SK Hynix Nasdaq Listing: Will SKHY Stock Rise or Fall?

2026/07/08 11:04:00

Introduction

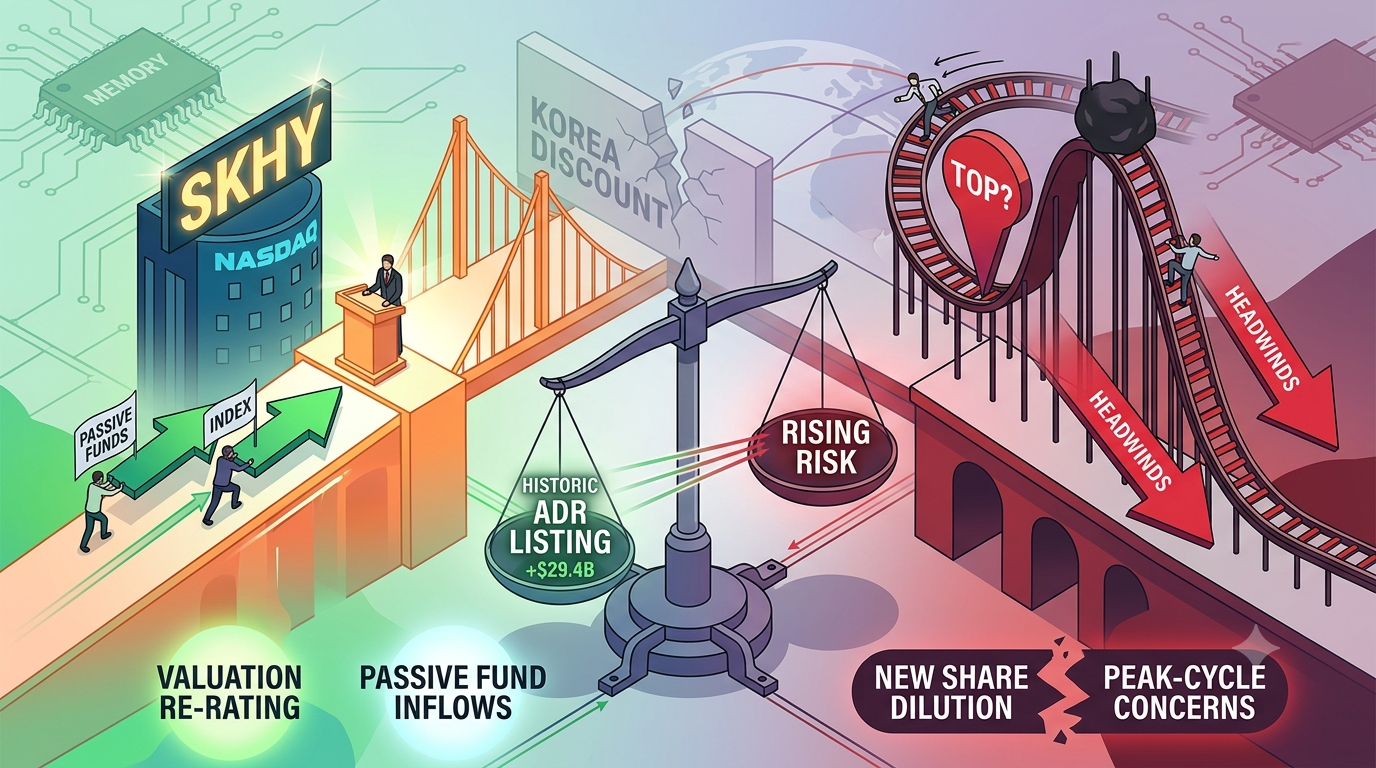

On June 30, 2026, SK Hynix filed an amended F-1 registration with the U.S. SEC to list American Depositary Receipts (ADRs) on the Nasdaq under the ticker SKHY, with trading expected to begin on July 10, 2026. The offering targets approximately $29.4 billion, which would make it the largest ADR listing in history — surpassing Alibaba's $21.8 billion New York debut in 2014.

For investors asking whether this milestone will send SK Hynix stock higher or mark a short-term top, the answer is: the listing creates both catalysts and risks. Near-term upside could come from valuation re-rating and passive fund inflows, but dilution from new share issuance and an already massive 710% twelve-month rally mean the path forward is not without serious headwinds.

What Makes the SK Hynix Nasdaq Listing Historic?

The SK Hynix ADR offering is not merely a fundraising event — it is a landmark moment for the global semiconductor industry. The company plans to issue 17.79 million new shares, representing roughly 2.5% of its 712.7 million outstanding shares, according to its SEC filing. The net proceeds — approximately 45.45 trillion won — are earmarked primarily for capital expenditures tied to new production facilities in Korea, including the acquisition of EUV scanners costing an estimated 11.9 trillion won, to be delivered by December 2027.

The offering is being managed by Bank of America, Citigroup, Goldman Sachs, and JPMorgan as global coordinators. Trading will begin under the ticker SKHY, with 10 ADRs representing one common share of SK Hynix's Korea-listed stock (KRX: 000660). Based on the Korean won closing price of approximately 2,555,000 won on June 24, 2026, the reference price per ADR is roughly $166.

What sets this listing apart is the sheer scale. At $29.4 billion, it comfortably eclipses the previous ADR record and even rivals the largest IPOs ever completed on U.S. exchanges. For context, Saudi Aramco's 2019 IPO raised $25.6 billion. This is a dual listing, not an initial public offering — SK Hynix has traded in Seoul since 1996 — but for U.S. and global investors, it removes a critical accessibility barrier that has suppressed the company's valuation for over a decade.

Will the Nasdaq Listing Boost SK Hynix's Valuation?

Probably — the most compelling bull case centers on valuation discount repair. SK Hynix currently trades at just 6.1x to 6.2x forward earnings based on next twelve months' profits, according to market data from June 2026. Its primary U.S. rival, Micron Technology, trades at approximately 7x forward P/E following a 14% selloff in late June — and as recently as June 22, 2026, Micron's multiple stood above 11x. This persistent gap is what analysts call the "Korea Discount."

HSBC addressed this gap directly in a June 2026 research note, pointing out that over the past 13 years, Micron has traded at an average 35% premium to SK Hynix. The reasons, HSBC explained, have nothing to do with business quality: they are "better access to U.S. investors, more shareholder-friendly policies, and higher beta supported by a smaller earnings base." SK Hynix has been the cheapest AI-adjacent asset in the world, locked inside a Korean-language exchange that most global institutional capital could not easily reach.

HSBC applied a 20% premium to its prior price-to-book estimate for SK Hynix, raising the P/B multiple from 2.8x to 3.4x. The firm upgraded its price target for SK Hynix's Korean shares from 2.9 million won to 4.0 million won — a 38% uplift — explicitly citing the Nasdaq listing as the catalyst. Of 37 analysts covering SK Hynix compiled by Investing.com, 35 rate it a Buy, with an average price target of approximately 3.09 million won.

The logic is straightforward: a Nasdaq listing removes the accessibility discount, not the quality discount. As Dave Mazza, CEO of Roundhill Investments, told Reuters in July 2026, "SK Hynix has been one of the most important companies in the world that most U.S. institutions could not easily own. The listing removes an accessibility discount, not a quality discount."

How Will Passive Fund Flows Affect SKHY Stock?

The ADR listing opens the door to trillions of dollars in passive capital. Once SKHY begins trading on the Nasdaq, it becomes eligible for inclusion in major U.S. equity indexes — most notably the Nasdaq 100 (tracked by the Invesco QQQ Trust, which manages approximately $482 billion in assets) and eventually the Philadelphia Semiconductor Index (tracked by the iShares SOXX ETF and the VanEck SMH ETF).

Mirae Asset Securities estimated in June 2026 that roughly $1.5 billion in new funds could flow into SK Hynix through local ETF inclusions alone. The broader impact could be far larger. Global mega passive funds and public pension funds that are restricted to U.S.-listed securities will, for the first time, be able to establish positions directly. This expands SK Hynix's investor base from regional Korean institutional players to global asset managers on an entirely different scale.

The timeline for index inclusion matters. SK Hynix could be fast-tracked into the Philadelphia Semiconductor Index by late July 2026. Once included, index-tracking funds like SOXX must automatically purchase SKHY shares to match the benchmark weighting — regardless of price. This creates a structural demand floor that did not exist while SK Hynix traded only in Seoul.

What Is the Arbitrage Opportunity Between KOSPI and Nasdaq?

Arbitrage activity between the Seoul-listed shares and the new ADRs will likely exert complex short-term pressure. The ADR-to-common-share conversion mechanism means any significant price gap between SKHY in New York and 000660.KS in Seoul will attract hedge funds running cross-market arbitrage — simultaneously buying the cheaper instrument and selling the more expensive one until the spread collapses.

This "script" has played out before. Both Alibaba and TSMC experienced similar arbitrage dynamics after their U.S. listings, and in both cases, the arbitrage mechanism ultimately helped narrow valuation gaps. For SK Hynix specifically, if the ADR trades at a premium to the KOSPI-listed shares — which is the expected scenario given broader U.S. investor access — arbitrageurs will buy the Korean shares and sell the ADR. This flow typically provides short-term support to the KOSPI mother stock as underlying demand rises.

However, the dynamic cuts both ways. If sentiment sours and the ADR trades at a discount, arbitrage flows reverse — amplifying selling pressure on the Seoul-listed shares. The arbitrage channel also means that any volatility in either market will transmit rapidly to the other, with less friction than before.

What Are the Key Risks Facing SK Hynix Post-Listing?

Despite the bullish catalysts, four major risks could weigh on SKHY stock in the near term.

Supply Shock from New Share Issuance. The $29.4 billion ADR is not a sale of existing shares by current stakeholders — it is a new issuance of 17.79 million shares. This matters because it creates genuine dilution. The company explicitly stated in its SEC filing that it plans to issue new shares worth approximately 45.45 trillion won. This dilution effect will be felt immediately, and more critically, once the new shares officially enter circulation on the Korean market on July 29, 2026, short-term selling pressure on the KOSPI listing could intensify.

Massive Prior Gains Already Priced In. SK Hynix's Korea-listed stock has surged approximately 710% to 770% over the past 12 months, even after a roughly 20% pullback from its June 2026 peak, according to data compiled in early July 2026. Year-to-date, the stock is up more than 220% to 273%, and its market capitalization has surpassed $1.1 trillion. When a stock has already delivered life-changing returns, a U.S. listing can serve as a liquidity event for early holders rather than a fresh buying opportunity for newcomers.

Memory Industry Cycle Risk. The semiconductor memory business is notoriously cyclical, and warning signs are emerging. On July 7, 2026, Samsung Electronics reported preliminary Q2 operating profit that surged 19-fold year-over-year to approximately $58 billion — yet its stock plunged as much as 10% that same day. SK Hynix shares also declined. The reason: Samsung's results revealed that nearly all of its profit came from DRAM and NAND price increases driven by the memory supercycle — this is an industry beta, not company-specific alpha. The market interpreted this as evidence that the entire cycle may be peaking, and investors began re-rating the sector downward. As David Morrison, senior market analyst at Trade Nation, noted following the Samsung report, "Investors are concerned that semiconductor and other AI-adjacent stocks may struggle to maintain such high levels of sales and margins going forward."

Competitive Pressure in HBM. While SK Hynix currently dominates the High Bandwidth Memory market with an estimated 56.4% revenue share as of Q1 2026, according to Counterpoint Research, Samsung is mounting an aggressive counter-offensive. Samsung is shifting half of its HBM production capacity to HBM4 and has halted production of 8-layer HBM3E to focus on next-generation products. Bernstein and TrendForce project Samsung's HBM market share could rise from 27% in 2025 to 37% in 2026, while SK Hynix's share may decline from 56% to 43%. Some analysts predict Samsung could overtake SK Hynix in HBM market share by 2027.

How to Invest in US Stock on KuCoin?

For crypto-native investors seeking exposure to the SK Hynix listing without a traditional brokerage account, KuCoin offers accessible trading instruments tied to traditional equity movements.

KuCoin provides access to a broad range of not only crypto markets, but also stock markets. Now users can also participate in KuCoin's Campaign of Trading US Stock Perps:

-

After complete simple trading missions, users may unlock 100,000 USDT prize pool rewards in TSLA, AAPL, or GOOGL.

Conclusion

SK Hynix's Nasdaq debut under ticker SKHY is a genuine watershed moment — the largest ADR listing in history, opening direct U.S. access to the world's leading HBM supplier at the height of the AI infrastructure buildout. The bull case is built on solid ground: a 20% valuation uplift from closing the Micron discount, billions in passive fund inflows from index inclusion, and arbitrage flows that should support the KOSPI mother stock. The company's fundamentals are extraordinary — 415% expected net profit growth and a 56% grip on the HBM market that feeds directly into NVIDIA's AI chip dominance.

Yet the risks are equally real. The 177.9 million new shares being issued create tangible dilution. The stock has already risen 710% in twelve months, making it one of the best-performing assets on Earth. Samsung's July 7 earnings reaction — a historic profit followed by a 10% stock crash — served as a stark reminder that memory is a cyclical business, and the market is already questioning whether this supercycle has peaked.

For investors, the SK Hynix U.S. listing is neither a guaranteed rocket nor an automatic top signal. It is a complex event where structural tailwinds (valuation re-rating, passive inflows) collide with cyclical headwinds (dilution, peak-cycle pricing, intensifying Samsung competition). The traders who profit will be those who weigh both sides of this equation rather than chasing the headline.

FAQs

What is SK Hynix's Nasdaq ticker symbol?

SK Hynix will trade on the Nasdaq under the ticker SKHY. The company's primary listing remains on the Korea Exchange (KOSPI: 000660), where it trades in Korean won. Each SKHY ADR represents one-tenth of one common share.

When does SKHY start trading on the Nasdaq?

According to the company's F-1 filing with the U.S. SEC, trading is expected to commence on July 10, 2026. This date is tentative and subject to final SEC approval and market conditions.

How much is SK Hynix raising in its ADR listing?

The offering targets approximately $29.4 billion (45.45 trillion won), which would make it the largest ADR listing ever, surpassing Alibaba's $21.8 billion New York listing in 2014.

Why has SK Hynix traded at a discount to Micron for so long?

According to HSBC research published in June 2026, Micron has traded at an average 35% premium to SK Hynix over the past 13 years due to three factors: easier access for U.S. investors, more shareholder-friendly corporate policies, and higher beta driven by a smaller earnings base. The Nasdaq listing directly addresses the first factor.