FDIC Stablecoin Guidelines: Full Breakdown of the Draft Rules for Bank-Issued Stablecoins

2026/04/19 10:48:37

The global financial landscape reached a pivotal milestone on April 7, 2026, when the Federal Deposit Insurance Corporation (FDIC) released its comprehensive draft rules for bank-issued stablecoins. This move, long-awaited by institutional investors and retail users alike, serves as the regulatory "connective tissue" for the GENIUS Act of 2025 (Guiding and Establishing National Innovation for U.S. Stablecoins Act).

For years, the distinction between a "bank deposit" and a "stablecoin" remained a murky legal gray area. With this latest draft, the FDIC has officially drawn a line in the sand. The proposed framework doesn't just regulate how banks issue digital assets; it fundamentally redefines the relationship between traditional fiat liquidity and the programmable economy. As a 2026 cryptocurrency publisher, we provide this deep-dive breakdown of the FDIC’s "Six Blades"—the core pillars that will determine which banks survive the transition to a tokenized financial system.

Key Takeaways

-

T+2 Redemption Mandate: Banks must facilitate stablecoin-to-fiat redemptions within two business days, effectively ending the era of "liquidity delays."

-

No "Pass-Through" Insurance: Stablecoin holders do not receive FDIC insurance on their tokens, though the underlying bank reserves must be held in highly secure accounts.

-

Yield Prohibition: To prevent competition with traditional savings accounts, issuers are strictly prohibited from offering interest or yield on stablecoin balances.

-

1:1 Reserve Segregation: Issuers must maintain a 1:1 ratio of high-quality liquid assets, with separate pools for each stablecoin brand to prevent "contagion" risk.

-

Attestation Rigor: Monthly public disclosures must be verified by a registered public accounting firm, alongside confidential weekly reports to the FDIC.

The Regulatory Genesis: From the GENIUS Act to FDIC Implementation

To understand the April 2026 draft, one must first look at the legislative foundation laid by the GENIUS Act of 2025. Signed into law on July 18, 2025, the Act mandated that only "permitted payment stablecoin issuers" (PPSIs) could operate within the United States. It effectively created a dual-track system: one for non-bank issuers regulated at the federal level and another for subsidiaries of insured depository institutions (IDIs).

The FDIC’s new draft rules focus specifically on these bank subsidiaries. The agency’s primary goal is to ensure that the issuance of digital dollars does not destabilize the core banking system. By treating stablecoins as a distinct category from traditional deposits, the FDIC is attempting to capture the efficiency of blockchain technology while insulating the Deposit Insurance Fund (DIF) from the inherent volatility of the crypto markets.

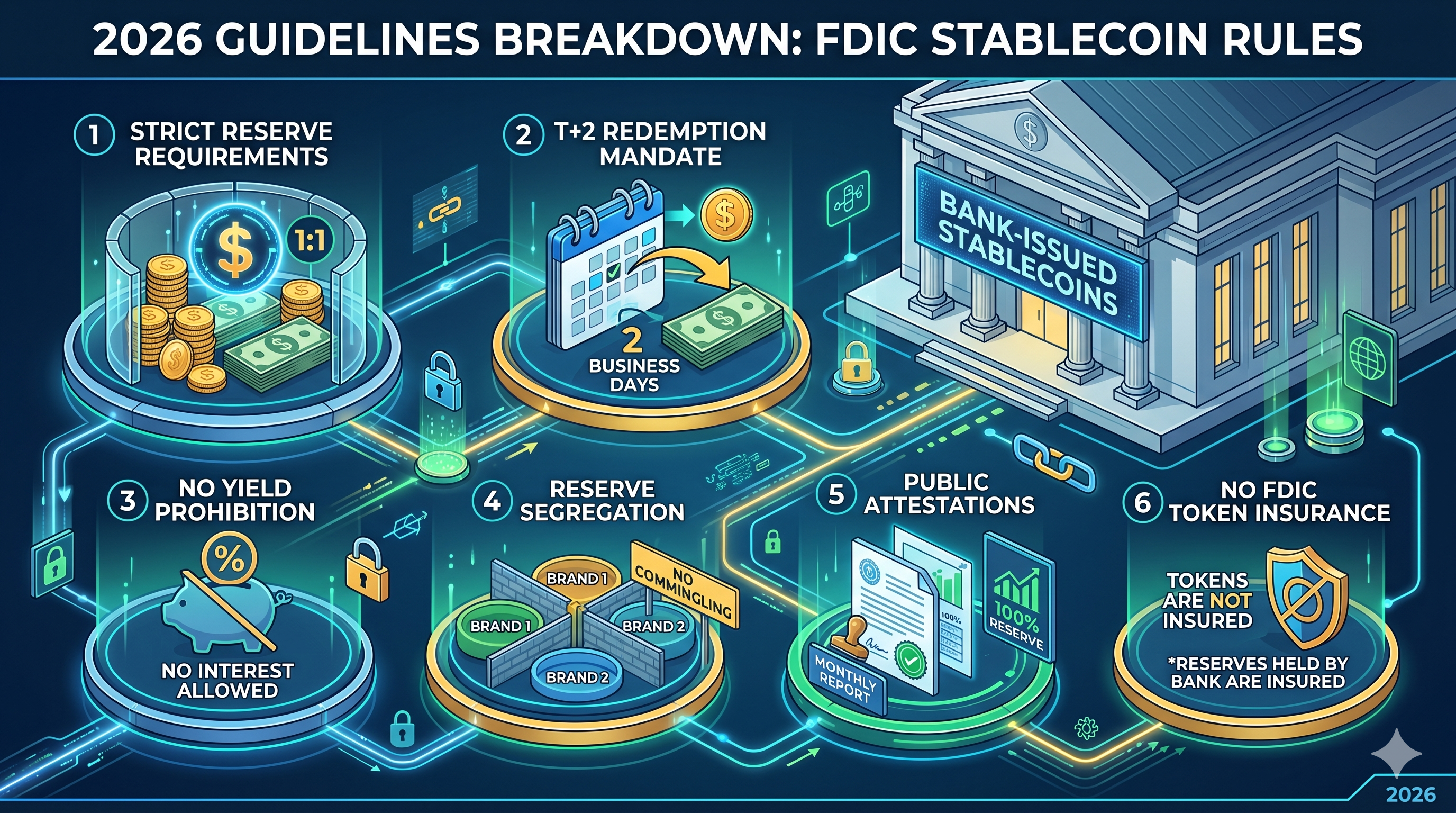

Strict Reserve Requirements and the 1:1 Ratio Mandate

The cornerstone of the FDIC’s proposal is the "identifiable reserve" requirement. Under the draft rules, every single circulating unit of a bank-issued stablecoin must be backed by a corresponding dollar (or dollar equivalent) held in reserve. However, the FDIC has added a layer of granularity that goes beyond previous standards.

If a bank subsidiary issues multiple stablecoin "brands"—for instance, one for retail payments and another for institutional settlement—it cannot commingle the reserves. Each brand must have a dedicated, traceable reserve pool. This "silo" approach is designed to ensure that if one token brand faces a localized crisis or smart contract failure, the contagion does not automatically drain the reserves of the bank's other digital offerings.

Furthermore, the FDIC has taken a hard stance on "re-pledging." Issuers are restricted from using reserve assets for secondary lending or high-risk repurchase agreements. While short-term U.S. Treasuries are permitted, they must remain "unencumbered," meaning they cannot be used as collateral for other bank operations.

The Redemption Standard: Defining Timely Liquidity (T+2)

One of the most significant pain points in the history of stablecoins has been the "redemption bottleneck." During periods of market stress, some issuers have historically struggled to convert digital tokens back into fiat in a timely manner. The FDIC’s April 2026 draft ends this ambiguity by codifying the T+2 standard.

Banks must now publicly disclose their redemption policies, including the exact process and any associated fees. Most importantly, the FDIC mandates that "timely redemption" means completion no later than two business days after the request is submitted. To protect the smallest participants, the FDIC has proposed that the minimum redemption threshold cannot exceed 1 stablecoin. This prevents banks from setting high barriers—like $100,000 minimums—that would effectively lock retail users out of the liquidity pool.

In a move that has sparked significant debate within the fintech sector, the FDIC draft explicitly prohibits issuers from paying interest or yield to stablecoin holders. This rule is designed to maintain a clear distinction between a payment instrument and a savings product.

The regulator’s logic is simple: if stablecoins were allowed to offer competitive interest rates, they would rapidly cannibalize low-cost "core deposits" from traditional banks. This could lead to a sudden flight of capital from the traditional banking system into the digital ecosystem, creating a systemic liquidity mismatch. By capping stablecoins as non-interest-bearing tools, the FDIC ensures they remain optimized for payments and commerce rather than speculative hoarding.

| Feature | Bank-Issued Stablecoin (2026 Draft) | Traditional Savings Account |

| Primary Purpose | Instant Settlement / Programmable Payments | Capital Preservation / Interest Accrual |

| Interest/Yield | Prohibited | Variable / Market Rates |

| FDIC Insurance | No (Insurance applies to bank reserves only) | Yes (Up to $250,000 per depositor) |

| Redemption | T+2 Business Days (Guaranteed) | Immediate (Standard Business Hours) |

| Settlement Speed | Near-Instant (24/7/365) | T+1 to T+3 (Banking Days) |

The Insurance Paradox: Protecting Reserves vs. Protecting Holders

Perhaps the most misunderstood aspect of the new guidelines is the treatment of deposit insurance. The FDIC has clarified that stablecoins are not deposit insurance products. This means that if you hold $1,000 in a bank-issued stablecoin and that specific issuing subsidiary fails, you do not have a direct "pass-through" claim to the FDIC’s $250,000 insurance limit.

However, the deposits that the issuer holds at the parent bank to back the stablecoin are treated as "corporate deposits." While the stablecoin holder isn't directly insured, the reserve assets themselves are subject to the bank’s standard safety and soundness protocols. This distinction is crucial for marketing: banks are strictly forbidden from using the FDIC logo on stablecoin marketing materials in a way that suggests the tokens themselves are insured.

Conversely, the draft clarifies the status of "tokenized deposits." If a bank simply uses blockchain to represent a standard ledger deposit (rather than issuing a separate stablecoin), those assets do retain full FDIC insurance. This creates a clear strategic choice for banks: issue a "stablecoin" for broad interoperability or a "tokenized deposit" for maximum consumer protection.

Reporting, Disclosure, and the Role of Public Attestations

To ensure the 1:1 reserve ratio isn't just a "pinky promise," the FDIC is instituting a dual-reporting structure. This represents a significant increase in the administrative burden for digital asset departments within banks.

-

Weekly Confidential Reports: Issuers must submit detailed balance sheets to the FDIC every week, outlining the exact composition of their reserves and the total volume of tokens in circulation.

-

Monthly Public Attestations: On a monthly basis, banks must publish a reserve report on their official website. Crucially, this report must be reviewed and signed off by a registered public accounting firm.

The "fresh perspective" here is that the FDIC is moving toward a "real-time auditing" mindset. While the current draft requires monthly public reports, insiders suggest the FDIC is building the internal infrastructure to eventually move toward daily, automated reporting via API directly from the bank’s blockchain nodes.

Conclusion: A New Era for Regulated Digital Finance

The FDIC’s April 2026 draft rules mark the end of the "Wild West" for bank-integrated crypto. By establishing clear guardrails for reserves, redemptions, and disclosures, the U.S. government is providing the legal certainty required for massive institutional adoption. While some may find the "no yield" rule restrictive, it is the price of admission for stablecoins to become a core component of the global financial plumbing.

For banks, the choice is now clear: adapt to the high-compliance, capital-intensive model of stablecoin issuance, or risk being sidelined as "tokenized deposits" and "programmable dollars" become the standard for 24/7 global trade.

FAQs

Q1: Are bank-issued stablecoins safer than Tether (USDT) or USDC?

While "safety" is relative, bank-issued stablecoins under the 2026 FDIC rules are subject to much stricter prudential supervision, including T+2 redemption guarantees and mandatory public accounting attestations that Tether is not federally required to provide.

Q2: Can I earn interest on these new stablecoins?

No. Under the FDIC draft and the GENIUS Act, issuers are strictly prohibited from offering interest. Users seeking yield must look toward decentralized finance (DeFi) protocols or traditional savings products.

Q3: What happens if a stablecoin-issuing bank goes bust?

Stablecoin holders have "priority claim" status over other creditors in insolvency proceedings under the GENIUS Act.() While you don't have FDIC insurance, you are first in line to receive the proceeds from the liquidation of the segregated reserve assets.

Q4: How do these rules affect "Tokenized Deposits"?

Tokenized deposits are treated differently. Because they are considered traditional deposits recorded on a blockchain, they retain standard FDIC insurance up to $250,000, unlike payment stablecoins.

Q5: When will these rules go into effect?

The comment period ends June 9, 2026. Final rules are expected by the end of 2026, with a mandatory compliance window for existing issuers likely opening in early 2027.