KuCoin Ventures Weekly Report: Tokenized U.S. Equities Reshape Global Liquidity Gateways Amidst Macro Divergence and Crypto Capital Restructuring

2026/06/01 17:47:00

1. Weekly Market Highlights

RWA Policy Foundations and Exchange-Led Innovation Converge: Tokenized U.S. Equities Accelerate Their Reach into Global Emerging Markets

Last week, market attention around RWA continued to shift from “asset issuance” toward a more front-facing phase defined by tradability, distribution, and global user access. Previously, RWA activity was largely centered on tokenized U.S. Treasuries, money market funds, private credit, and similar asset classes, with its core value reflected in institutional back-office efficiency, compliant custody, and settlement process optimization. More recently, however, the parallel progress of U.S. market infrastructure, exchanges, and crypto platforms has made tokenized equities—especially on-chain U.S. stocks—a more visible entry point for RWA adoption among global users.

This shift is first reflected in the continued acceptance of tokenization by traditional securities market infrastructure. On May 27, DTCC, or The Depository Trust & Clearing Corporation, announced that its DTC Tokenization Service plans to connect with the Stellar public blockchain, with DTC-tokenized assets expected to become available in the first half of 2027. DTC refers to The Depository Trust Company, a core DTCC subsidiary responsible for centralized custody and settlement of U.S. securities, including securities custody, settlement, and related lifecycle management functions. The significance of this development lies not in a single public-chain integration, but in the fact that the tokenization of DTC-custodied assets, corporate action processing, reporting, and cross-chain movement are being incorporated into a more standardized market infrastructure framework. Unlike the traditional model of simply “issuing new assets on-chain,” this path places greater emphasis on connecting tokenized assets with existing securities custody and settlement systems.

From the perspective of U.S. equity tokenization, several parallel paths are currently emerging:

-

A regulated path combining traditional exchanges with the DTC settlement system. For example, Nasdaq has been pushing to support the trading of certain stocks and ETFs in tokenized form under existing market rules, with settlement conducted through DTC.

-

A back-end infrastructure path represented by DTCC, focused on how custodied assets can be standardized into tokenized form, and how corporate actions, reporting, and cross-chain interoperability can be handled.

-

A front-end product path led by CEXs or crypto platforms, which provides users with on-chain economic exposure to U.S. stocks, ETFs, or related assets through regulated brokers, custody arrangements, or third-party issuance structures.

-

A modular trading infrastructure path, where platforms do not necessarily issue assets directly, but instead provide matching, settlement, margin, risk management, and liquidity infrastructure for institutions or developers to build customized RWA markets.

-

An on-chain derivatives exposure path, represented by Perp DEXs such as Hyperliquid. These products do not hold underlying stocks and do not correspond to dividend, voting, or other shareholder rights. Instead, they use stocks, indices, or commodities as reference assets and provide users with 24/7, stablecoin-denominated, and higher-leverage trading exposure through perpetual contracts. Strictly speaking, this path is not tokenized equities, but it shows that on-chain demand for global asset exposure is extending from spot-like mirrored assets to derivatives trading.

Exchange-side product experimentation has also been an important driver of this round of discussion. On May 26, Bitget launched its Reality platform, focused on tokenized U.S. stocks and ETFs. Its rTokens are claimed to be backed 1:1 by real stocks or ETFs, with the underlying assets held through a regulated U.S. broker-dealer, while also supporting the mapping of corporate actions such as dividends and stock splits. Compared with products that only track prices, this structure places greater emphasis on integrating tokenized stocks into the exchange account system and connecting them with margin, strategy trading, and lending modules. Around the same period, OKX launched Exchange OS. Its direction is not to directly issue a specific category of RWA assets, but to modularize exchange capabilities such as matching, margin, clearing, settlement, and risk management, allowing institutions and developers to deploy different types of trading markets on X Layer, including potential future RWA markets. The two approaches represent, respectively, a self-built asset market model and a shared trading infrastructure model. In addition, Binance has previewed a new product launch on June 1. Given earlier reports that Binance had been considering a return to tokenized stock-related business, the market has linked this preview to potential equity exposure products. However, as of now, Binance has not disclosed official product details.

On the demand side, the potential user base for on-chain U.S. equities is mainly concentrated in emerging markets. For users across Asia, Africa, Latin America, and other regions, traditional cross-border securities investment often involves multiple frictions, including account opening, FX conversion, deposits and withdrawals, trading hours, settlement cycles, and local compliance restrictions. Stablecoins, meanwhile, have already become a more familiar gateway to dollar-denominated assets for some users. Once U.S. stocks, ETFs, or other highly liquid assets can be accessed through stablecoin accounts, on-chain wallets, or CEX accounts, the user journey may shift from “FX conversion—brokerage account opening—U.S. stock trading” to “using stablecoins as the funding base to allocate global assets within the same platform.” At the same time, Perp DEX support for stocks, indices, and commodities also shows that some on-chain users do not necessarily seek real securities rights, but place greater value on low entry barriers, around-the-clock access, and leveraged price exposure. This is the core change as RWA moves from an institutional back-office tool toward a global front-end trading product.

For exchanges, the significance of RWA is not merely the addition of new trading pairs, but the opening of a broader product space in which crypto accounts can support multi-asset allocation. In the past, the core assets on CEXs were mainly built around spot trading, derivatives, earn products, and Launchpads, with asset volatility highly dependent on crypto market cycles. With the introduction of tokenized equities, tokenized ETFs, money market funds, and U.S. Treasuries, exchanges may be able to further develop unified margin, portfolio collateral, cross-asset strategies, and regional distribution capabilities. In other words, RWA could become an important tool for CEXs to extend from crypto exchanges toward multi-asset exchanges.

That said, this trend remains at an early stage, and policy and structural risks still require close attention. The core questions around tokenized equities include whether the underlying assets are truly custodied, whether token holders enjoy full securities rights, how corporate actions such as dividends and stock splits are executed, whether secondary market prices may deviate from traditional markets, and how different jurisdictions coordinate rules around securities distribution, KYC/AML, and investor suitability. Especially as demand from emerging markets rises quickly, the tension between “global accessibility” and local securities regulatory boundaries may become a major constraint on the next phase of product expansion.

2. Weekly Selected Market Signals

Macro Divergence and Liquidity Spillover: Crypto Capital Restructuring Amidst the US Stock Market Rally

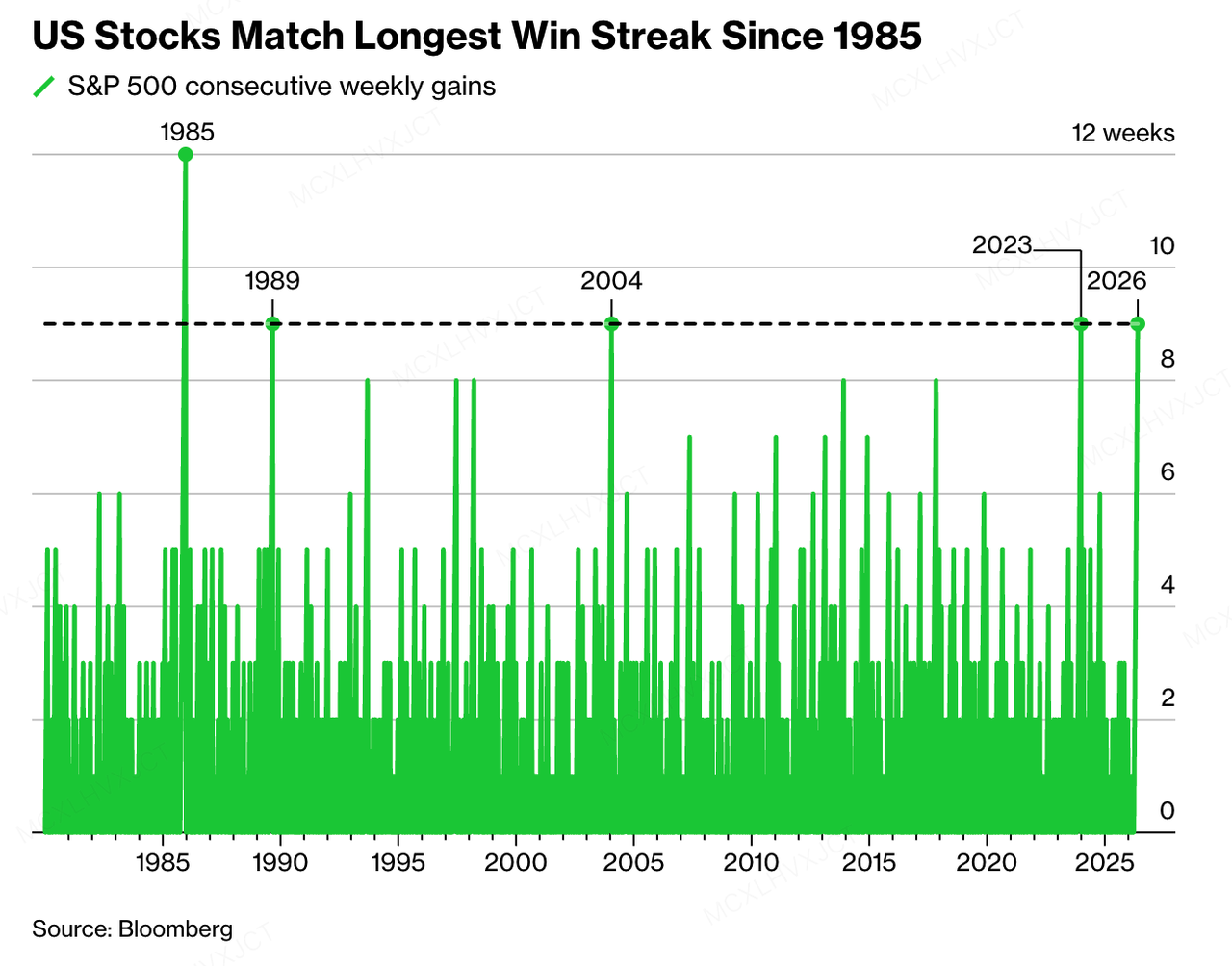

Propelled by the AI investment boom, strong corporate earnings expectations, and geopolitical optimism surrounding Middle East diplomatic negotiations, the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all hit record closing highs this week. Notably, the S&P 500 surged 16% cumulatively across April and May, recording one of its best bimonthly performances in history. Historical data indicates that since 1950, bimonthly surges of this magnitude have only occurred four times, and following each previous instance, the index maintained its upward trajectory over the subsequent six months, with a median gain of 17%. The frenzy triggered by memory chips continues to attract incremental institutional capital, and the technology and semiconductor sectors are expected to potentially maintain their lead in the short term.

However, elevated asset prices exhibit a certain degree of divergence from real-economy macroeconomic fundamentals. On one hand, the US and Iran exchanged proposed amendments over the weekend regarding a draft agreement aimed at extending the ceasefire and opening the Strait of Hormuz. As concrete signs of implementation remain unclear, coupled with heightened geopolitical uncertainties stemming from Israel expanding its ground assault in Lebanon, Brent crude rose 1.3% in response, returning to around $93 per barrel. On the other hand, US Q1 GDP (second estimate) was revised down to an annualized growth rate of 1.6%; consumer confidence in May experienced a slight decline, touching a historic low of 44.8 mid-month, while inflation expectations for the year ahead rebounded to 4.8%.

JPY Weakness and Global Liquidity Spillover Risks

On the liquidity front, the Japanese Yen performed poorly in May, dropping 1.7% for the month and approaching the critical 160 psychological threshold against the dollar. Although Japan's Ministry of Finance deployed a record $73.6 billion for market intervention over the past month, the persistent and significant US-Japan interest rate differential has driven bearish bets on the Yen by leveraged funds and asset managers to their highest levels since July 2024. Market analysis suggests that unilateral market interventions may be facing diminishing marginal returns, and future trajectories might rely more heavily on the Bank of Japan's rate hike actions or hawkish forward guidance at its June 16 policy meeting.

It is worth noting that as a crucial funding currency for global carry trades, the Yen's interest rate trajectory exerts a strong spillover effect on global net liquidity. If the Bank of Japan opts for a higher-than-expected rate hike under exchange rate pressures, it could push up Yen borrowing costs, thereby triggering the unwinding of some cross-border carry trade positions. This potential capital repatriation effect may marginally tighten global liquidity, which could exert downward pressure on the valuations of highly elastic risk assets, such as elevated US tech stocks and crypto assets. Consequently, expectations of a narrowing US-Japan interest rate differential and its cascading effects on global leveraged funds could serve as one of the core indicators for assessing liquidity pressures on risk assets in the near term.

Crypto Secondary Market: Pullback and Liquidity Shifting

The crypto secondary market has recently displayed a sluggish pullback trend, with capital flows largely moving in tandem with broader risk asset preference shifts.

-

Institutional Diversification Effect: Strongly absorbed by core traditional investment narratives such as AI, chip manufacturing, and the reshoring of the US semiconductor industry, incremental institutional capital has exhibited distinct sector rotation. Compared to soaring tech stocks, the allocation share of established mainstream crypto assets among risk-on funds has fallen to a periodic low.

-

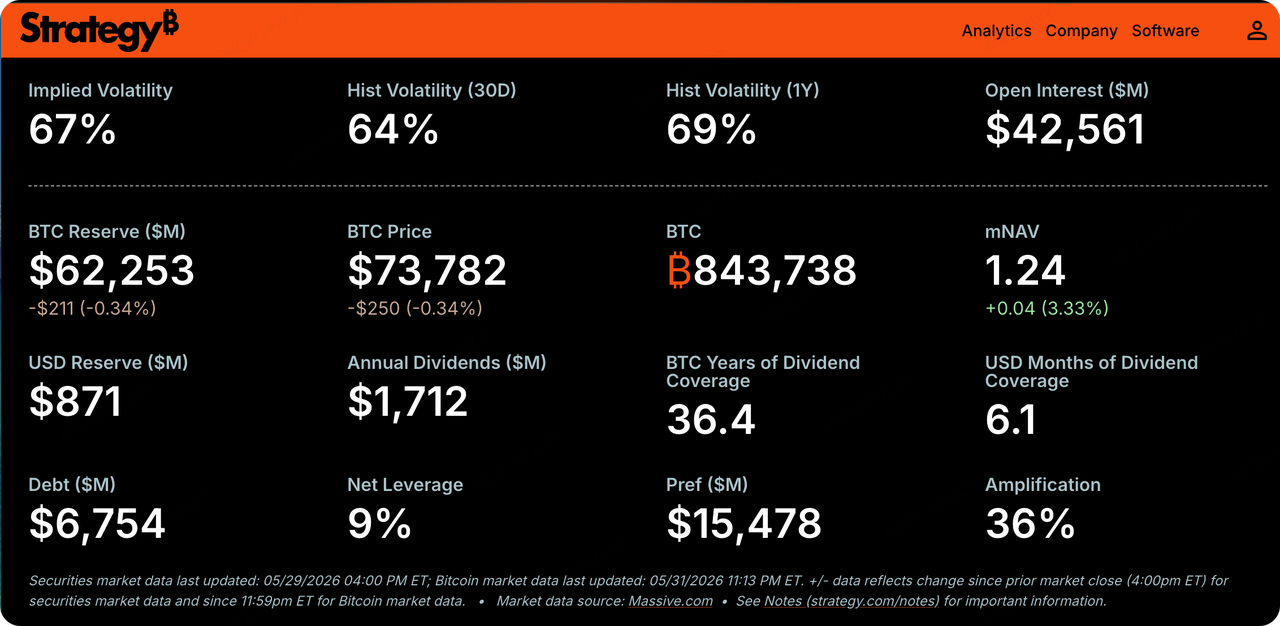

Slowing Pace of Corporate Purchases: MicroStrategy (MSTR), the largest public corporate holder, has noticeably slowed its pace of spot Bitcoin accumulation. Following its Q1 earnings call, the company paused its At-The-Market (ATM) offering mechanism used to raise funds for coin purchases last week. Furthermore, as the trading price of its perpetual preferred stock (STRC) has largely failed to meet the issuance condition of trading near its $100 par value over the past two weeks, related fund-raising and buying operations have temporarily stalled.

Data Source: SoSoValue

Last week, capital flows in crypto spot ETFs experienced a severe correction, indicating a noticeable cooling in institutional demand for Bitcoin and Ethereum exposure. The broader market displayed significant characteristics of structural capital reallocation.

US spot Bitcoin ETFs suffered net outflows for 9 consecutive trading days, with a cumulative scale reaching approximately $2.84 billion, marking the longest continuous bleeding streak since the products launched in 2024. BlackRock's IBIT was the primary source of outflows during this liquidation cycle. Notably, the maximum single-day net outflow reached $723.5 million—ranking as the fifth-largest single-day outflow in spot Bitcoin ETF history—directly flipping the overall capital flow for 2026 from positive to negative. Spot Ethereum ETFs performed equally poorly, enduring capital outflows for 13 consecutive trading days, with cumulative outflows of approximately $694 million, shrinking their total net assets to $11.27 billion.

While mainstream ETFs faced sell-offs, certain XRP spot ETFs and Hyperliquid-related ETFs continued to record net inflows. Among them, the US HYPE spot ETF registered a single-day net inflow of $1.72 million, pushing its total net assets to $122.20 million. Additionally, Grayscale has submitted preliminary ETF application documents to the SEC to establish a fund holding 2 million HYPE tokens, aiming to position itself in the ongoing competition for HYPE-related spot ETFs.

Stablecoin Circulation and On-Chain Liquidity

Data Source: DeFiLlama

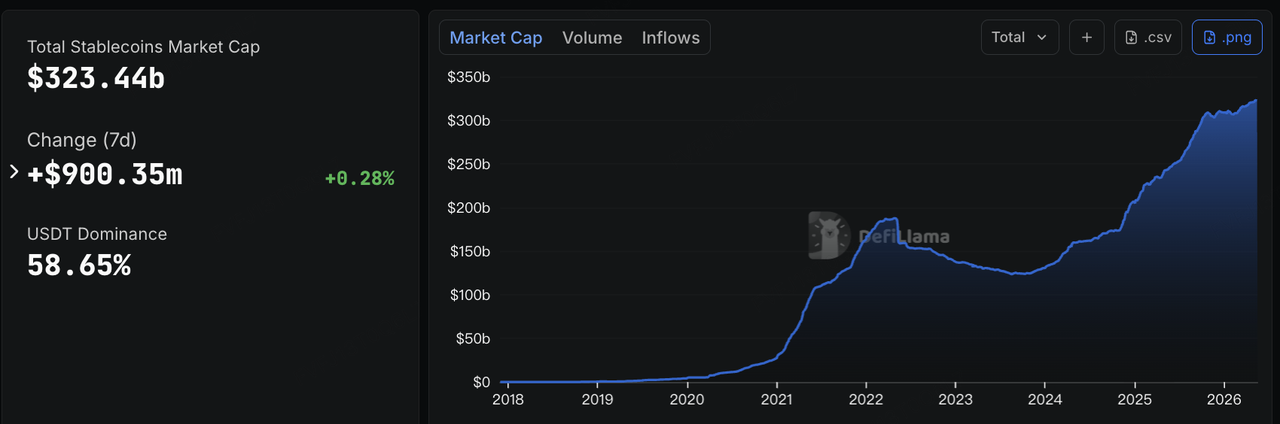

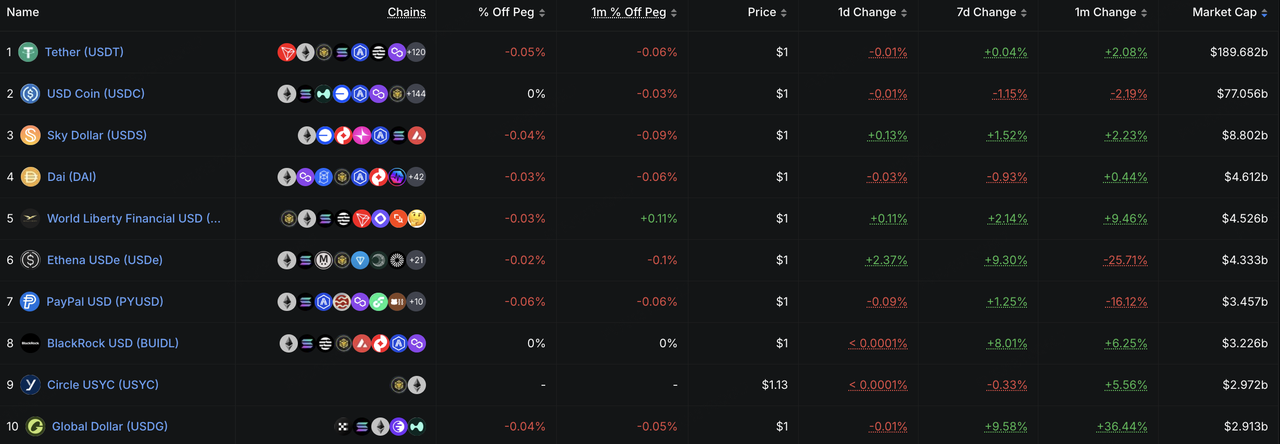

On-chain liquidity demonstrated overall weakness, with total stablecoin market capitalization pulling back in the short term, indicating a temporary lack of purchasing power in the spot market.

The total circulating market capitalization of global stablecoins currently stands at $320.18 billion, reflecting a net decrease of $2.758 billion over the past 7 days (a 0.85% drop). This suggests a certain degree of risk aversion and capital withdrawal intent under the current macro environment.

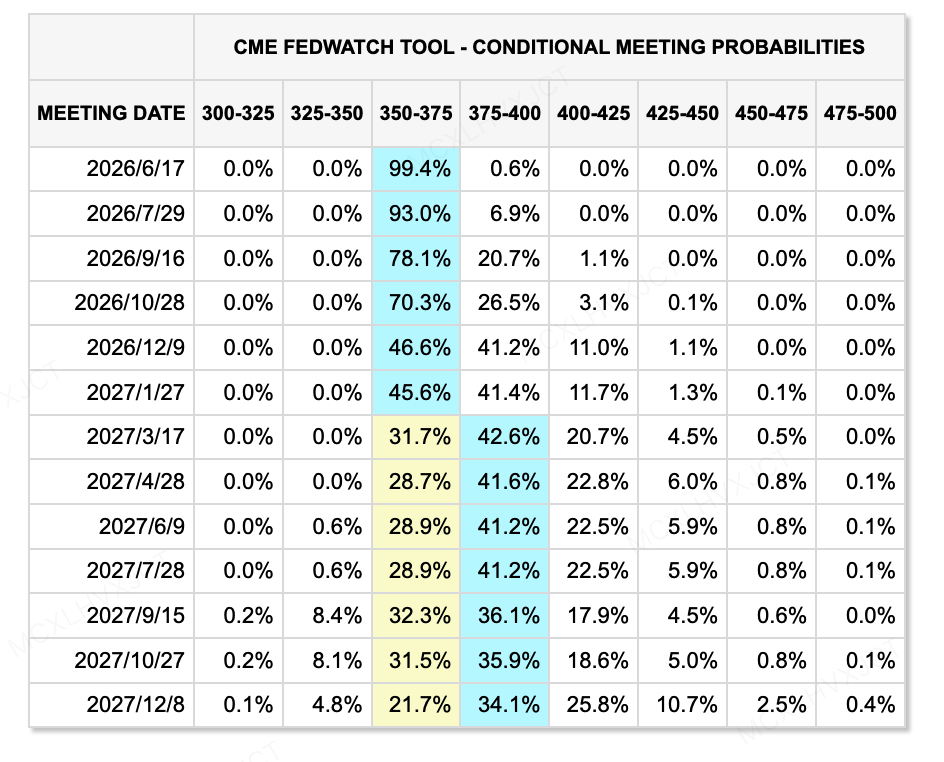

Data Source: CME FedWatch Tool

Federal Reserve Rates and Global Net Liquidity

-

De Facto Financial Tightening: Estimates from mainstream Wall Street investment banks indicate that due to US Treasury yields persistently fluctuating at high levels, the macro financial environment has effectively experienced a "de facto rate hike" of approximately 75 basis points. This has placed significant implicit downward pressure on the valuation anchors of risk assets across the board.

-

New Chair's Term Begins: The new Federal Reserve Chair, Kevin Warsh, was officially sworn in on May 22. The market currently views the mid-June FOMC meeting—his first in charge—as a critical crossroads. After the April CPI touched a three-year high of 3.8%, Warsh's characterization of inflation persistence and potential interest rate adjustment signals may directly influence the asset pricing logic for the second half of the year.

-

Highly Concentrated Short-Term Rate Expectations: According to the latest probabilities from the CME FedWatch Tool, market expectations for the upcoming June 17, 2026 policy meeting show absolute concentration. The probability of maintaining the current interest rate target range is as high as 99.4%, while the probability of holding the same range at the July 29 meeting has reached 93.0%. Treasury traders are currently treating the upcoming Non-Farm Payrolls (NFP) data as a core test indicator to verify whether the Fed might pivot towards a more restrictive policy in the future.

Key Macro/Financial Events to Watch Next Week

-

June 01 (Monday): US May ISM Manufacturing PMI (A leading indicator for core inflation and real economy sentiment).

-

June 03 (Wednesday): US May ADP Employment Change, US May ISM Non-Manufacturing PMI.

-

June 05 (Friday): US May Unemployment Rate, US May Non-Farm Payrolls (NFP) (This data may directly serve as a crucial pricing basis for the Fed's mid-June policy meeting).

-

June 07 (Sunday): OPEC and non-OPEC oil-producing countries (OPEC+) Ministerial Joint Monitoring Committee holds a regular meeting (Its latest stance on oil production quotas could directly intervene in long-term inflation logic).

Primary Market Observations:

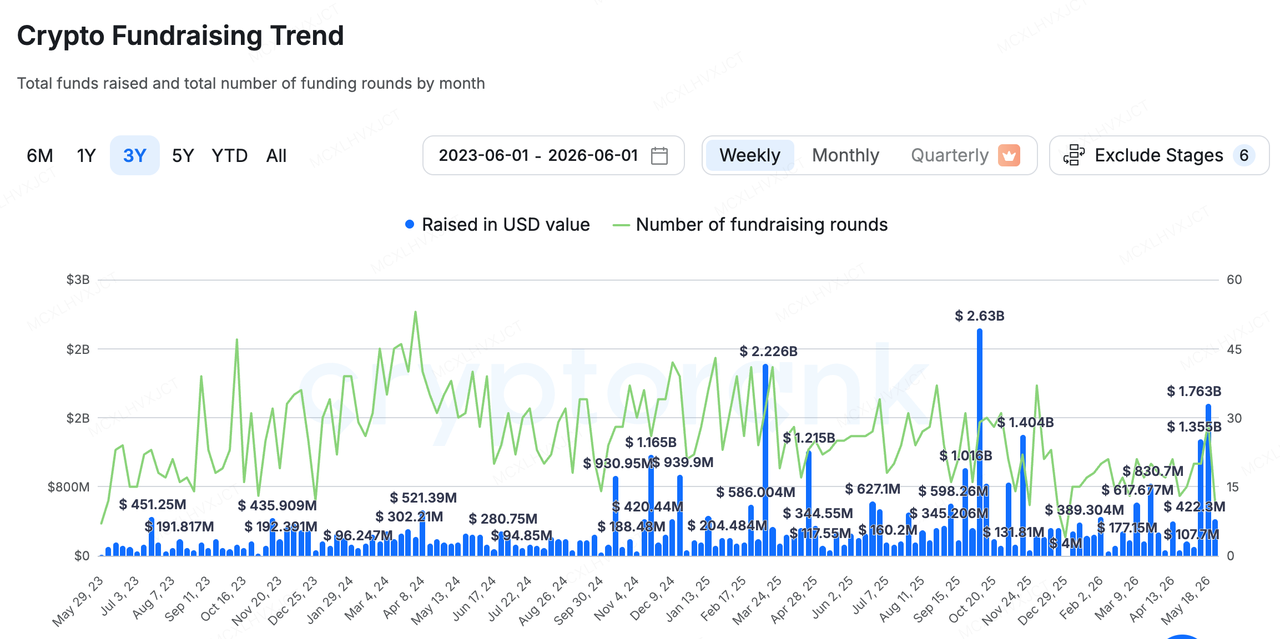

Data Source: CryptoRank

Based on CryptoRank's broad statistical scope, total crypto primary market funding last week was $422 million. Structurally, the market continues to exhibit a significant capital concentration effect, primarily characterized by funds heavily clustering around a few top-tier compliant infrastructures and licensed trading platforms. Concurrently, late-stage M&A and strategic integration activities have experienced a periodic uptick (e.g., the successive acquisitions of Rarible, Flybit, GAMEE, and zkPassport).

This may indicate that in the current macro liquidity environment, primary market capital is relatively restrained in scattering investments across the application layer; instead, it prefers to seek defensive certainty in core sectors with licensing and channel dividends via M&A or strategic capital injections.

This week, the most critical structural highlight in the primary market centered on the South Korean compliant crypto ecosystem. Capital flows presented an exceptionally rare contrast narrative: "Retail Pivots Left, Institutions Pivot Right".

-

Massive Diversification and Shifting of Retail Capital: According to market data, the Korea Composite Stock Price Index (KOSPI) demonstrated strong unilateral upward momentum in 2026, with cumulative year-to-date gains exceeding 94%. The immense wealth effect of the traditional stock market has heavily attracted the attention of local retail investors, leading a massive amount of highly risk-on domestic retail capital to exit the secondary crypto market and flow into traditional equities to chase asset dividends.

-

Reverse Positioning by Traditional Finance and International Capital: During this window of retail capital exiting the crypto market, domestic South Korean traditional finance giants and top-tier global crypto venture funds are inversely accelerating their deep equity restructuring and gateway lock-ins of local licensed crypto infrastructures at scales of hundreds of millions of dollars:

-

Channel Penetration by Traditional Brokerages: Dunamu, the parent company of South Korea's largest digital asset exchange Upbit, closed a $204 million strategic funding round from traditional brokerage Samsung Securities, pushing its post-money valuation directly to the $10.2 billion level.

-

Regional Defensive Positioning by International Compliant Capital: On May 29, OKX Ventures and leading South Korean traditional finance firm Korea Investment & Securities (KIS) officially announced their joint acquisition of 19.6% (approx. 20%) stakes each in Coinone, South Korea's third-largest crypto exchange. Pending compliance reviews by relevant regulatory agencies, KIS and OKX Ventures will jointly become Coinone's third-largest shareholders.

-

During this cooling period for retail trading sentiment, traditional financial institutions are leveraging the opportunity presented by equity restructurings in licensed exchanges to conduct counter-cyclical asset reorganizations. These intensive crypto deployments by institutions are likely forward-looking bets on future compliant digital expansions centered around KRW stablecoins and RWAs, while concurrently aiming to complete strategic defenses of core fiat-to-crypto gateways.

When retail enthusiasm fades, the infrastructure value of exchanges in compliant circulation, customer reach, and clearing gateways becomes even more prominent. In the future, the South Korean digital asset market is expected to gradually transition away from the isolated ecosystem previously dominated purely by retail sentiment, evolving instead into an institutionalized consortium model jointly participated in by banks, brokerages, internet tech giants, and licensed exchanges. Throughout this process, the equity ownership of licensed fiat channels may become one of the core variables in the distribution of digital financial competitiveness in the Asia-Pacific region.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.