Stablecoin Transaction Volume in 2026: How Stablecoins Surpassed Visa and Mastercard

2026/05/16 07:36:24

Introduction

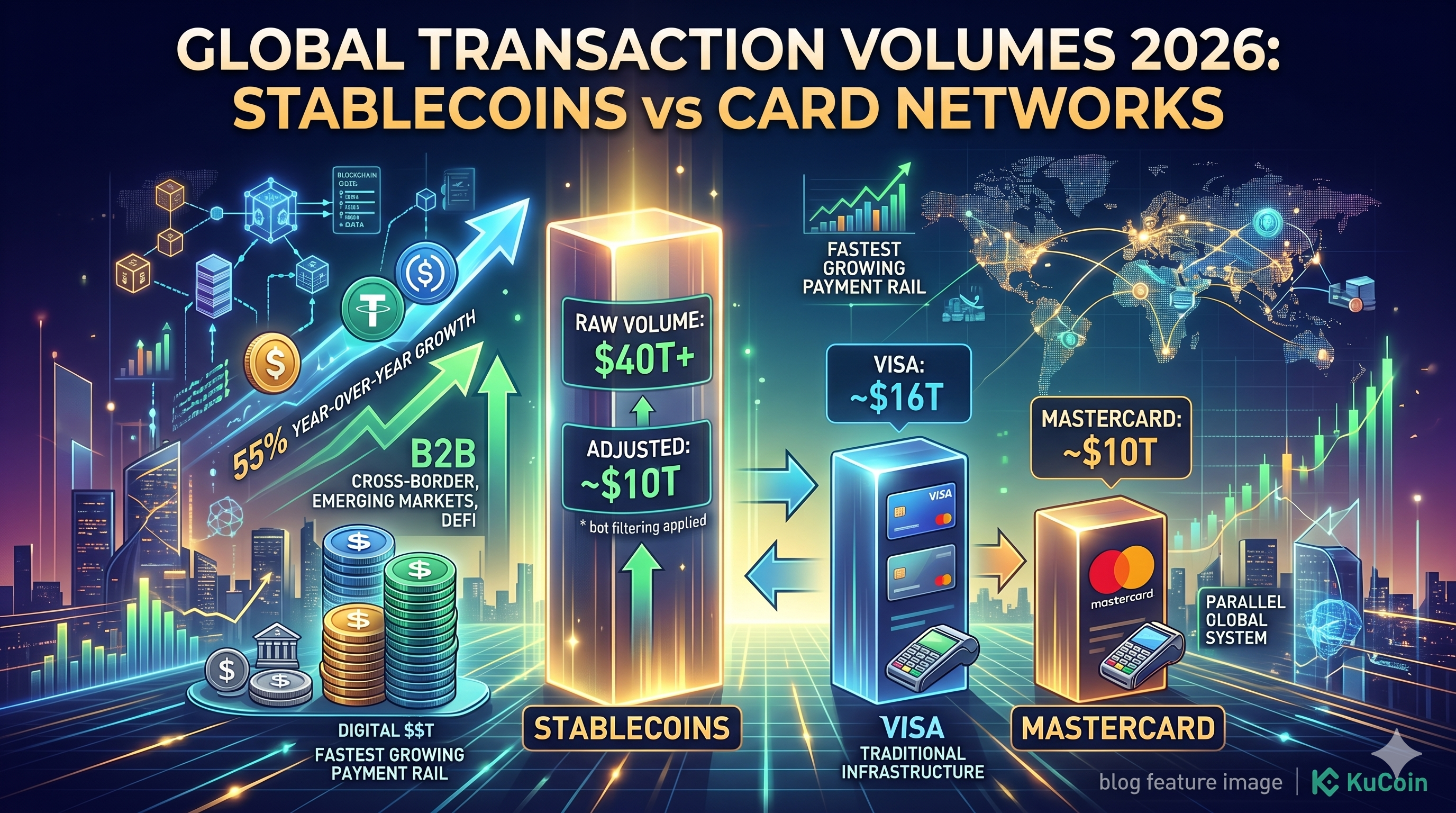

Stablecoins settled $27.6 trillion in transaction volume in 2024 — already exceeding the combined annual throughput of Visa and Mastercard — and projections for 2026 push that figure beyond $40 trillion. According to a March 2026 report from Standard Chartered's digital assets research desk, stablecoin on-chain settlement is now the fastest-growing payment rail in financial history, expanding at roughly 55% year-over-year.

The shift is no longer theoretical: USDT, USDC, and a growing roster of regulated dollar tokens are moving more value across blockchains than the two largest card networks combined move through traditional infrastructure. This article breaks down the 2026 numbers, separates organic payment volume from bot-driven activity, and explains what the milestone means for traders, businesses, and the broader crypto market.

How Much Volume Do Stablecoins Process in 2026?

Stablecoins are on pace to process between $40 trillion and $46 trillion in raw on-chain volume in 2026, according to data aggregated by Visa Onchain Analytics and Artemis in April 2026. That compares to roughly $16 trillion in combined annual payment volume reported by Visa and Mastercard across their most recent fiscal disclosures.

The gap widened sharply in the first quarter of 2026. Monthly stablecoin transfer volume averaged $3.8 trillion in Q1 2026, based on Artemis dashboard figures from April 2026, while Visa processed approximately $1.3 trillion per month and Mastercard around $850 billion.

Adjusted vs. Raw Volume

Raw volume overstates real economic activity, but even adjusted figures are massive. Visa's own on-chain analytics tool — which strips out bot trades, MEV activity, and internal exchange transfers — pegs "organic" stablecoin volume at roughly $9 trillion to $11 trillion annualized as of early 2026. That adjusted figure already rivals Mastercard's full annual throughput.

The distinction matters because critics often dismiss stablecoin volume as artificial. The reality is more nuanced: even after filtering, stablecoins now move trillions in genuine payment, remittance, and settlement value each year.

What Is Driving Stablecoin Volume Growth in 2026?

Three forces are pushing stablecoin transaction volume past card networks in 2026: cross-border B2B payments, on-chain treasury management, and emerging-market dollar demand. Each contributes a distinct slice of the trillion-dollar monthly flow.

Cross-Border B2B Payments

Cross-border business payments are the single largest organic driver. According to a Citi Treasury Services note published in February 2026, corporates settled an estimated $2.4 trillion in B2B stablecoin payments during 2025, with the figure expected to double in 2026. The appeal is straightforward — settlement in seconds, fees under 10 basis points, and no correspondent banking delays.

Companies like SpaceX, ScaleAI, and several major commodities traders have publicly confirmed using USDC and USDT for supplier payments in markets where SWIFT rails are slow or expensive.

On-Chain Treasury and DeFi Activity

DeFi-driven volume remains the second pillar. Stablecoins serve as the base trading pair on every major decentralized exchange, and lending protocols like Aave and Sky hold over $80 billion in stablecoin deposits as of April 2026, per DeFiLlama data. Treasury managers increasingly park idle capital in tokenized money market funds denominated in USDC.

Emerging-Market Dollar Access

Demand for digital dollars in Argentina, Turkey, Nigeria, and parts of Southeast Asia continues to surge. A Chainalysis report from March 2026 noted that retail stablecoin transfers under $10,000 grew 78% year-over-year in Latin America, reflecting genuine consumer adoption rather than speculative flow.

How Do Stablecoins Compare to Visa and Mastercard?

Stablecoins beat card networks on raw volume, settlement speed, and cost — but card networks still dominate consumer point-of-sale payments and merchant acceptance. The two systems serve overlapping but distinct functions.

|

Metric

|

Stablecoins (2026)

|

Visa

|

Mastercard

|

|

Annual volume

|

$40T+ (raw), ~$10T (adjusted)

|

~$16T

|

~$10T

|

|

Average settlement time

|

2-15 seconds

|

1-3 days

|

1-3 days

|

|

Average fee

|

0.01% - 0.10%

|

1.5% - 3.5%

|

1.5% - 3.5%

|

|

Active users

|

~250M wallets

|

4.5B+ cards

|

3.4B+ cards

|

|

Merchant acceptance

|

Limited but growing

|

130M+ merchants

|

100M+ merchants

|

Data compiled from Artemis, Visa, and Mastercard fiscal disclosures, April 2026.

Where Cards Still Win

Card networks retain a decisive edge in everyday retail. Chargeback protection, fraud insurance, and universal merchant integration remain unmatched. Stablecoins are not yet replacing the tap-to-pay experience at a coffee shop — they are replacing wire transfers, FX desks, and correspondent banking.

Where Stablecoins Win

Stablecoins dominate any use case where speed, cost, and global reach matter more than consumer protection. That includes B2B settlement, remittances, exchange transfers, and 24/7 capital movement across borders.

Which Stablecoins Drive the Most Volume in 2026?

USDT and USDC together account for roughly 88% of all stablecoin transaction volume in 2026, with USDT alone responsible for over 60% of on-chain transfers, according to CryptoQuant data from April 2026. The remaining share is split among USDe, PYUSD, FDUSD, and a growing list of regulated regional stablecoins.

Tether (USDT)

USDT remains the global liquidity king. Its circulating supply crossed $165 billion in early 2026, and it dominates emerging-market activity, particularly on Tron, where transaction fees are sub-cent.

Circle (USDC)

USDC leads in regulated and institutional flow. Following Circle's NYSE listing in 2025 and full MiCA compliance in the EU, USDC has become the default stablecoin for corporate treasuries, fintech integrations, and tokenized fund issuance. Its supply sits at roughly $62 billion as of April 2026.

Yield-Bearing and Regional Stablecoins

Ethena's USDe, PayPal's PYUSD, and newer euro- and yen-denominated stablecoins are growing fast but remain niche. Yield-bearing stablecoins in particular have attracted DeFi capital, with USDe alone clearing over $10 billion in supply by Q2 2026.

What Are the Risks of the Stablecoin Boom?

Stablecoin growth faces three principal risks in 2026: regulatory fragmentation, reserve transparency, and concentration risk. None are existential, but each could throttle volume growth.

Regulatory Fragmentation

The U.S. GENIUS Act, passed in late 2025, established a federal framework for payment stablecoins, but enforcement details remain in flux. Europe's MiCA is fully in effect, while Asia-Pacific jurisdictions range from welcoming (Singapore, Hong Kong) to restrictive (China, India). Cross-border issuers must navigate overlapping rules.

Reserve and Transparency Concerns

Tether continues to attract scrutiny over the composition of its reserves, despite quarterly attestations. Any loss of confidence in a major issuer could trigger redemptions large enough to stress short-term Treasury markets — Tether alone holds over $100 billion in U.S. government debt as of Q1 2026.

Concentration Risk

Two issuers controlling nearly 90% of volume creates systemic fragility. A technical failure, sanction, or smart-contract exploit affecting USDT or USDC would ripple across every major exchange and DeFi protocol simultaneously.

How Will Stablecoin Volume Evolve Beyond 2026?

Stablecoin transaction volume is projected to reach $80 trillion to $100 trillion annually by 2028, based on a Bernstein research note published in March 2026. Three trends will define the next phase.

Bank-Issued Stablecoins

Major banks including JPMorgan, Citi, and several European institutions are launching their own deposit tokens and stablecoins under the GENIUS Act framework. These will compete directly with USDT and USDC for institutional flow.

Tokenized Real-World Assets

Stablecoins are the settlement layer for tokenized Treasuries, money market funds, and private credit — a market BlackRock projects will reach $2 trillion by 2030. Every tokenized asset transaction settles in a stablecoin, multiplying volume.

Layer-2 and Alternative Chain Migration

Most stablecoin activity has shifted away from Ethereum mainnet to Tron, Solana, Base, and Arbitrum. Sub-cent fees and instant finality are making micro-payments and machine-to-machine transactions economically viable for the first time.

Conclusion

Stablecoins crossed the line from crypto curiosity to global payments infrastructure in 2026. With projected annual volume of $40 trillion or more — well above the combined throughput of Visa and Mastercard — digital dollars are now the fastest, cheapest, and most accessible way to move value across borders. Even after stripping out bot activity and internal exchange transfers, organic stablecoin volume rivals the world's second-largest card network.

The drivers are real and durable: cross-border B2B settlement, DeFi activity, and emerging-market demand for dollar access. USDT and USDC dominate today, but bank-issued stablecoins, tokenized assets, and Layer-2 scaling will reshape the competitive landscape over the next two years. Risks remain — regulatory fragmentation, reserve transparency, and issuer concentration could all slow growth — but none threaten the underlying trajectory. For traders, businesses, and investors, the message from 2026 is clear: stablecoins are no longer a crypto sub-sector. They are a parallel global payment system, and their volume curve points decisively up.

FAQs

1. Are stablecoin transaction volume figures inflated by bots and MEV?

Yes, partially. Raw on-chain volume includes automated market maker rebalancing, MEV bot activity, and internal exchange transfers. Visa Onchain Analytics estimates that adjusted "organic" volume is roughly 25% to 30% of raw figures — still around $10 trillion annually in 2026, comparable to Mastercard's total volume.

2. Do stablecoins actually replace Visa and Mastercard at checkout?

Not meaningfully yet. Card networks still dominate consumer point-of-sale payments thanks to chargeback protection, fraud insurance, and universal merchant acceptance. Stablecoins are replacing wire transfers, correspondent banking, and FX settlement — not in-store retail payments.

3. Which blockchain processes the most stablecoin volume in 2026?

Tron leads in transaction count and emerging-market USDT activity, while Ethereum and Solana lead in dollar-value settlement and institutional flow. Base and Arbitrum have grown rapidly for DeFi-driven stablecoin volume, capturing a combined 15% market share by April 2026.

4. Is it safe to hold large amounts in USDT or USDC?

Both issuers publish regular reserve attestations and hold majority reserves in short-term U.S. Treasuries. USDC, regulated under MiCA and the U.S. GENIUS Act, offers stronger transparency guarantees, while USDT provides deeper global liquidity. Diversifying across issuers remains the most prudent approach for large holdings.

5. How do stablecoin fees compare to traditional payment rails?

Stablecoin transfers cost between 0.01% and 0.10% on most chains, versus 1.5% to 3.5% for card payments and $15 to $50 for international wire transfers. On low-fee chains like Tron and Solana, a $1 million stablecoin transfer typically costs under $1 in network fees, compared to thousands of dollars through SWIFT.