brokerages cannot fully cover into on-chain subscription activity, trading interest, and market discussion. It also shows that RWA user demand is extending beyond low-volatility assets such as U.S. Treasuries and money market funds toward high-attention stocks, Pre-IPO assets, and derivative exposure. On the other hand, it also shows that RWA is not simply about putting an asset’s name on-chain and calling it financial infrastructure. When the underlying asset is scarce and subscription demand surges, supply constraints, allocation rules, refund mechanisms, legal-attribute disclosure, and user expectation management all become critical to whether the product can function properly.

Looking ahead, the SpaceX case may push further segmentation among crypto platforms offering Pre-IPO and tokenized equity products. One group of platforms may continue to strengthen their positioning as front ends for hot asset exposure, focusing on rapid subscription access, pre-market pricing, perpetual contracts, and secondary-market liquidity. Another group will need to move closer to traditional securities infrastructure by building stronger credibility around upstream brokerage partnerships, custody verification, allocation mechanisms, corporate action handling, and compliance disclosure. For the industry, SpaceX does not simply prove that “U.S. equities can be tokenized.” Rather, it reminds the market that when RWA expands from low-volatility assets into high-attention equities, user demand can scale rapidly, but infrastructure weaknesses will scale with it. The next stage of competition in tokenized equities will shift from “who can list the hottest asset first” to “who can deliver asset exposure in a real, stable, and transparent way.”

2. Weekly Selected Market Signals

AI Capital Anxiety Intertwines with Hidden Yen Risks; Crypto Primary Market Accelerates Towards "Institutional-Grade" Concentration

This week, global risk assets experienced a resonance of an "expectation trap and liquidity squeeze." The market is undergoing a profound logic shift: transitioning from purely trading the "profit expectations of the AI industrial revolution" to confronting the severe test of "macro liquidity and capital expenditures."

Data Source: Bloomberg

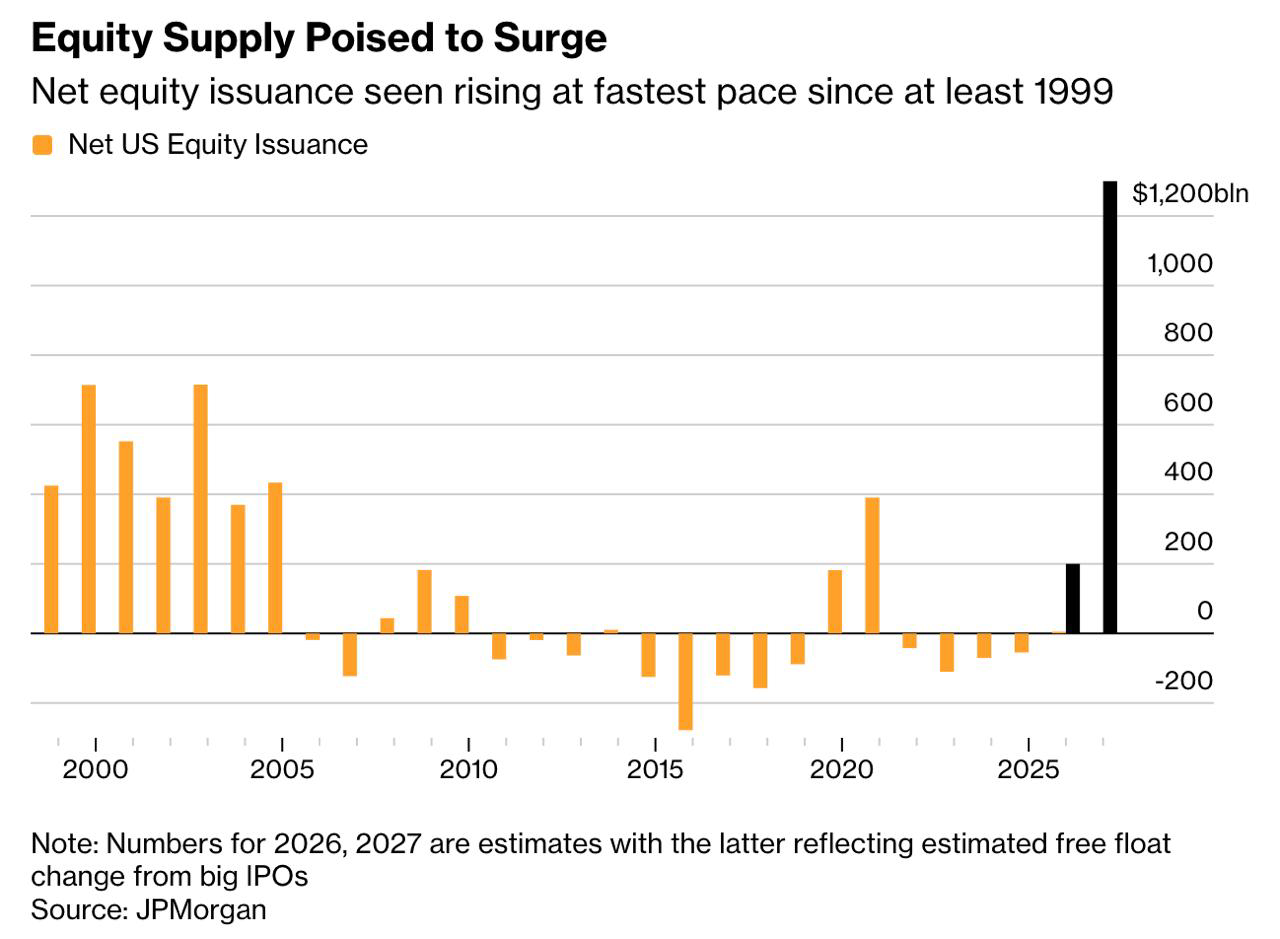

The Era of Mega IPO Liquidity Siphoning and "Equitization": Marked by SpaceX's record-breaking $75 billion IPO on June 12 (surging 19% on its first day to reach a $2.1 trillion valuation), tech giants are ending the decade-long era of US stock "de-equitization" (buybacks and shrinkage). To fund the astronomical spending on AI infrastructure, Wall Street expects up to $1.5 trillion in new stock supply to flood the market over the next two years (with OpenAI and Anthropic following suit). This shatters the original supply-demand balance of the US stock market, creating a terrifying liquidity siphon effect in the short term on all risk assets, including Asia-Pacific equities and the crypto market.

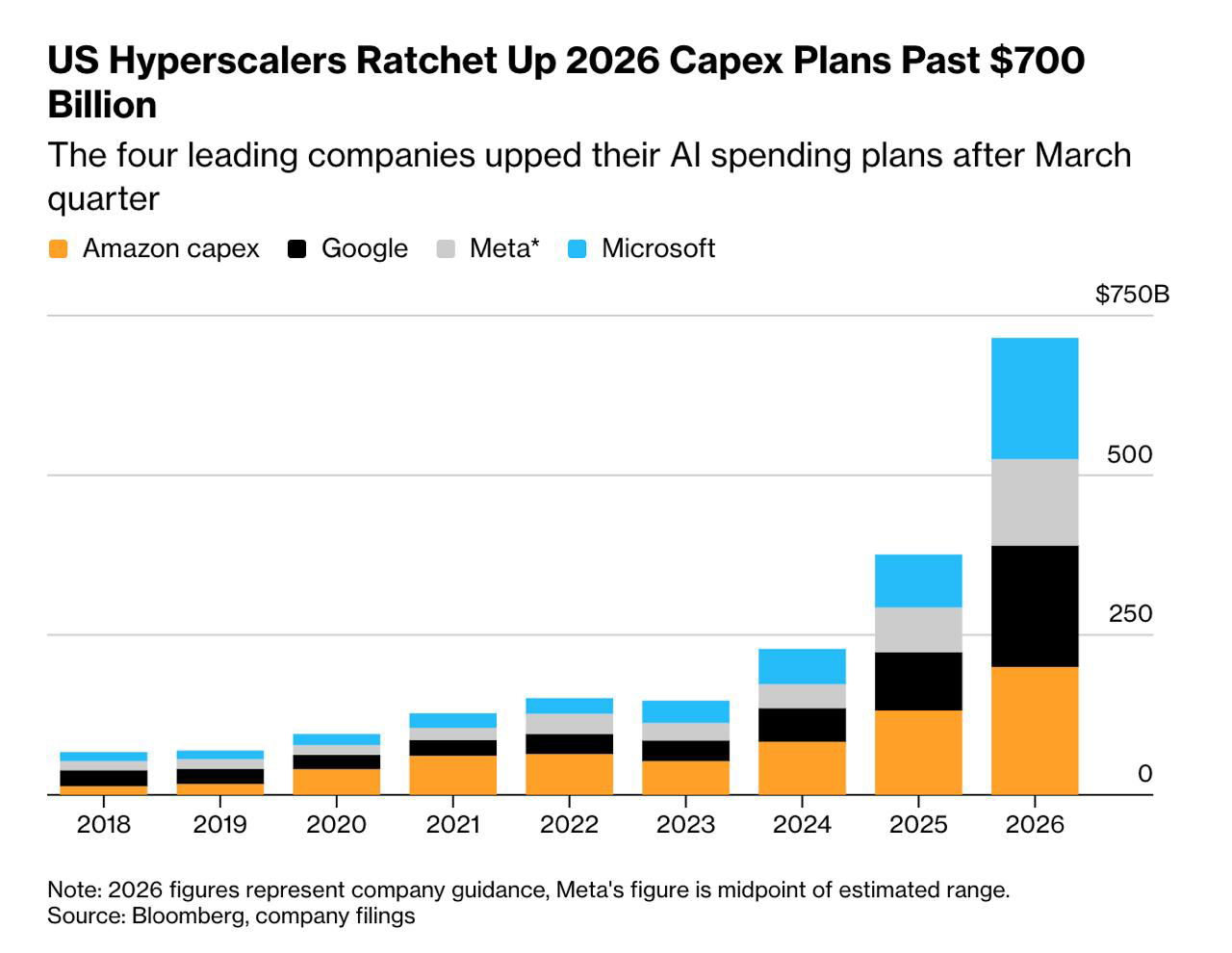

Another core market contradiction is that tolerance for AI giants' capital expenditures (CapEx) is running out. Take Meta, for example: its CapEx now accounts for 35% of total revenue, far exceeding Google's 26%, yet its computing power is primarily used to optimize internal recommendation algorithms, lacking an independent monetization outlet. Oracle's post-earnings plunge was similarly triggered by exorbitant CapEx. As long as the timeline for AI monetization remains unclear, sky-high capital expenditures will be repriced by the market from "growth profits" to a "risk premium."

Examining the frenzy surrounding companies like SpaceX and OpenAI through a crypto lens reveals striking similarities to the defining characteristics of former "Tier-1" crypto projects—"high concept, high expectations, low float, and high fully diluted valuation." SpaceX actually sold less than 5% of its equity in this IPO. Under the sexy narrative of "disrupting humanity" and an extremely dry float structure, bulls easily created a trillion-dollar market cap illusion. However, the gravity of capital markets never fails; ultra-high valuations propped up by "price-to-dream ratios" will ultimately face mean reversion through actual profits or brutal valuation corrections.

Crypto Front: The Market is Undergoing Cross-Asset "Deleveraging" Washouts and Stabilization

-

Broader Market Bottoms Out and Rebounds, Sentiment Repairs: After experiencing previous selling pressure, Bitcoin briefly dipped below the $60,000 mark early this week. However, driven by easing geopolitical tensions over the weekend (expectations of a US-Iran peace deal) and the smooth landing of the SpaceX IPO, which alleviated fears of a liquidity siphon, risk appetite quickly warmed up. As of June 14, BTC stood above $64,000, rebounding over 8% from its low. Mainstream altcoins like Solana also followed the broader market, showing a single-day recovery.

-

In-Depth Analysis: The Double-Edged Sword of Leverage in "Bitcoin Shadow Stock" MSTR: During this round of plunges, MicroStrategy (MSTR) shares retreated all the way to around $115, getting "halved" compared to last year's peak. MSTR's model of issuing debt to buy coins—creating "coins per share" out of thin air—gives it built-in leverage during uptrends. But during downtrends, it not only faces shrinking Bitcoin asset values but also suffers a double blow from Wall Street "killing the premium" and potential corporate credit rating downgrades. This reminds investors: directly holding spot BTC avoids the non-systemic risks associated with individual stocks.

-

Phase Exhaustion of Corporate Buying Waves: Data shows that, aside from the disturbances of spot ETF fund flows, the pace of active Bitcoin allocation by global corporate treasuries (excluding MSTR) has significantly slowed recently. The drying up of corporate treasury buying has weakened the physical support beneath BTC's price, making the market more reliant on short-term liquidity and macro sentiment drivers.

Data Source: SoSoValue

Looking at ETFs, Outflows Pause and Left-Side Buying Coalesces: As the selling pressure from the SpaceX IPO diminished, ETF demand showed signs of stabilizing. Last Thursday, US spot Bitcoin ETFs saw a single-day total net inflow of $85.85 million, marking the strongest performance since mid-May. Notably, BlackRock's IBIT recorded a net inflow of $57.69 million. Institutional investors' long-term demand to use ETF structures as a hedge against inflation and fiat depreciation remains intact.

Data Source: DeFiLlama

Based on the Latest On-Chain Data: The current stablecoin market as a whole exhibits a "shrinking volume and wait-and-see" posture, but it also reveals a significant divergence in capital structure during this process. The total market cap of stablecoins across the network is currently around $315.058 billion, with a net outflow of approximately $987.79 million (-0.31%) over the past 7 days. Among them, USDT (which holds absolute market dominance at 59.17%) and USDC recorded single-week outflows of -0.24% and -1.10%, respectively. Market panic lingers, and the trading willingness and new purchasing power of on-site funds are experiencing a periodic decline.

Data Source: CME FedWatch Tool

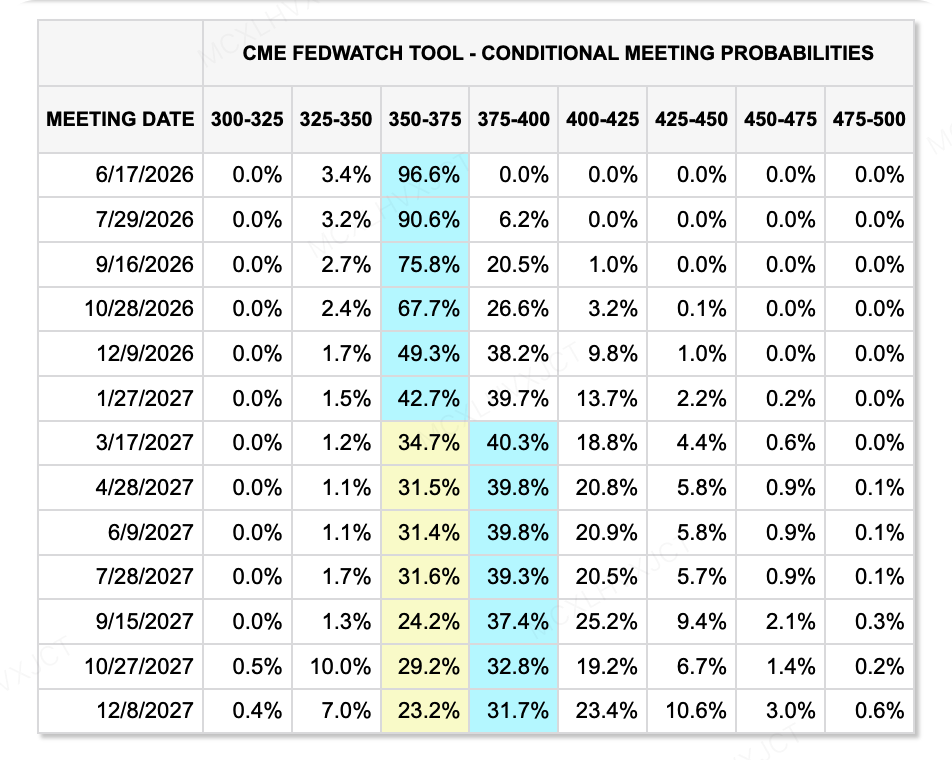

On the Interest Rate Front: Crucial attention must be paid to new Fed Chair Kevin Warsh, who will host his first FOMC meeting this Thursday. Under the high-inflation pressure of May's CPI hitting 4.2%, Kevin will face a dual pincer attack from macro data (stubbornly high inflation) and the White House (the President calling for rate cuts). The market will closely monitor his rhetoric during the press conference: will he bow to inflation data and release a hawkish signal for a "rate hike this year"? Or will he propose a compromise of "using Quantitative Tightening (QT) as a substitute for rate hikes"? Furthermore, rumors about whether he might unprecedentedly cancel the release of the "interest rate dot plot" will be a core suspense affecting far-forward asset pricing.

Other Factors Affecting Global Monetary Liquidity Include:

-

Bleeding-Stop Signal: US-Iran Deal Plunges Oil Prices. The brightest spot on the macro front comes from the expectation of a signed peace agreement between the US and Iran. Brent crude plummeted over 6% to around $87, significantly easing long-term energy inflation pressures. Against the backdrop of CPI breaking 4%, cooling oil prices are crucial to preventing a "1994-style market crash."

-

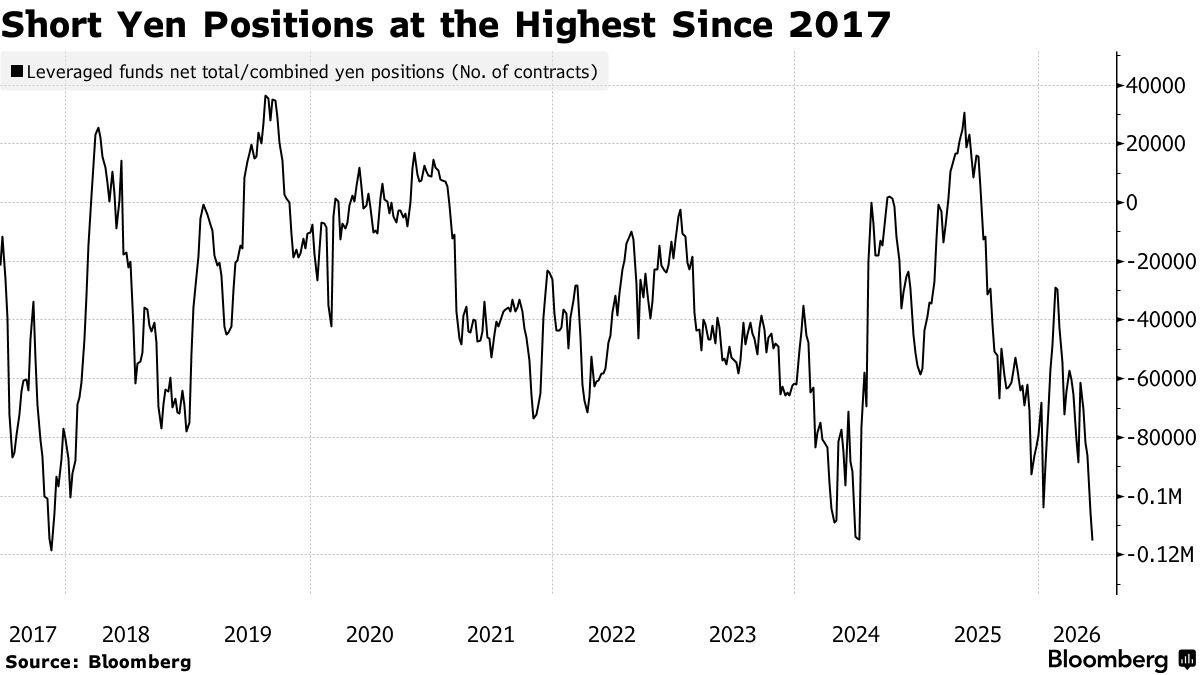

Tail Risk: The Extremely Crowded Yen Carry Trade. Despite the potential rate hike resolution from the Bank of Japan, speculators are still massively shorting the yen. Leveraged funds' net short yen contracts have surged to over 115,000, hitting a nine-year high. Should the BOJ tighten beyond expectations and trigger a violent yen rebound, it could easily recreate a stampede of carry trade unwinding, sending shockwaves through global liquidity.

Major Events to Watch This Week:

This week (June 15 to June 21), global capital markets welcome the most important "Super Central Bank Week" of the year. Interest rate decisions from three major central banks will land densely. Due to inflation pressures triggered by recent Middle East geopolitical situations, the divergence in global monetary policies is further intensifying.

-

June 15 (Mon): NY Empire State Manufacturing Index

-

June 16 (Tue): Release of China's May Macroeconomic Data (Retail Sales, Industrial Value Added, 70-City Home Prices); Bank of Japan Interest Rate Decision (Press Conference by Deputy Governor Shinichi Uchida)

-

June 17 (Wed): US May Retail Sales Data (often dubbed "Horror Data" for its market impact); UK May CPI

-

June 18 (Thu): Federal Reserve Interest Rate Decision and Press Conference (New Chair's Debut); Bank of England Interest Rate Decision

-

June 19 (Fri): Japan May CPI Inflation Data

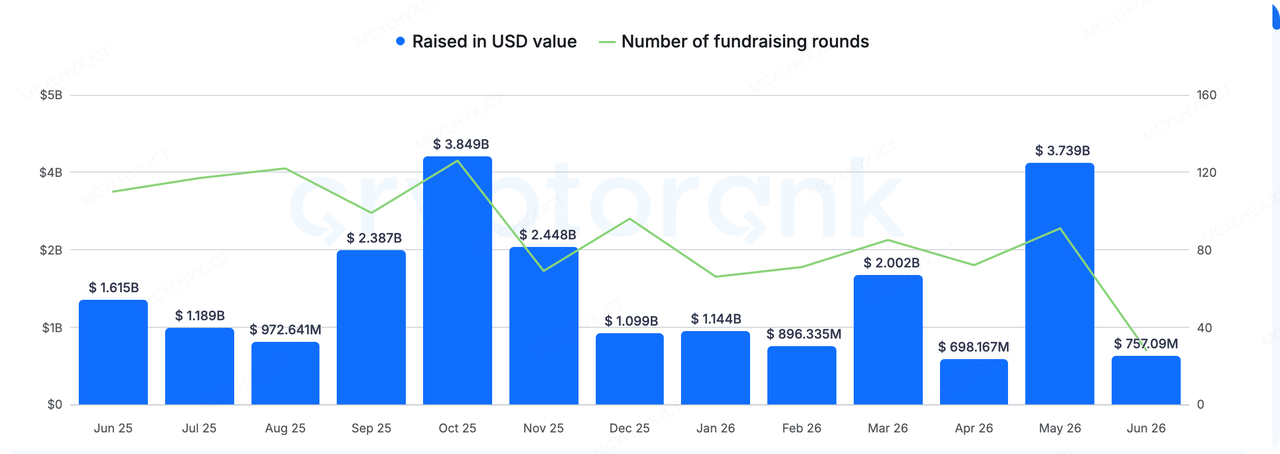

Primary Market Financing Observations:

Data Source: CryptoRank

This week, the primary market exhibited an extreme "ice and fire" dichotomy and highly concentrated structural characteristics. According to tracking data from RootData, this week not only birthed super-massive funding rounds like Digital Asset ($355 million) and Morpho ($175 million), but mature project M&A (Mergers and Acquisitions) continued to be a core keyword—from Blockworks acquiring Messari, to GSR Securities, Metaplanet Securities, and Light Protocol being successively acquired.

The flow of capital and industrial resources gives a clear signal: the crypto market is accelerating the clearance of redundant noise, and infrastructure in core sectors is concentrating towards a few top oligopolies.

Crypto media and data platform Blockworks acquired its former rival Messari for slightly over $10 million. It is worth noting with a sigh that Messari was valued at a whopping $300 million in its previous funding round in 2022. This brutal 96% haircut acquisition nakedly reveals the merciless washout inflicted by the bear market and cycle transitions on once highly-valued startups.

-

Logic Evolution: In previous bull markets, data platforms primarily served retail sentiment and hype; but this cycle is different. The approval of ETFs, the tightening of compliance frameworks, and the influx of Wall Street institutional capital are forcing the entire industry to align with traditional finance's research and disclosure systems. As the volume of capital grows, the market no longer just needs news flashes and candlesticks, but structured databases, rigorous research report systems, and long-term fundamental tracking.

-

Sector Centralization: Every maturation phase of the crypto industry goes through a process of "first compressing the noise, then centralizing the infrastructure." We have already seen the centralization of exchanges, custodians, and ETF channels, and now it's the turn of data and research portals.

Judging from recent primary market shifts, the next capital cycle will belong to infrastructure builders who can bridge institutional capital flows, possess solid closed-loop business models, and provide compliance-grade services.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.