Author: Ilya Strebulaev

Compiled by Deep潮 TechFlow

Shenchao Summary: This is the first publicly released lecture note from Stanford Graduate School of Business’s VC course. The author has taught this course for many years, with over 500 of the 1,300 students going on to start their own ventures and 600 entering the VC industry.

He decided to fully open the course content, starting with the most fundamental and commonly misunderstood cash flow provisions—convertible preferred stock, liquidation preferences, and conversion rights—terms that determine exactly how much founders receive upon exit.

This is essential reading for founders who are planning to raise funds or are already in discussions.

The full text is as follows:

This article will explain how cash flow provisions work, how liquidation preferences impact your returns, and how convertible preferred stock gives investors an advantage.

These are fundamental concepts that entrepreneurs should understand.

Welcome, and my motivation

I have been teaching a venture capital course at Stanford Graduate School of Business for many years. Over this time, more than 1,300 students have taken the course, about 500 of whom went on to found startups, and approximately 600 entered the venture capital (VC) and broader private equity industry as investors. I stay in touch with many of them and frequently receive emails or messages saying, “Professor, I’ve pulled up your lecture notes and slides again—I’m raising funds or negotiating a term sheet.”

I’ve always wanted to broadly share my knowledge and experience, especially because the world of venture capital and entrepreneurship is often shrouded in mystery and widely misunderstood. That’s why I began posting VC insights on LinkedIn almost every day. But to delve into the details of a complex and challenging subject—where concepts build upon one another layer by layer—requires a different medium. So, I’m here.

After reading each article, you should have a solid understanding of how investors make decisions, how entrepreneurs and investors negotiate cash flow allocation and corporate governance, and numerous other everyday matters in the startup world.

In the initial articles, we will dive straight into the core, focusing primarily on cash flow provisions in the first-round VC financing. Cash flow provisions are essentially the rules that determine "who gets what" when slicing up the pie. We will introduce the most commonly used financial instrument in VC financing—convertible preferred stock—and cover all the major contractual terms that determine how returns are allocated between founders and investors. After thoroughly covering first-round VC financing, we will move on to subsequent rounds. Only then will we be prepared to discuss pre-VC rounds, including instruments such as SAFEs and convertible notes. Many students ask me why we don’t start with SAFEs—after all, these are the securities many founders issue first. But the key feature of a SAFE is that it converts into securities the startup will issue later; without understanding those future securities, it’s difficult to truly grasp the SAFE. After covering cash flow provisions, we will turn to control, corporate governance, and conflicts of interest within startups—absolutely critical topics. As I repeatedly tell my students, “You can only lose control of your startup once. Once it’s gone, it’s gone forever.”

Typical case

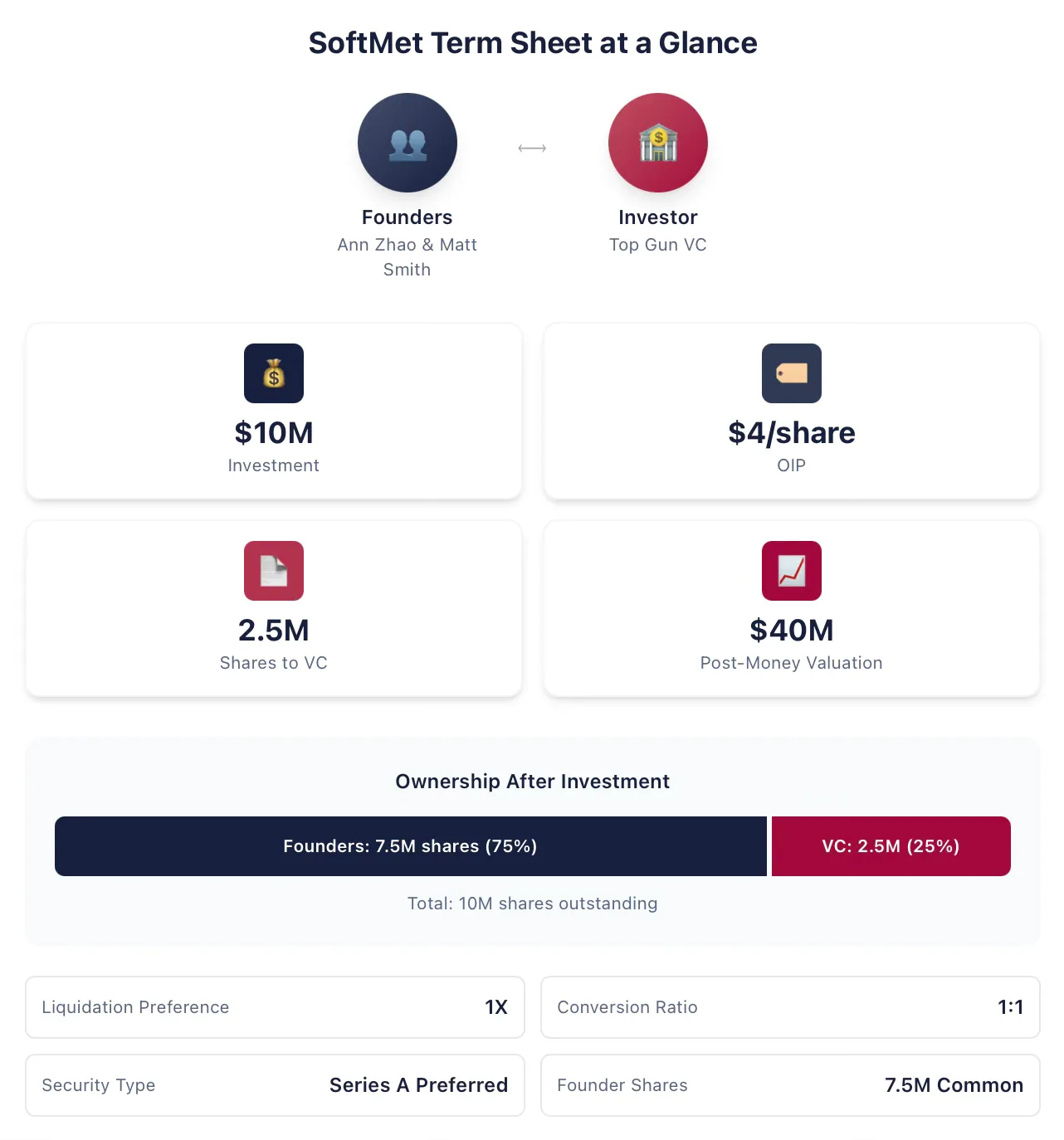

When explaining the topic of cash flow, I will use a consistent case study that is modified and expanded as the content progresses. Ann Zhao and Matt Smith are co-founders of SoftMet, a technology startup. During the fundraising process, they met Rob Arnott, a partner at the leading venture capital firm Top Gun. Rob subsequently invited Ann and Matt to present their startup idea to all partners at Top Gun. A week later, the founders received a term sheet from Top Gun. The term sheet proposes:

Top Gun invested $10 million in SoftMet.

Top Gun received Series A preferred shares from SoftMet at an issuance price (original issue price) of $4.

Series A preferred stock has a 1x liquidation preference.

One share of Series A preferred stock is convertible into one share of SoftMet common stock.

Series A preferred stock comes with various additional terms and conditions.

The founder holds 7.5 million common shares.

The company's post-money valuation is $40 million.

Ann and Matt need to understand the meaning of this term sheet: What exactly is Series A preferred stock? What is post-money valuation? What is liquidation preference? What is conversion? Which features should they pay special attention to in this proposal? Among all the terms, which ones may have significant financial implications that they might want to renegotiate? Which terms are more founder-friendly?

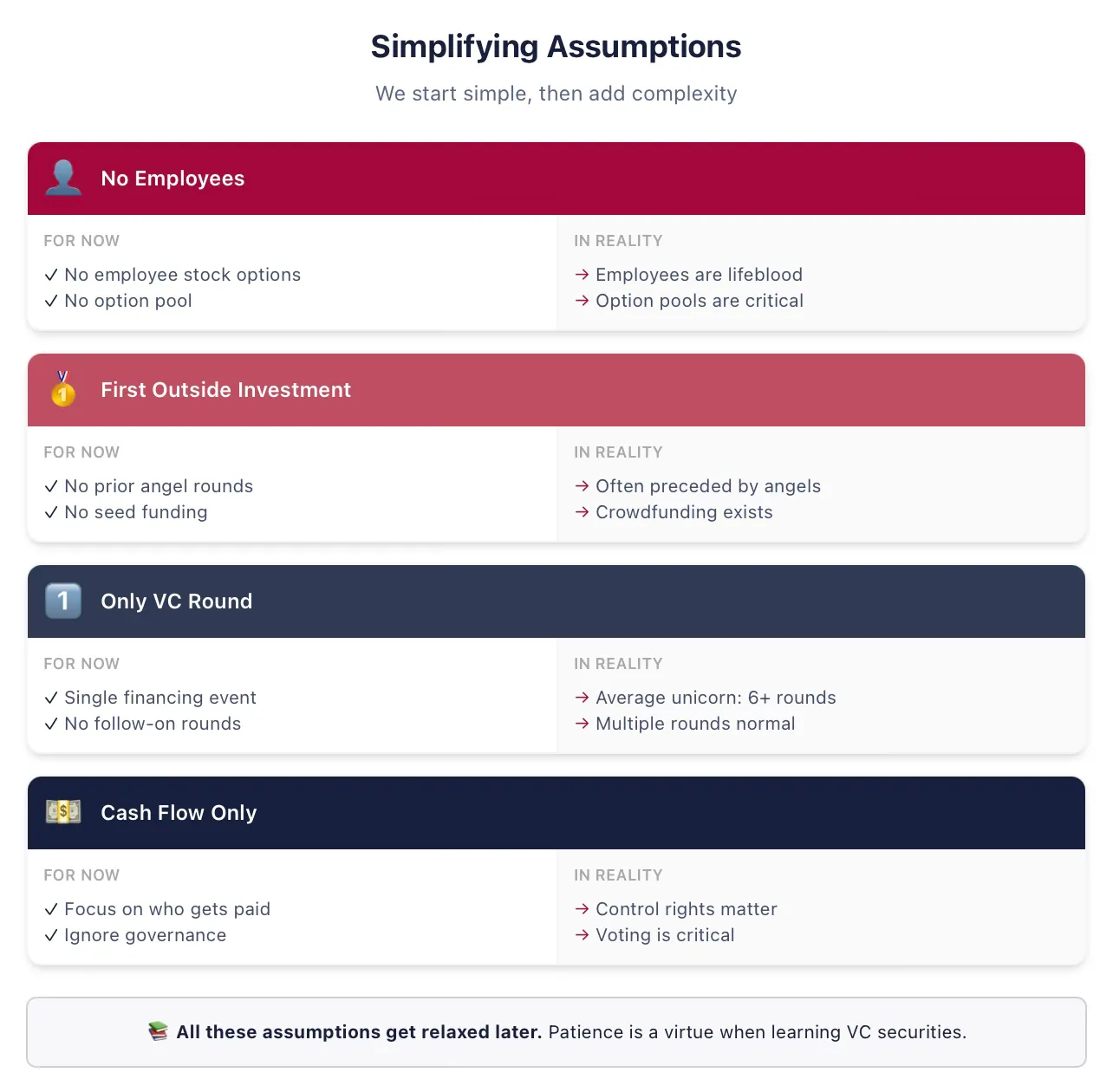

We need to make some simplified assumptions to introduce all the concepts.

To keep things clear, we’ll start with some simplified assumptions. We’ll relax all these temporary assumptions in later lectures—stay tuned! Don’t leave because you think, “This ivory tower professor doesn’t know that founders don’t ‘hold shares’ but ‘vest’ etc.” I know, and we’ll come back to all of this at the right time.

Below are the assumptions I will consistently use in the introductory materials on the first round of VC funding (if these terms are unfamiliar, this is precisely why we are simplifying them now):

Assumption: SoftMet does not employ any employees. This assumption means that SoftMet does not need to compensate employees with cash or stock, and that the founders are regarded solely as owners, not employees. Vesting schedules and founder employment terms will be discussed later.

Assumption: Top Gun is SoftMet’s first external investor. In reality, most VC rounds are preceded by angel or seed rounds using different securities.

Assumption: This round of funding will be the only investment SoftMet raises as a privately VC-backed company. In reality, my research shows that the average U.S. unicorn has raised over six rounds of VC funding. We will certainly relax this assumption soon.

Assumption: Only cash flow terms matter. The term sheet also covers corporate governance—control, voting rights, board seats—but we’ll address these later.

Investors receive returns on their investments in exchange for financial securities.

Top Gun's $10 million investment is a venture capital round—cash exchanged for securities. The $10 million that Top Gun proposes to invest is called the investment amount.

As compensation for its investment, Top Gun will receive securities granting it partial ownership of SoftMet. Specifically, as part of this round, a certain number of new securities—Series A preferred shares—will be issued to Top Gun. But how many shares will Top Gun receive? How will ownership percentages be allocated after Top Gun’s investment? How will future proceeds be distributed between the founders and the VC investor?

The term sheet provides clues to these questions by outlining who gets what under different scenarios. The number of shares Top Gun receives is determined by the investment amount and the original issue price of the Series A preferred shares. The original issue price is the price per share paid by investors at the time of issuance, commonly abbreviated as OIP, and may also be referred to as the original purchase price (OPP).

Note: OIP differs from par value. Par value is the arbitrary stock value stated in a company’s articles of incorporation at the time of registration and has little to no relation to the company’s actual valuation, carrying no real economic significance. Common par values are $0.001 or $0.0001, or “no par value” may be used.

We can use the OIP to determine the number of shares Top Gun received. With an investment amount of $10 million and an OIP of $4, Top Gun received the quotient of the two:

Therefore, Top Gun invested $10 million in cash in SoftMet in exchange for 2.5 million shares of Series A preferred stock. More generally, the relationship among OIP, the investment amount, and the number of shares acquired by investors in this round is as follows:

Once you know any two of these three values, you can determine the third. Real-world term sheets vary significantly in how they describe proposed investments, but they should always allow you to back into these three values from the given information. SoftMet’s term sheet provides the investment amount and the OIP. Alternatively, the term sheet might provide the investment amount and the number of shares the investor receives.

Example 1: Original issuance price

The VC fund Great Innovation Partners invested in the early-stage company Fox Solutions, Inc., acquiring 2 million shares of seed-stage preferred stock for an investment of $25 million. What was the original issuance price of this security?

Original issuance price:

In other words, Great Innovation paid $12.50 per share for the seed round preferred stock.

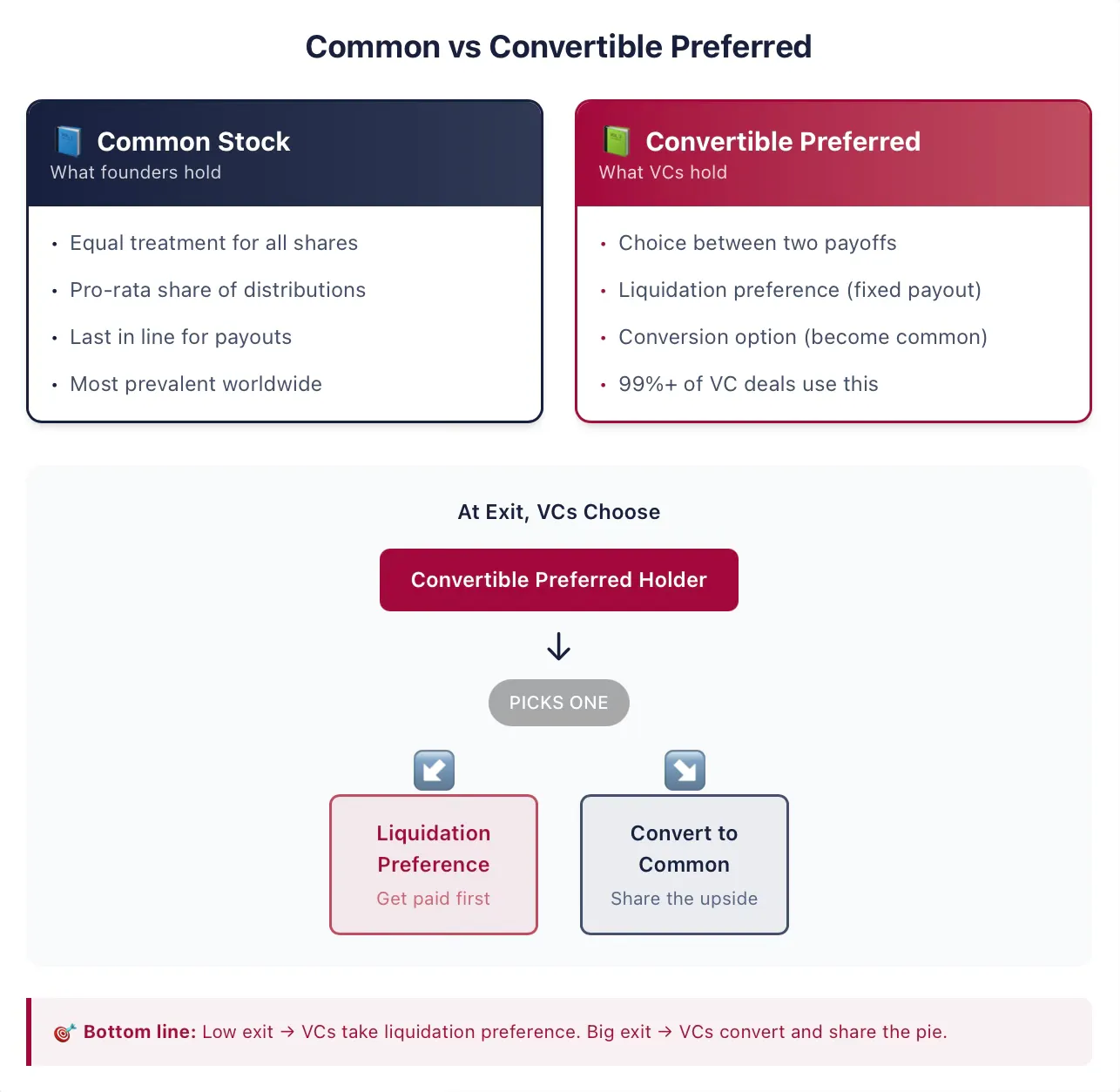

Founders typically hold common shares.

Founders of early-stage companies typically hold common stock, the most prevalent form of ownership in both publicly listed and private companies worldwide. Stock is a form of company ownership that grants its holders—known as shareholders—certain rights. In other words, shareholders have a claim on the company. The term "equity" is also commonly used to describe this claim, and we will use "stock" and "equity" interchangeably here. The terms "stock" or "equity" also distinguish these securities from another common type of corporate claim: debt.

The term "common" in "common stock" only has meaning when a company has issued other types of securities. If common stock is the only security issued by the company, then each share of the company’s stock is treated equally—there is only one class of claim! More generally, each share of common stock is treated exactly the same as any other share of common stock.

When dividends are distributed, each common share is entitled to receive exactly the same dividend as any other common share. Therefore, dividends are distributed equally among all outstanding common shares. However, if other holders own a different type of security, the distribution of dividends may be significantly different. In VC transactions, this is almost always the case.

Investors hold convertible preferred shares.

The Series A preferred stock received by Top Gun is an example of convertible preferred stock. Convertible preferred stock is the type of security chosen by the majority of U.S. venture capitalists. This security combines characteristics of both debt and common stock. Unfortunately, for aspiring entrepreneurs or early-stage investors, the structure of this security is relatively complex, especially when compared to traditional financial instruments like direct debt and common stock. Fortunately, we will now master it together.

At its core, convertible preferred stock is a financial security that gives holders the option to choose between two potential payout scenarios. Holders can elect to convert the convertible preferred stock into another security, typically common stock (known as the conversion option). Alternatively, holders may receive a one-time payment before common shareholders receive any proceeds (known as the liquidation preference). This right often comes with numerous additional conditions and depends on many other contractual terms we will explore. But the fundamental idea is that this security grants investors the right to choose between the conversion feature and the liquidation preference feature.

One very important point—especially for those with experience in stock markets and investment banking—is that in traditional financial markets, companies sometimes issue securities known as preferred stock. Although they may appear similar on the surface, securities issued in VC transactions have many characteristics that make them fundamentally different from preferred stock in public markets. If you’re familiar with preferred stock from public markets—this is different. Don’t skip this section.

Example 2: Preferred shares issued by a publicly traded company

In 2018, the large publicly traded insurance company MetLife issued a new series of preferred shares, MET-E, offering 28 million shares to the market. This type of preferred stock functions similarly to debt securities, providing investors with a permanent fixed dividend. MET-E offers investors a coupon rate of 5.63% but grants no voting rights (unlike common stock). Preferred shareholders have priority over common shareholders in receiving dividends from company earnings (though after creditors). Preferred shares such as MET-E typically do not have conversion features.

VC agreements typically refer to this type of security as preferred stock, but when you see preferred stock in a VC agreement or term sheet, you can safely assume it is also convertible. In my analysis of thousands of VC agreements, over 99% of "preferred stock" is actually convertible.

Although the term "convertible" is often omitted from the security's name, other additional terms are typically included. For example, the security may be named Series A Preferred Stock, as in the case of Top Gun’s proposed investment.

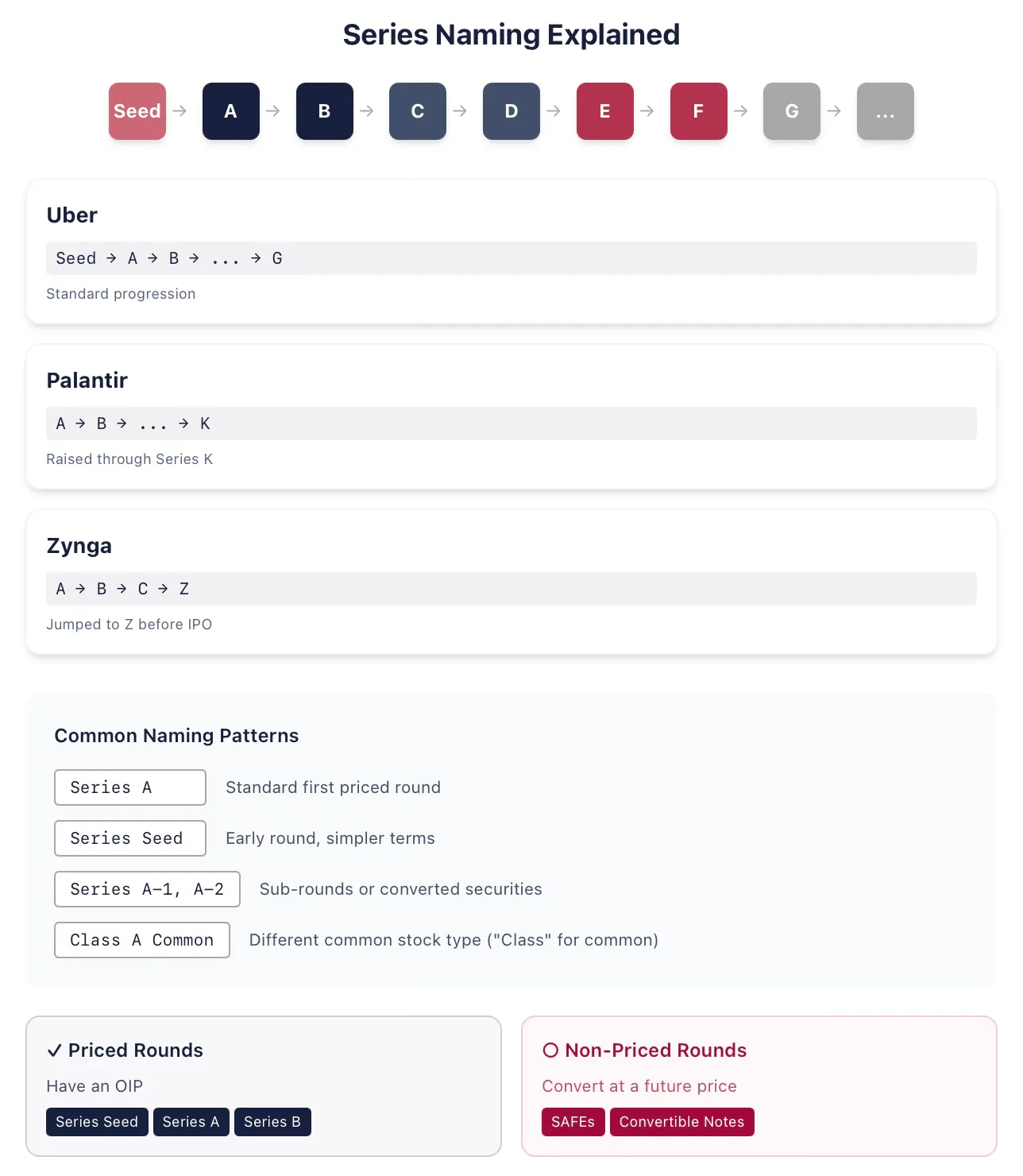

Example 3: Series Letters

Ride-sharing company Uber sequentially issued seed, Series A, Series B, and other rounds of preferred stock up to Series G during its private venture capital-backed phase. Big data analytics firm Palantir issued Series K preferred stock in its 2015 funding round, having previously issued Series A through Series J. Space company SpaceX will likely exhaust all letters in naming its various series of preferred stock before its eventual IPO (I am writing this in January 2026). Sometimes, companies issue securities out of alphabetical order, such as during corporate restructurings. For example, online gaming company Zynga issued Series A, Series B, and Series C preferred stock, then skipped ahead to issue Series Z preferred stock just before its IPO.

Historically, Series A preferred stock was the name given to the securities issued in a company’s first round of venture capital financing. Over the past fifteen years or so, the first securities issued have often also been called seed preferred stock (as in Uber’s case). This typically means that the structure of these securities may be simpler than that of a full Series A preferred stock. Founders and investors may also wish to signal that the company is still in a very early stage. Once the company completes another financing round, Series A preferred stock is typically issued. This means you should not assume that “Series A” necessarily indicates the first round of venture capital financing.

So what is a Series A venture capital round? The best way to determine this is to ask whether the round is a priced round—that is, whether the securities have a fixed price. If the company issues a SAFE or convertible note, it is not a priced round; however, seed preferred stock is a priced round. (Note: You often hear that unpriced rounds do not set any valuation for the company. This is incorrect, and we will address this at the appropriate time.)

Lawyers advising VC investors and startups are quite creative in naming, resulting in many other variations. Sometimes, these subtle naming differences reflect specific arrangements. For example, any series may be followed by or accompanied by additional numbered series (e.g., an A round may be followed by an A-1 round, A-2 round, etc.). When these are part of the same round, A-1 shares typically differ from A-round shares only in certain specific terms; otherwise, they are identical, often because some outstanding securities have been converted into (nearly equivalent) A-round shares. Alternatively, they may belong to entirely different financing rounds—for instance, because the company feels it has not yet reached the milestones expected of a B-round company in its sector.