Beyond Crypto Trading: Mapping Crypto Pre-IPO Markets

2026/06/15 17:38:00

From AI Giants to Private Markets: The Next Frontier for CEXs

Authors: KuCoin Ventures (Claude, Mia)

Crypto exchanges are currently experimenting with diverse Pre-IPO solutions. On the surface, this appears to be a race for exposure to highly sought-after private companies like OpenAI, SpaceX, and Anthropic. However, the deeper question is whether crypto exchanges will ultimately remain just highly efficient venues for risk trading, or evolve into more open,global asset accounts.

1. Introduction: Why Crypto-Based Pre-IPO Products Matter

The explosive growth of Pre-IPO assets and related solutions is not merely trend speculation. In our view, it is the result of three converging structural forces:

-

Top-tier private companies (e.g., in AI, aerospace, and hard tech) are delaying their IPOs, leading to a depleted supply of high-quality assets in public markets and capturing the most significant valuation upside within the private stage. By the time retail investors participate post-IPO, they are often nearing the exit windows of institutions and early shareholders.

-

Leading platforms like Robinhood, Coinbase, and Binance are facing bottlenecks in user traffic and asset supply, creating an urgent need to compete for mindshare as the "next-generation investment gateway."

-

Concurrently, industry development trends are becoming clearer. Ongoing market discussions and a gradually forming consensus are illuminating various product formats: issuer-authorized RWA (Real World Asset) tokenized securities, third-party packaged security exposures, and diverse forms of mirrored notes and derivatives. The CFTC's late-May stance on perpetual contracts also indicates a tendency to discuss them within a framework of regulated exchanges, clearing, margin requirements, customer asset protection, and reliable price referencing. This overall positive signaling serves as a constructive response to market expectations.

Competition in this sector has reached a fever pitch. Today, the real question is no longer "who listed which trending asset," but rather: what exactly are users holding? Where does the pricing originate? Who acts as the custodian? What are the exit mechanisms? And what liabilities do the platforms bear?

Current market products vary significantly: SPVs, funds, tokenized funds, mirrored notes, synthetic tokens, and perpetual contracts—each corresponding to distinct asset ownership rights, regulatory boundaries, and exit mechanisms. Some function more like long-term investment accounts, while others are essentially just price exposures and trading instruments. Therefore, the true significance of crypto exchanges' Pre-IPO solutions lies in their role as a catalyst, pushing exchanges to test the waters from being pure crypto platforms toward becoming "comprehensive asset trading gateways."

-

If a platform intends to build investment-driven products, it must clearly address the underlying assets, custody, rights documentation, and exit mechanisms.

-

If a platform intends to build trading-driven products, it must clarify pricing sources, leverage, funding rates, liquidation mechanisms, and the non-equity nature of the instruments.

Moving forward, the access premium for "pseudo-equity" products operating in gray areas will likely be compressed. To retain independent value, exchanges cannot rely solely on regulatory blind spots. Instead, they must prove their superiority over traditional financial gateways in aspects such as trading efficiency, capital efficiency, global distribution, composability, or asset servicing.

2. Why Does the Market Need Pre-IPO Assets?

The market's concentrated focus on Pre-IPO and private equity tokenization in 2025-2026 is highly correlated with the rising heat around AI and the delayed IPOs of several top-tier unicorns. However, the deeper endogenous reasons are multifaceted: a supply deficit of high-quality growth assets in public markets, the waning narrative of crypto-native assets, rising user demand to participate in high-growth targets, and the simultaneous strategic imperative for exchanges to evolve from pure crypto platforms into comprehensive asset gateways.

1) High-quality growth assets are entering public markets increasingly late.

Historically, an IPO was the key dividing line for growth companies transitioning from institutional to public capital. Today, top emerging AI companies often complete the majority of their valuation expansion within the private market. By the time retail investors participate post-IPO, they may already be approaching the liquidity exit windows of institutions, employees, and early investors. A primary driver of Pre-IPO demand is precisely this unequal distribution of returns between public and private markets. This mirrors the dynamic once prevalent in the crypto market, where high-FDV (Fully Diluted Valuation), low-float "VC coins" necessitated limited, discounted IEOs to generate wealth effects.

2) The IPO window is recovering, and top private companies possess immense narrative density and liquidity appeal.

Companies like OpenAI, SpaceX, Anthropic, xAI, Stripe, and Databricks carry strong narrative weight and the ability to attract liquidity. For exchanges, these assets are primed to be packaged into a new cycle of narrative-driven assets: low cognitive barrier for users, high market attention, substantial price volatility, and the potential to foster cross-platform competition.

3) The crypto market inherently needs new asset supply.

As the altcoin bubble recedes and relying solely on new token issuances fails to sustain trading activity, CEXs must seek new targets beyond crypto-native assets. Pre-IPO assets sit at the intersection of "traditional asset logic" and "crypto trading experience." They are backed by real-world companies and growth narratives, yet can be structured into low-barrier, tradable, and globally distributable products.

4) RWA infrastructure is now equipped to onboard equity-based assets.

Capabilities such as stablecoin settlement, on-chain wallets, KYC and geo-fencing, custody, oracles, AMMs, on-chain order books, perpetual contract risk management, and cross-chain distribution have steadily matured. Private assets—previously highly non-standardized, low-frequency in trading, and heavily reliant on legal paperwork—now have the opportunity to be fractionalized and introduced to broader global distribution networks.

5) Trading platforms are competing for the "comprehensive asset account" gateway mindshare.

The appeal of Pre-IPO assets lies not just in specific targets, but in their ability to facilitate a paradigm shift: users are beginning to re-evaluate exchanges from being mere "venues for trading crypto tokens" to "trading gateways for global new economy enterprise assets." Wallets, Launchpads, Earn products, asset management, derivatives, and RWA sectors can all anchor around Pre-IPO with distinct positionings—some serving long-term allocation, some catering to speculative trading, some driving brand elevation, and others optimizing for user engagement and capital retention.

Therefore, Pre-IPO is not an isolated RWA branch, but a crucial testing ground for exchanges expanding their asset boundaries. It simultaneously captures the spillover demand for private growth assets, the need for new asset supply within the crypto market, and the strategic imperative for platforms transitioning from pure crypto origins to comprehensive asset trading gateways.

3. Why Are These Products Emerging Now?

The concentrated rollout of Pre-IPO tokenization and crypto solutions in 2025-2026 is not because private assets have suddenly become easier to circulate. Rather, it is because capabilities across trading, settlement, custody, risk management, and compliance structuring have gradually matured. This allows previously highly non-standardized private exposures to be productized and traded.

1) On-chain financial infrastructure is now sufficient to support the distribution and trading of non-standard assets. Stablecoins have solved USD denomination and cross-border settlement; wallets provide a global user gateway; on-chain order books, AMMs, and CEX matching engines offer secondary trading capabilities; and KYC, geo-fencing, and whitelist mechanisms provide essential tools for user onboarding across different jurisdictions. Built on this foundation, private assets—which previously relied on legal paperwork, OTC matching, and high barriers to entry—can now be fractionalized and introduced to broader distribution networks via tokens, notes, fund shares, or contracts.

2) Product structures have expanded from "actual equity transfers" to multi-layered economic exposure packaging.

The current market no longer relies solely on direct equity transfers. Instead, it utilizes diverse structures such as SPVs, funds, tokenized funds, tracking certificates, mirrored tokens, pegged notes, and perpetual contracts to package underlying private assets or valuation expectations into tradable products across different tiers.

This means that for different products, two core questions must first be distinguished:

-

Whether the private asset itself can be legally issued, transferred, and distributed.

-

What rights the on-chain token, note, or contract actually represents.

"Putting securities on-chain" is not inherently regulatory arbitrage. The real dividing line lies in whether the token represents actual security rights, whether it is recognized by the issuer or their agent, whether the underlying securities are subject to transfer restrictions, whether on-chain transfers trigger synchronized off-chain ownership changes, and whether the product is merely a synthetic exposure issued by a third party.

3) Regulatory direction is transitioning from ambiguity to boundary redefinition.

Since the most sought-after targets for crypto Pre-IPO assets are currently U.S. tech companies, product design cannot bypass several core boundaries: U.S. securities law, private equity transfer restrictions, issuer corporate bylaws, shareholder registry rules, SPV equity transfer arrangements, security-based swap regulations, and investor suitability requirements.

Based on relevant SEC public filings and regulatory logic, if a product fundamentally represents security rights, the right to securities returns, or security price exposure—regardless of whether it is packaged as a token, note, investment contract, or cash-settled derivative—it typically needs to be analyzed under the corresponding securities regulatory framework.

Recent official documents and public discussions indicate that U.S. regulatory priorities may include lowering the costs of going and staying public, exploring viable pathways to open private assets to retail investors, and clarifying the legal boundaries of tokenized securities. This implies that the regulatory focus may not simply be an outright liberalization of Pre-IPO tokens, but rather integrating growth assets into a more formalized product system featuring disclosure, valuation, and accountability.

Consequently, the narrative that gray-market Pre-IPO products previously relied on—that "retail investors have no other access"—may gradually weaken. Future on-chain solutions that retain value will likely need to prove their tangible advantages in trading efficiency, global liquidity, short-selling capabilities, leverage, real-time price discovery, or cross-border distribution, rather than relying solely on regulatory blind spots and access scarcity.

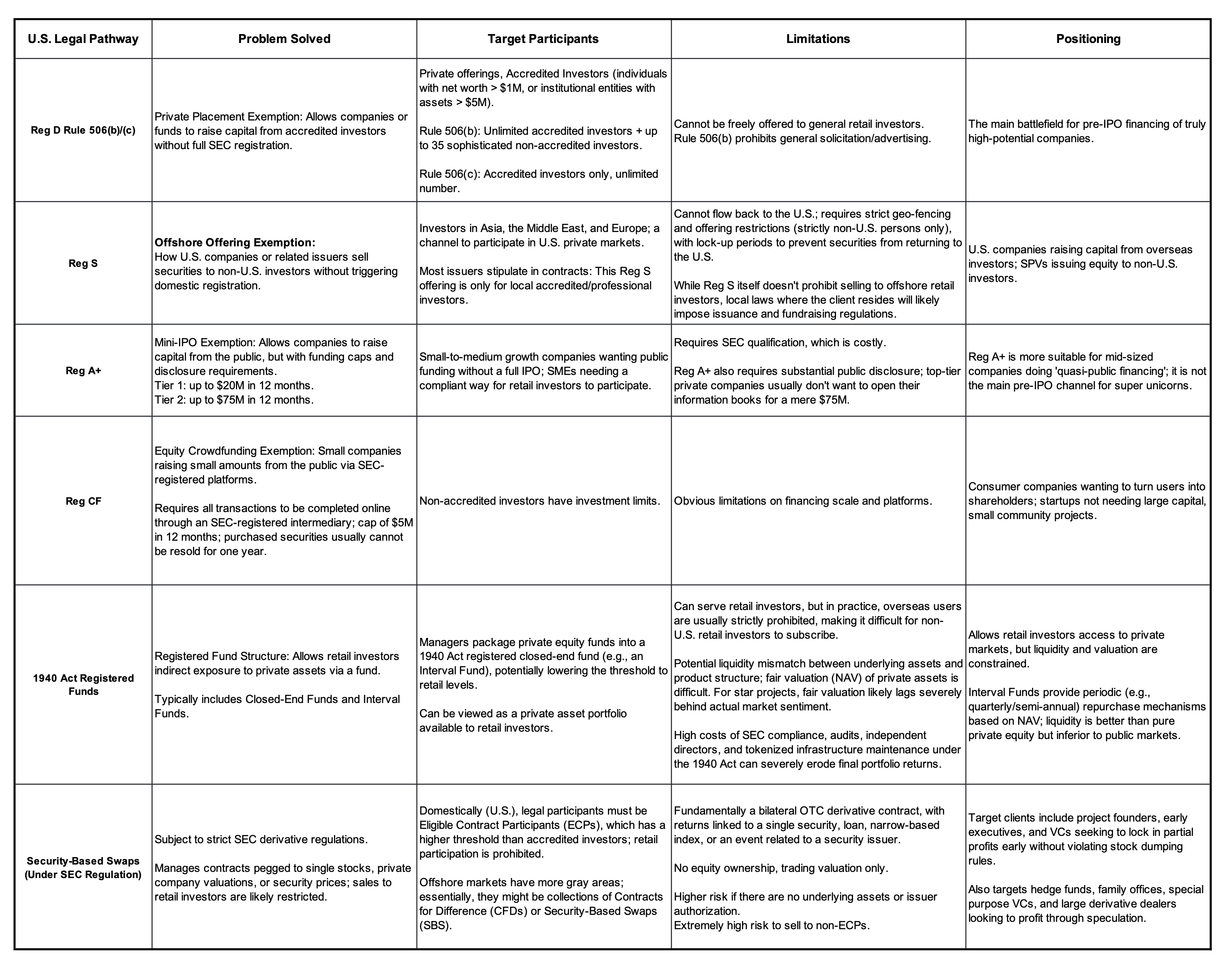

Legal Framework and Exemption Pathways for the Issuance and Trading of U.S. Private Assets

Source: SEC official website and online public sources.

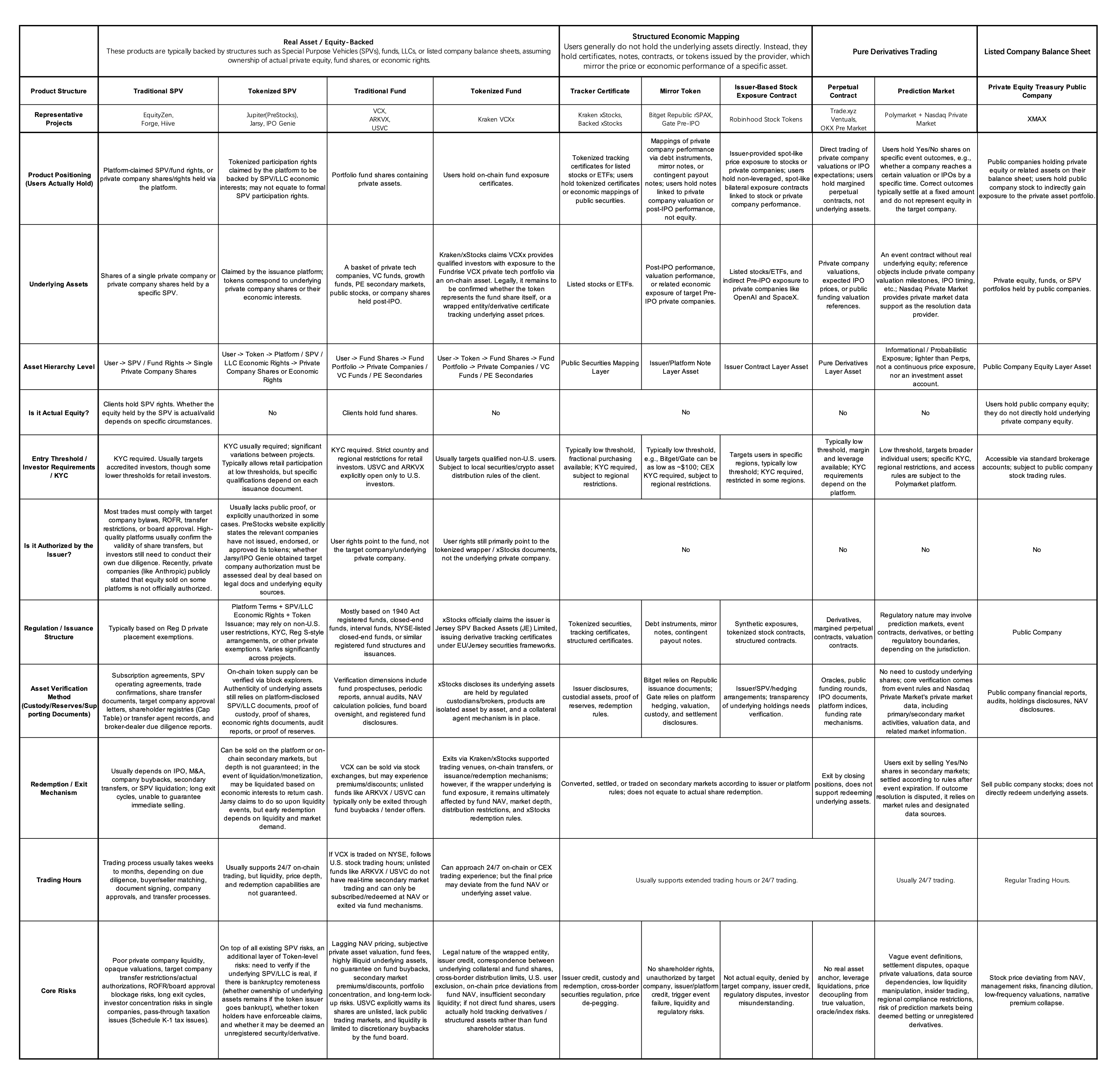

4. What Products Are Actually Operating in the Market?

The current Pre-IPO products in the market may appear complex, but they fundamentally answer the same question: how to package private assets—originally characterized by high barriers to entry, low liquidity, and strict transfer restrictions—into products that retail users can access, platforms can distribute, and the market can trade. These can be broadly categorized into five tiers based on the strength of investor rights. The higher the tier, the closer it is to actual asset ownership; the lower the tier, the closer it is to pure price exposure and trading instruments. Different tiers correspond to varying regulatory risks, commercial values, and approaches to user education.

Tier 1: Actual Equity Recognized by the Issuer

This category possesses the clearest rights but entails the highest execution difficulty. It requires issuer approval, compliant equity transfers, investor qualification screening, securities registration, custody, transfer agents, tax processing, and cross-border sales arrangements. It aligns most closely with traditional securities market logic and establishes high long-term barriers to entry. However, due to varying degrees of legal recognition for on-chain equity, securities registration, and on-chain transfers across jurisdictions, rapid global expansion is highly difficult in the short term.

Tier 2: SPV / Fund Shares

Investors hold rights in an SPV (Special Purpose Vehicle) or fund, which indirectly holds shares in the target company. This model reduces the complexity of directly entering the target company's cap table and aligns with traditional private secondary market practices. However, its critical risks lie in whether the target company recognizes the equity or rights transfer, whether transferring SPV shares requires consent from the GP, the platform, or the company, and whether the exit pathway is clear.

Tier 3: Tokenized SPVs

This structure further brings traditional SPVs, fund shares, or related economic interests on-chain, enhancing distribution and trading convenience. Consequently, the contradiction becomes more apparent: the transferability of an on-chain token does not guarantee the free transferability of the off-chain equity, SPV shares, or fund rights. A significant mismatch may exist between the liquidity of the outer-layer token and the underlying asset. Thus, the critical question for this tier is whether the underlying asset documentation, proof of custody/reserves, ownership mapping, and redemption mechanisms are sufficiently robust and transparent.

Tier 4: Economic Interest-Linked Certificates (Linked Note / Mirror Token / Synthetic Token)

These products are typically issued by third parties. Investors acquire economic returns tied to the target company's valuation, post-IPO performance, or related asset prices, rather than acquiring shareholder status. The advantages are structural flexibility, high issuance efficiency, low distribution barriers, and easy integration for exchanges or wallets. The primary risk is that investors bear the issuer's credit risk, structural term risks, price tracking risks, and uncertainties surrounding triggering events.

Tier 5: Pre-IPO Perps / Valuation Perpetual Contracts

This is a relatively lightweight structure. Investors gain price exposure without share delivery, shareholder rights, or corporate-level claims. It is better suited for traders expressing views on a private company's valuation, and for exchanges creating high-liquidity, long/short, leveraged trading products. It can also center around verifiable events (e.g., Pre-IPO prediction markets on whether a company IPOs by a certain date, whether day-one market cap exceeds a threshold, or whether a funding round valuation hits a specific range).

In its policy statement on perpetual contracts, the CFTC noted that perps lack a fixed expiration date and rely on a funding rate mechanism to maintain relative alignment with the underlying asset's spot price. Precisely because perps have no settlement expiration, their reference price cannot simply be reliable at a single settlement point; it must remain continuously reliable across every funding rate interval. The CFTC's explanatory document regarding Deribit's perpetual contracts also explicitly limits its scope to Deribit-like perp structures where the underlying is a digital commodity with deep, active, and continuous spot market trading. This interpretation does not extend to asset classes beyond digital commodities.

This presents a dual signal for Pre-IPO Perp products:

-

Positively: Perps are entering the regulatory discussion framework as a product structure and should no longer be simply equated with offshore gray-market products.

-

Negatively: Regulators will place greater emphasis on whether the underlying asset possesses a continuous, deep, observable, and manipulation-resistant reference price.

Digital commodities like BTC and ETH meet this requirement relatively easily. However, the equity valuations of private companies like SpaceX, OpenAI, and Anthropic lack continuous public price feeds. Their price discovery relies heavily on oracles, market makers, order books, and parameter design. If the underlying is an economic exposure to a single private company's equity, it may also trigger SEC scrutiny regarding security-based risk exposures or security-based swaps.

In other words, the advantage of a Pre-IPO perp is that it mitigates issues related to actual equity transfers, SPV rights transfers, and issuer shareholder registries; however, it does not bypass the issues of derivatives regulation, market manipulation, investor suitability, and the reliability of the price anchor.

The regulatory risks, commercial values, and user education approaches corresponding to these five structural tiers are entirely distinct. Therefore, before designing and listing Pre-IPO products, platforms must clarify their positioning:

-

Investment-driven products must answer: "What exactly are users holding, who is the custodian, how do they exit, and who is liable for recourse if something goes wrong?"

-

Trading-driven products must answer: "Where does the price originate, how is leverage restricted, how are funding rates calculated, and how do liquidation rules protect users?"

If a platform conflates these two narratives, it risks simultaneously amplifying mis-selling, blurring compliance boundaries, and misaligning user expectations.

Classified by asset mapping logic and specific product structure, a detailed comparison is provided below:

Source: Project official websites, official documentation, and press releases

5. Key Case Studies

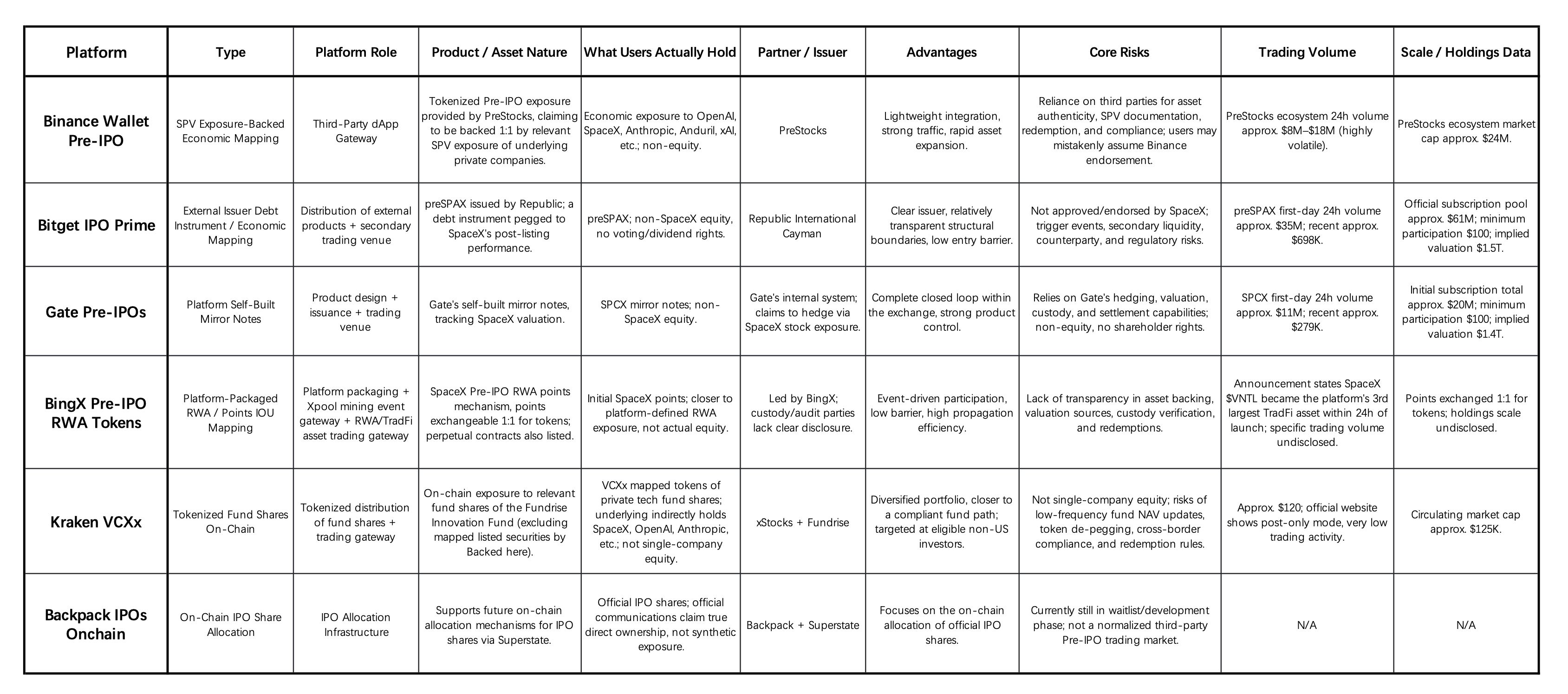

5.1 Core Comparison of Pre-IPO Solutions Across Crypto CEXs / Exchange Wallets

Source: Project official websites, official documentation, and press releases

1) Pre-IPO is emerging as a new narrative gateway for exchanges to supplement asset supply. Against the backdrop of high-quality tech companies remaining private for longer and a shortage of high-growth asset supply in the crypto market, exchanges and wallets are packaging "Pre-IPO Alpha exposure" to companies like OpenAI, SpaceX, Anthropic, ByteDance, and DeepSeek into low-barrier entry points. The significance of this extends beyond merely adding new trading instruments; it facilitates the transition of CEXs from pure crypto platforms into comprehensive asset trading portals.

2)the depth of platform participation defines the boundaries of liability. Binance Wallet operates primarily as a traffic gateway, with underlying liabilities resting mostly on PreStocks. Bitget relies on Republic's external issuance structure, assuming mainly distribution and trading roles. Gate and BingX lean toward self-built or self-packaged solutions, facing greater pressure to justify valuations, asset backing, custody, hedging, and settlement. Kraken VCXx is pursuing the tokenization of fund shares, while Backpack remains in the infrastructure development phase for on-chain IPO allocation.

3)most products represent economic performance mapping rather than actual equity. Aside from Backpack's official communications emphasizing the potential future provision of real IPO shares, current CEX-related products predominantly offer SPV exposure, debt instruments, mirror notes, points/IOUs, or fund share mappings. They typically do not grant users voting rights, dividend rights, or direct shareholder rights.

4)the sector is still in a traffic-testing phase and lacks institutional-grade depth. Bitget and Gate experienced high trading enthusiasm initially, but subsequent liquidity and sustained trading volumes have yet to be proven. Kraken VCXx exhibits lower scale and activity, while BingX and Backpack lack complete comparable data. Overall, these products currently focus on capturing user mindshare and experimenting with asset innovation. Due to limitations regarding compliance frameworks, asset verification, proof of custody, redemption mechanisms, and secondary liquidity, significant institutional capital likely remains on the sidelines.

5)the long-term opportunity lies in establishing Pre-IPO RWAs as core infrastructure. Future competition will not merely revolve around "who lists the most trending assets," but on establishing robust capabilities in asset verification, issuer authorization, proof of custody, valuation mechanisms, KYC/qualified investor screening, redemption settlement, and secondary liquidity management. To capture long-term value in this track, CEXs must evolve from narrative-driven asset gateways into verifiable, tradable, and manageable pre-IPO asset infrastructures.

5.2 Trade.xyz Core Solution Breakdown

Trade XYZ's IPOP (Pre-IPO Perpetual Contracts) are USDC cash-settled perpetuals that primarily reference the expected listing price or valuation of target companies. Technologically, its order matching, funding rates, liquidations, and ADL (Auto-Deleveraging) are managed by HyperCore, while Trade XYZ is primarily responsible for pricing components such as oracles, mark prices, and external prices.

Upon launch, each IPOP has an initial reference price. According to official documentation, this initial price is currently a synthesized judgment based on the market's expected IPO range, private valuations, media reports, secondary market prices, and anticipated issue prices. Post-launch, the Perp price is driven primarily by long and short trading activity. Without external market prices, Trade XYZ's oracle relies on an internal mechanism: it calculates the buying and selling pressure imbalance from the order book, and then uses a continuous-time EMA (Exponential Moving Average) to incrementally adjust the price. The oracle updates every 3 seconds, but only moves a fraction of the distance between the current price and the target price. A larger time constant makes the price harder to manipulate, but also slower to react.

Overall, prior to a Pre-IPO asset's listing, the contract's shadow price is collectively formed by the order book + liquidity + long/short forces + funding rates + market expectations.

Post-IPO, Trade XYZ states it will transition the Pre-IPO contract into a standard externally-priced perpetual contract. If the company fails to list, settlement may occur based on the TWAP (Time-Weighted Average Price) of the IPOP asset's lifecycle (calculating the time-weighted average price over the entire trading period, the full lifespan, or a 60-day window). Simultaneously, Trade XYZ explicitly states that these contracts are not shares, not IPO allocations, and not tokenized equity; they confer no ownership, voting rights, or dividend rights.

The significance of Trade.xyz lies not merely in listing trending assets, but in employing a complete Traditional Finance (TradFi) Perp parameter system to solve the problem of "where price discovery comes from when external markets are closed." Its mechanisms include the oracle extracting data from the order book, slow convergence to target prices, time constants, safety valves, price bands, funding rate scaling, and ADL. The prior authorization of the S&P 500 index by S&P Dow Jones to Trade.xyz indicates that the combination of "authorized data + on-chain perps" is already being tested by traditional index institutions.

Compared to spot-based Pre-IPO products, Pre-IPO Perps offer three main advantages:

-

Shorting Mechanisms and Two-Way Liquidity: Actual Pre-IPO equity is highly illiquid, and a "securities lending" market is virtually non-existent in the physical spot market. This implies that even as regulated spot tokenization channels develop, investors may primarily face long-only structures. Perps bypass the physical constraints of spot lending through funding rate mechanisms, providing shorting and hedging tools for highly illiquid Pre-IPO targets (e.g., SpaceX, Anthropic, OpenAI).

-

Boundaries of Leverage and Capital Efficiency: Regulated US spot markets typically face strict retail leverage limits. Perps on derivative DEXs or CEXs can offer higher capital efficiency, though such leverage exposure may not be widely available to retail investors in the short term under traditional compliance frameworks.

-

Reducing Friction in Cross-Border Spot Delivery and Issuer Equity Transfers: Even as the US market explores tokenized securities, such products remain constrained by securities laws, broker KYC, and cross-border sales restrictions. Pre-IPO Perps do not deliver underlying stocks nor enter the target company's shareholder register. This objectively reduces friction related to SPV transfers, ROFR (Right of First Refusal), issuer consent, and cross-border equity delivery. However, regulatory risk is not eliminated. Recent CFTC statements suggest regulatory focus on Perps will shift toward the reliability of reference prices, susceptibility to manipulation, adequacy of margins and customer asset protection, and whether SEC joint review is required if the underlying asset represents single-company equity exposure.

Naturally, Pre-IPO Perp products also carry several key risks:

1) Price discovery relies heavily on oracles, market makers, and parameter design, making it susceptible to order-driven manipulation during low liquidity.

2) Open Interest (OI) caps, contract price bands, funding rates, and ADL will impact the actual trading experience.

3) Despite lacking equity transfer conflicts, they may still trigger regulations concerning derivatives, security-based swaps, market manipulation, and suitability.

4) The price of Pre-IPO Perps may reflect sentiment and access premiums for extended periods and should not be viewed as the target company's true valuation.

Trade.xyz's value lies in providing continuous trading and two-way expression mechanisms for Pre-IPO valuations. However, its compliance narrative is better scoped as a "non-equity, cash-settled, valuation expectation trading tool"rather than "buying pre-listing shares of a company early." For these products to achieve institutionalization in the future, the core focus cannot just be listing more hot assets; they must also demonstrate that their pricing sources, risk parameters, market surveillance, and customer protection mechanisms can withstand regulatory scrutiny.

Simultaneously, numerous products in the market attempt to align closely with SPVs, economic equity rights, mirror tokens, or linked notes. The critical question here extends beyond "how the price is traded" to "whether the underlying company recognizes these equity arrangements." This is precisely why Anthropic's statement warrants a separate discussion.

6. Structural Risks and Opportunities from Issuer Attitudes: From Anthropic's Statement to Platform Strategies

In May 2026, Anthropic updated its statement regarding unauthorized sales of company stock and investment scams. The company emphasized that both its common and preferred stock are subject to transfer restrictions. Stock transfers, or transfers of economic interests in Anthropic stock, without board approval will not be recognized on the company's shareholder register. In other words, even if a buyer provides capital, Anthropic will not necessarily recognize them as a shareholder.

Anthropic's statement further noted that Special Purpose Vehicles (SPVs) are not permitted to hold Anthropic stock. Any transfer of Anthropic stock to an SPV may be deemed invalid under its transfer restrictions. Offers to participate in past or future Anthropic funding rounds via SPVs are also explicitly prohibited by the statement.

More precisely, if the core economic value of an SPV or a structured note derives from Anthropic equity interests and attempts to bypass the company's transfer restrictions, the arrangement risks remaining unrecognized by the company.

Such statements have a direct impact on Pre-IPO products: when issuers explicitly oppose unauthorized equity transfers, structures like SPVs, tokenized SPVs, mirror tokens, and linked notes may conflict with corporate bylaws, transfer restrictions, shareholder registers, and issues of investor misrepresentation. Risks are particularly elevated for products marketed as "close to real equity" but unable to prove issuer authorization or the validity of title transfer.

In contrast, purely cash or stablecoin-settled Pre-IPO Perps are structurally lighter. They do not claim to hold underlying shares, offer no shareholder rights, and do not enter the target company's shareholder register. Therefore, the likelihood of being directly impacted by an issuer's equity transfer restrictions is relatively low.

Naturally, this does not mean Perps are a risk-free structure. It simply shifts the risk from "the validity of equity transfer" toward "derivatives compliance, pricing sources, oracle mechanisms, leveraged liquidations, market manipulation, and investor suitability." For offshore exchanges prioritizing efficiency, Pre-IPO Perps are better understood as price exposure products rather than equity substitutes.

Therefore, before launching Pre-IPO offerings, trading platforms must first clarify their core objective: are they building a trading market, or an asset account?

-

If positioned as a price-discovery trading platform: The product focus should be on liquidity, pricing sources, leverage, liquidation, funding rates, risk disclosure, and the prevention of market manipulation. The products can be Perps, synthetic indices, cash-settled contracts, or predictive exposures. However, platforms must explicitly inform users: these are not stocks, they do not represent shareholder status, and they provide no underlying corporate equity.

-

If positioned as a compliant value-investing platform: The due diligence focus must shift to the authenticity of the underlying assets, SPV/fund/note structures, issuer credit, custody arrangements, rights documentation, exit mechanisms, compliant sales jurisdictions, and investor suitability. In this scenario, platforms should not solely pursue trading volume; they must assume stronger responsibilities for asset distribution and investor protection.

Certainly, some trading platforms can advance both tracks simultaneously. They could launch investment-oriented Pre-IPO spot, note, fund, or SPV products within their LaunchPad, Wallet, Earn, Asset Management, or RWA modules, while concurrently offering Pre-IPO Perps in their derivatives modules, allowing users to trade the valuation expectations of unlisted companies.

However, in practical execution, issues of mixed product narratives may arise. If trading-oriented products are marketed as "buying real equity early," it amplifies the risks of mis-selling and regulatory scrutiny. Conversely, if investment-oriented products become overly trading-focused, it could transform long-term private equity assets into short-term, sentiment-driven trading vehicles.

7. Structural Opportunities for VCs

For VCs, the opportunities in crypto Pre-IPO solutions should not be limited to gaining exposure to a few trending companies. The opportunities more likely to form long-term moats lie in the infrastructure underpinning this value chain. This infrastructure ecosystem is bifurcating into two categories: one centered around capital efficiency, price discovery, and liquidity; the other focused on compliance, trust, asset ownership, and exit pathways.

7.1 Trading-Oriented Infrastructure: Core Services in Price Discovery, Leverage, and Liquidity

This track avoids the complexities of physical property rights delivery. Its core relies on crypto-native derivatives and prediction markets to resolve the pain points of the traditional Pre-IPO spot market—namely, the inability to short, lack of leverage, and fragmented liquidity. Its business model depends heavily on trading volume, volatility, market-making depth, and liquidity network effects.

-

Perp DEXs / Prediction Markets / Appchains and Ecosystems: The Perp DEX ecosystem, represented by platforms like Hyperliquid, still holds niche application and infrastructure opportunities. Attention should also be directed toward new challengers offering differentiated liquidity, risk management, or asset expansion capabilities.

-

RWA Perp Risk Management Systems: Systems supporting margin, liquidation, Auto-Deleveraging (ADL), price bands, and anomaly handling for non-crypto underlying assets like stocks, indices, commodities, and Pre-IPOs.

-

Oracles and Price Discovery Networks: Integrating private secondary transactions, funding round valuations, broker quotes, on-chain order books, market maker quotes, and external market prices.

-

Market Making and Cross-Market Hedging Tools: Tools assisting market makers in managing risks across on-chain contracts, OTC equity, public market proxies, and relevant indices.

-

Funding Rate and Risk Parameter Engines: Redesigning funding rate mechanisms, price bands, leverage limits, and position limits specifically tailored for traditional and private assets.

-

Trade Surveillance and Market Manipulation Prevention: Identifying wash trading, price manipulation, oracle attacks, and abnormal leverage behaviors in low-liquidity assets.

Following further statements from the CFTC regarding the regulatory path for perpetual contracts, future infrastructure opportunities for RWA Perps may expand from "whether it can be traded" to "whether it can be accepted by institutions and regulators." This includes compliant margin systems, customer asset segregation, risk disclosure, cross-border FBOT (Foreign Board of Trade) access, reference price governance, manipulation surveillance, real-time margin, liquidation and ADL disclosures, as well as parameter change audit systems tailored for regulatory review. The market will likely require more infrastructure to serve the compliance needs of TradFi institutions entering 24/7 derivative markets.

7.2 Investment-Oriented Infrastructure: Compliant Issuance, Title Transfer, and Exits for Assets

This track follows the institutional route of digitizing traditional financial assets. As public discussions by the SEC continue to focus on private asset valuation, governance, disclosure, and retail investor protection, this sector will likely undergo a shakeout, separating the robust from the flawed. Its business model is driven by AUM, asset distribution volume, and asset servicing fees. Key focal points include compliance moats, asset acquisition capabilities, issuer relationship networks, and institutional client trust.

-

Compliant Issuance Infrastructure: Private issuance through compliance frameworks, tokenization of private equity assets, Alternative Trading Systems (ATS), investor accreditation, and cross-border sales regulations.

-

SPV / Fund Administration: Establishment, management, accounting, tax, audit, investor registries, yield distribution, and liquidation for SPVs involved in token issuance.

-

Transfer Agency and Cap Tables: Securities registration, transfer approvals, shareholder registers, GP consent for share transfers, and issuer permissions management.

-

Custody and Proof of Ownership: Mapping, auditing, and attestation between off-chain equity, notes, or fund shares and on-chain tokens.

-

Private Asset Valuation and Disclosure: Disclosures regarding funding round data, secondary market transactions, fund NAV, discounts/premiums, lock-ups, and exit pathways.

-

Exit and Settlement Services: Post-IPO lock-ups, secondary transfers, tender offers, buybacks, fund redemptions, and stablecoin/fiat settlement.

In the long run, the most noteworthy players will likely possess both trading and asset account capabilities. The wallet interface serves as a crucial gateway: it can host spot assets, funds, notes, and SPV tokens, while also acting as a KYC channel to bind users' real identities. Simultaneously, it can connect with Perps, DEXs, lending, and yield products, further unlocking the liquidity and composability of Pre-IPO tokens.

Therefore, the market will continue to monitor the middleware that helps exchanges and wallets achieve multi-asset expansion. This includes compliance abstraction layers, cross-asset risk views, unified asset reporting, tax and valuation systems, private asset information disclosure modules, and product access controls tailored to different jurisdictions.

8. Conclusions and Trend Predictions

If the regulated US TradFi market initiates a top-down reopening of growth asset access to more ordinary investors, crypto products must prove they are not merely relying on "regulatory bypass/regulatory arbitrage." They must demonstrate superior trading experiences or asset servicing capabilities: 24/7 access, low entry barriers, global liquidity, shorting mechanisms, leverage, instant price discovery, composability, or more efficient cross-border distribution.

In March 2026, the SEC held a roundtable on private markets, focusing on valuation, governance, and "responsible retailization." In opening remarks, Commissioner Atkins noted that risk itself is not a valid reason for continuously excluding ordinary investors, but expanding access must proceed in tandem with investor protection, valuation governance, and appropriate guardrails. Judging from official statements, the focus of US regulatory discussions is not simply allowing retail investors barrier-free entry into private markets, but rather expanding participation pathways through product arrangements equipped with strong governance, disclosure, and valuation frameworks.

The long-term moats for pure tokenized titling and conduit businesses will likely be compressed by official traditional infrastructure. If the NYSE, Nasdaq, broker-dealers, ATS, registered funds, and private market platforms begin systematically providing formal access points, the access premiums for many unauthorized mirror notes, weakly-disclosed SPV tokens, and "pseudo-equity" products will likely decline.

However, this does not mean the market lacks new demand and business opportunities. A compliant spot market may not fully satisfy speculative capital's demands for capital efficiency, two-way trading, global access, and 24/7 price discovery. The independent ecological niche for Perps will likely remain intact. In fact, their market capacity may expand and risk management difficulty may decrease due to the future emergence of more reliable official spot prices and registered market references.

The subsequent evolution of Pre-IPO tokens will not necessarily be a single-track zero-sum game. It is more likely that platforms will develop multi-track product matrices based on their positioning, user demographics, and regulatory capabilities.

-

One track is the trading-oriented liquidity market: Platforms provide price discovery, leverage, long/short capabilities, and 24/7 trading. Users are trading the valuation expectations of unlisted companies. This direction is best suited for perpetual contracts (Perps), prediction market event contracts, synthetic exposures, mirror tokens, and indexed products. Its core competitiveness lies not in "whether it represents real equity," but in pricing mechanisms, liquidity, risk parameters, liquidation rules, and the overall trading experience.

-

The other track is the investment-oriented asset account: Platforms provide equity bearing, compliant issuance, custody, disclosure, and exit pathways that are closer to actual private assets. Users are purchasing long-term asset exposures. This direction is best suited for SPVs, funds, tokenized funds, compliant notes, and issuer-authorized products. Its core competitiveness lies not in trading stimulation, but in asset authenticity, rights documentation, proof of custody, valuation disclosure, and ultimate exit mechanisms.

A more realistic scenario is that top-tier exchanges will not limit themselves to just one route. They could seamlessly host investment-leaning Pre-IPO products within their Wallet, Launchpad, Earn, Asset Management, or RWA modules, while simultaneously launching Pre-IPO Perps, prediction markets, and synthetic exposures in their derivatives, DEX, or professional trading zones. This allows users with varying risk appetites to allocate, trade, and hedge within the same ecosystem.

The real risk does not lie in platforms pursuing both tracks simultaneously, but in conflating the narratives of the two. If trading-oriented products are packaged as "buying real equity early," it easily invites mis-selling and regulatory blowback. If investment-oriented products become overly financialized, it could transform long-term private equity assets into short-term, sentiment-driven trading vehicles.

Therefore, the players most likely to succeed in the future are not necessarily those solely focused on trading or asset accounts, but platforms capable of clearly stratifying the two systems.

On one side, they must clearly articulate the nature of trading products as "non-equity, pure price exposure." On the other side, they must solidify asset products by explicitly defining "what the user actually holds, how they can exit, and who to seek recourse from if issues arise." The true long-term value of exchanges will no longer be competing to list more Pre-IPO targets faster; what warrants the most attention is how they integrate trading, assets, risk management, disclosure, and user education into a single, coherent product architecture.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.