KuCoin Ventures Weekly Report: Compliance Rewires Stablecoins: Note-Issuing Banks Enter & Super DApps Emerge; Risk Aversion Dominates Macro Fund Flows

2026/04/14 15:33:01

1. Weekly Market Highlights

The Stablecoin Narrative Reaches a "Tipping Point": East-West Regulatory Frameworks Resonate as Top Projects Compete for Native Use Cases

In the current crypto capital market, stablecoins are undergoing a paradigm shift from "simple mediums of exchange" to the "core infrastructure of the crypto economy." This week, the stablecoin sector not only saw the substantive implementation and advancement of East-West policies at the macro-regulatory level, but at the application level, top Web3 native protocols like Hyperliquid and Polymarket are also utilizing them as core weapons to build ecological moats. This indicates that competition in the stablecoin sector has moved beyond the early battles for scale, officially entering a dual-track phase of "broadening compliance channels" and "implementing native use cases."

On the regulatory front, the clarification of policy frameworks is paving the way for the entry of large-scale traditional capital, and a "top-down" compliance channel is taking shape. Last week, the dust settled on the first batch of stablecoin licenses in Hong Kong. On April 10, the Hong Kong Monetary Authority (HKMA) announced the issuance of the first two Hong Kong stablecoin licenses to HSBC and Standard Chartered-backed Anchorpoint. Amid fierce competition from 36 applications, only these two large financial institutions with note-issuing bank backgrounds stood out, sending an extremely strong regulatory signal to the market.

Combined with the GENIUS Act previously advanced by the US, we can clearly see the common trends and divergent execution details in stablecoin regulation between the world's two major financial centers: both view Anti-Money Laundering (AML) and risk blocking as insurmountable red lines. However, in terms of implementation, the US leans towards "hard technical constraints" relying on code and rules, while Hong Kong has opted for "strong entity credit access" tied to traditional financial giants.

The HKMA demonstrated a high degree of restraint and caution in issuing the first batch of licenses. The regulator made it clear that even if additional licenses are issued in the future, the overall number will be extremely limited. The first batch of licensed institutions must possess robust asset reserve arrangements and the ability to prudently manage risks. This shows that Hong Kong is not currently pursuing a "decentralized" issuance format for stablecoins, but is instead prioritizing ensuring that they can operate within a controllable and auditable framework.

With note-issuing banks entering the fray with top-tier AML systems, the future stablecoin sector will no longer be a simple "coin issuance game." Instead, it will be an "asset-heavy, compliance-heavy" infrastructure that severely tests underlying liquidity management, B2B2C commercial use case expansion (such as cross-border payments and tokenized asset settlement), and on-chain/off-chain compliance penetration capabilities. For native Web3 institutions, relying solely on conceptual packaging is no longer viable. Only by elevating their AML capabilities to par with traditional banks, and making use cases solid and deep, can they possibly stay at the table in future licensing battles.

As external regulations gradually clear compliance hurdles, top on-chain applications have shown a significant divergence in their stablecoin strategies. They are no longer satisfied with simply integrating external USDT/USDC as settlement tools; instead, they have begun to deeply transform underlying settlement structures to build stronger liquidity moats and deliver ultimate user experiences within their applications.

-

Hyperliquid's Deep Integration with Native USDH: As the derivative DEX with the highest omnichain trading volume currently, Hyperliquid recently officially advanced the deployment of its native compliant stablecoin, USDH, through an on-chain validator vote. This is not simply issuing a token, but a system-level liquidity tilt: officials explicitly stated that in the recent network upgrade, the taker fee for spot-quoted assets (i.e., trading pairs using USDH) will be slashed by 80%, alongside increased maker rebates. This aggressive strategy directly and deeply binds the protocol's underlying public chain and omnichain order book with the native stablecoin. By shedding strong reliance on external centralized stablecoins, Hyperliquid successfully retains asset yield distribution rights and underlying liquidity within its own ecosystem.

-

Polymarket Expands the "Seamless" Infrastructure of pUSD: Diverging from Hyperliquid's route, the phenomenal prediction market Polymarket has opted for native empowerment of underlying assets. Recently, Polymarket launched Polymarket USD (pUSD), an internal collateral token on the Polygon network fully backed 1:1 by native USDC. This move aims to thoroughly strip away the vulnerabilities of the previously relied-upon bridged asset (USDC.e). By adopting pUSD and a brand-new trading engine, Polymarket successfully eliminated bridging risks, significantly lowered gas fees, resolved transaction failures under high concurrency (such as nonce invalidation), and achieved perfect compatibility with institutional-grade multi-sig wallets. Polymarket has also fully optimized the frontend experience: when ordinary users deposit USDC, the frontend automatically handles the conversion, and withdrawals seamlessly revert back, rendering the entire process virtually imperceptible. Overall, this upgrade can be seen as Polymarket paving the way for the large-scale entry of institutional funds and quantitative market makers.

This week's regulatory rollouts and project dynamics indicate that the stablecoin ecosystem is substantively bifurcating into two main tracks. "Regulated USD/HKD tokens," strongly constrained by the GENIUS Act and HKMA licenses, will become the settlement standard for traditional finance (TradFi) giants entering the crypto world. Meanwhile, on-chain super DApps are building moats by transforming underlying token structures—either relying on strong integration, self-built ecosystems, and fee subsidies to create use cases and cultivate user habits like USDH, or systematically optimizing the usage efficiency of native assets to create a seamless trading experience like Polymarket's pUSD. In the future, as the issuance framework and landscape of stablecoins are fundamentally established, subsequent competition will unfold more on the application side. Those who can command the "definition rights" and "consumption rights" of stablecoins in specific scenarios are more likely to command higher valuation premiums.

2. Weekly Selected Market Signals

U.S. “Blockade” Looms, Oil Returns Above $100, Gold Comes Under Pressure, U.S. Equity Futures Fall, and Crypto Pulls Back

Last Friday, the release of U.S. March CPI briefly lifted market sentiment, with U.S. equities opening slightly higher. However, the University of Michigan consumer sentiment index subsequently fell to a record low, reigniting concerns over a “high inflation + weak growth” backdrop. Over the weekend, U.S.-Iran peace talks collapsed, and Trump then announced a blockade on maritime traffic to and from Iranian ports. This triggered another sharp bout of volatility across global markets on Monday: oil prices moved back above $100, expectations of an energy supply shock intensified, the U.S. dollar strengthened, gold retreated, U.S. equity futures and Asian equities came under pressure, and cryptocurrencies also pulled back.

The U.S. and Iran held 21 hours of talks in Islamabad, Pakistan, but failed to reach an agreement. Iran viewed the U.S. demands as overly harsh, while Washington continued to press Tehran for explicit concessions on the nuclear issue. After the talks, Trump stated that “the only thing that became clear” was that Iran was unwilling to give up its nuclear ambitions. Beginning on April 13, the United States will impose a blockade on maritime traffic to and from Iranian ports. Given that the Strait of Hormuz is itself a critical chokepoint for global energy transportation, this move is still sufficient to materially raise market concerns over disruptions to crude oil and natural gas supply.

The breakdown in talks also reversed the improvement in risk appetite that had just emerged last week. Previously, expectations of a temporary U.S.-Iran ceasefire had helped lift the S&P 500 by 3.6% over the week, while the MSCI Emerging Markets Index also posted a notable rebound. But after tensions escalated again over the weekend, markets began repricing tighter energy supply and renewed second-round inflation risks. The Strait of Hormuz handles roughly one-fifth of global seaborne crude oil shipments. If Iranian exports and regional shipping remain disrupted, spot crude oil and natural gas prices are likely to remain highly volatile.

Supported by ceasefire expectations, the crypto market had briefly recovered alongside broader risk assets last week. But as geopolitical tensions flared again over the weekend, BTC pulled back and returned to trading around the $71,000 level. At the same time, institutional risk appetite has yet to show a clear recovery. Activity in CME Bitcoin futures has fallen to a 14-month low, suggesting that traditional institutions remain cautious about adding exposure in a highly volatile environment.

Data Source: TradingView

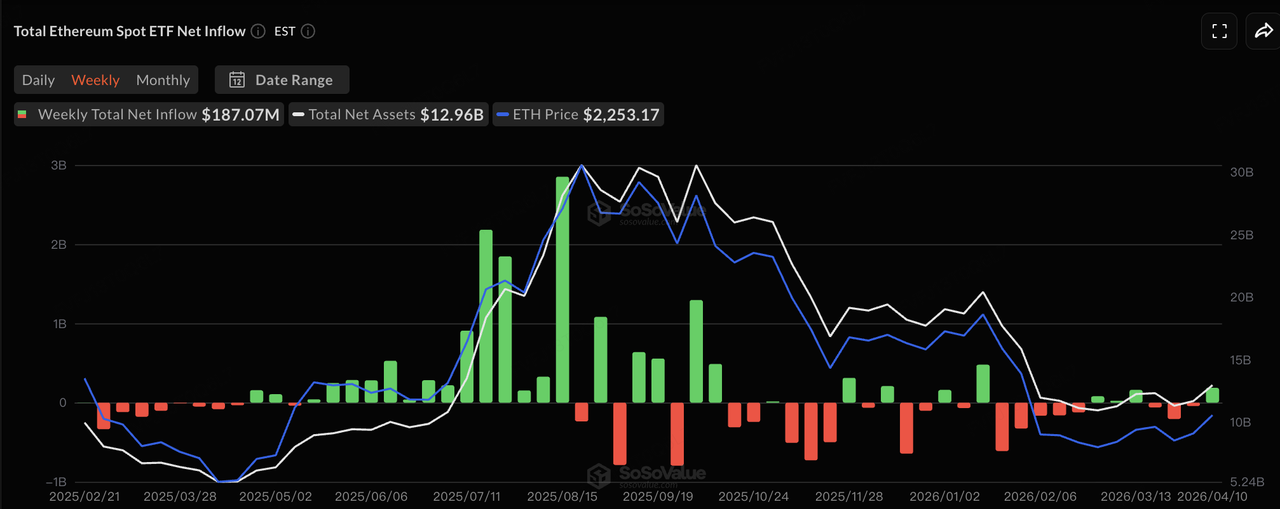

On the flows side, institutional allocation appetite through ETFs improved last week. According to SoSoValue, U.S. spot BTC ETFs recorded approximately $786 million in net inflows last week, while ETH ETFs saw $187 million in net inflows, ending three consecutive weeks of net outflows. This suggests that during the brief easing in geopolitical tensions, institutional capital did step back in to some extent. However, with U.S.-Iran tensions heating up again, it remains important to watch whether daily ETF flows weaken again this week.

Data Source: SoSoValue

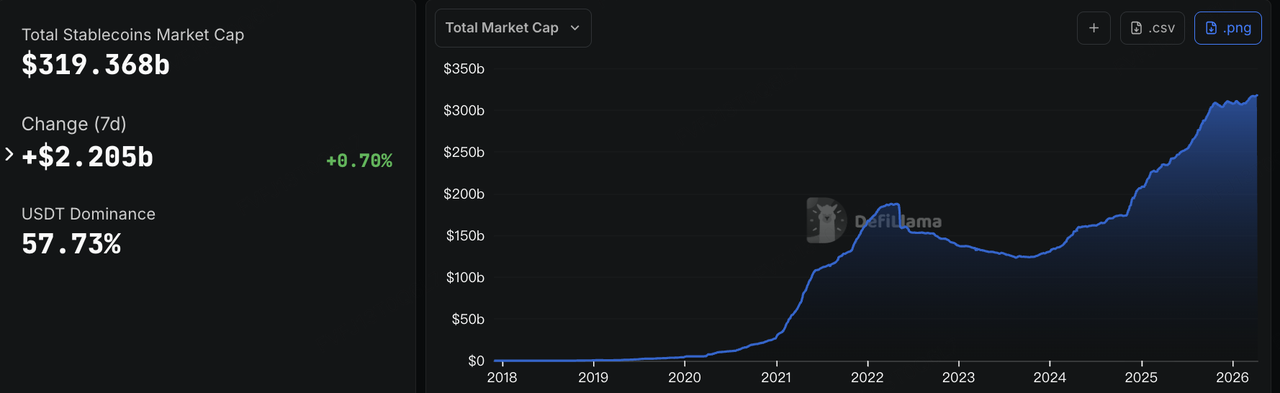

On-chain demand for “cash” has remained broadly resilient. Over the past seven days, total stablecoin supply increased slightly and continued to approach the $320 billion mark. Traditional fiat-backed and overcollateralized stablecoins remained broadly stable, with USDT, USDC, and PYUSD all continuing to expand. Meanwhile, tokenized U.S. Treasury products with RWA yield characteristics also continued to grow, with BlackRock’s BUIDL and Ondo’s USDY both moving higher, reflecting continued demand for on-chain U.S. dollar yield instruments in the current market environment.

Data Source: DeFiLlama

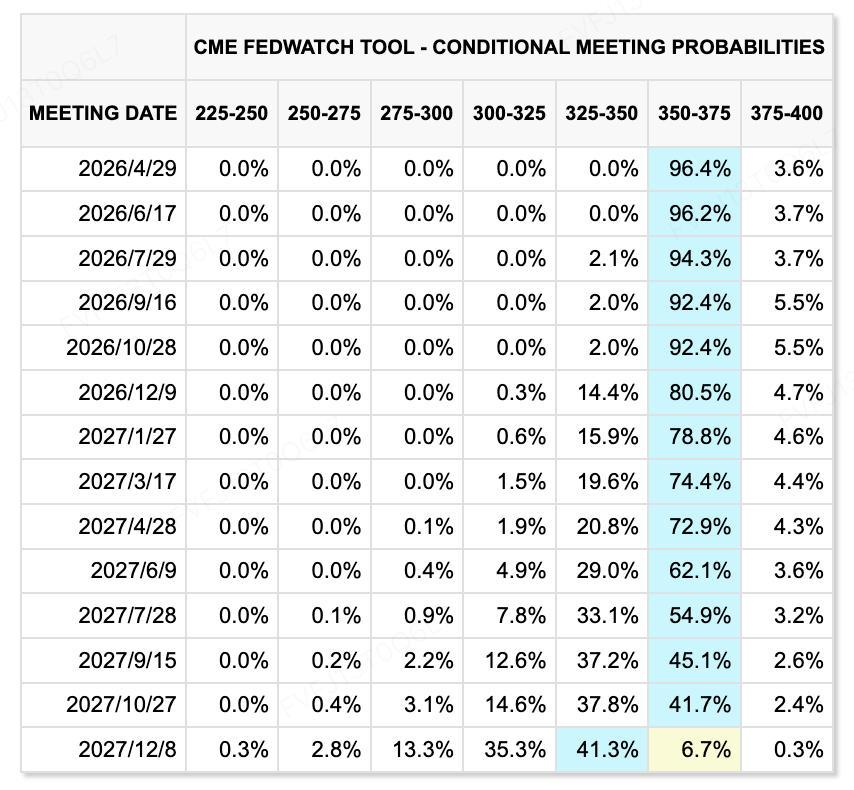

From a macro perspective, following the release of U.S. March CPI last week, the market has almost fully priced out the possibility of a rate cut in April, with the Federal Reserve keeping rates unchanged remaining the base-case expectation. This week, the market will focus on U.S. March PPI, the Beige Book, and speeches from multiple Fed officials to assess whether rising energy prices are beginning to feed further into producer prices. If oil remains elevated and PPI strengthens again, expectations for “higher for longer” interest rates could become even more entrenched. In the near term, geopolitics remains the key market variable, and headlines related to Hormuz will continue to drive the pricing of global risk assets.

Data Source: CME FedWatch Tool

Key Events to Watch This Week:

The market will focus on the following themes in the week ahead:

-

Geopolitics and energy markets: Following the breakdown in U.S.-Iran talks, the United States is preparing to begin a blockade on maritime traffic to and from Iranian ports. At the same time, OPEC and the IEA will release their monthly oil market reports, prompting the market to reassess the global supply-demand balance and inventory trends.

-

Macro and technology/industry developments: The U.S. first-quarter earnings season is officially underway, with Goldman Sachs set to report on April 13, followed by other major financial institutions and technology companies. Investors will closely watch how management teams assess the impact of higher oil prices, renewed inflation pressure, and geopolitical disruptions on demand and profit margins.

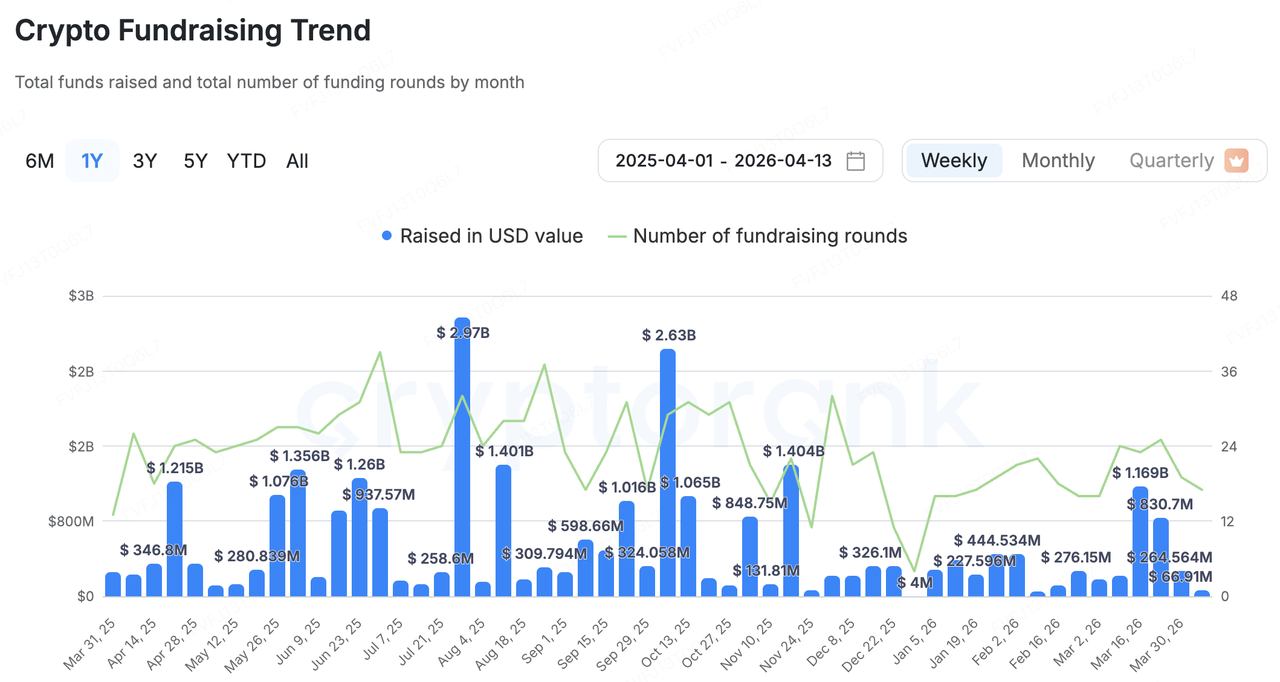

Primary Market Funding Observations:

Data Source: CryptoRank

In the primary market, according to CryptoRank’s broad statistical methodology, only $66.91 million in total funding was disclosed last week across 17 capital events. Overall activity remained subdued, with capital continuing to concentrate in a small number of larger deals. Among them, RWA infrastructure project Pharos completed a $44 million financing round, accounting for around 66% of the week’s disclosed total and standing out as the most significant single transaction.

In addition, GoSats announced the completion of a $5 million Series A round. Based in India, the project combines Bitcoin and gold rewards with everyday consumer spending to help businesses improve customer acquisition and loyalty. The new funding will mainly be used to launch additional fintech products and build an AI-powered personalized services system. The round was led by Konvoy, with participation from Y Combinator, Taisu Ventures, and others.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.