The Digital Ruble Goes Live on September 1: What Changes for Russians and Businesses

2026/07/14 11:32:00

Bank of Russia Governor Elvira Nabiullina stated: "Everything is ready for the widespread use of the digital ruble" — systemically important banks and major trading enterprises must connect to the platform, and according to her, all participants are already prepared. Starting September 1, 2026, this is no longer a pilot but a mandatory stage: the largest banks are required to open digital wallets for customers, while trading companies with revenue over 120 million rubles must accept payment in the new form of the national currency. The digital ruble is a third form of money alongside cash and non-cash rubles, with the same denomination, the same issuer, and no exchange-rate difference whatsoever between the forms. Below we break down exactly what changes for citizens and businesses from September 1, who is required to connect first, how well personal data and transfers are protected, when offline payments will appear, and how much businesses can save on fees.

How Does the Digital Ruble Differ From Money on a Bank Card?

The main difference between the digital ruble and money on a bank card is the form of obligation. Money on a card represents a debt owed by a specific commercial bank to the client: if the bank loses its license, the depositor receives compensation through the deposit insurance system, but only up to the established limit. The digital ruble works differently — it is held directly on the Central Bank's platform, and the servicing bank merely provides access to that platform through its mobile app. This means the bankruptcy or license revocation of a specific bank has no effect on the safety of the funds: they are not physically tied to a commercial organization's balance sheet.

The digital ruble is a digital form of legal tender, not a corporate bonus, gift certificate, or an in-house currency with a limited shelf life. It has no "expiration date" — it doesn't burn off, doesn't zero out, and doesn't lose value over time, unlike accumulated loyalty points. There is no exchange-rate difference between cash, non-cash, and digital rubles in principle — one digital ruble always equals one ordinary ruble, and converting between forms carries no loss and no conversion fee.

Technologically, each unit of the digital ruble receives a unique digital code that makes it possible to trace its movement at every stage — from the moment the Central Bank issues it to its final use by a buyer. The platform's developers note that this feature is meant to make money laundering through chains of shell accounts harder and to significantly simplify tracing funds in cases of fraud, theft, or unauthorized withdrawal — the transaction can be traced back to a specific recipient.

From a user-experience standpoint, the digital ruble works through the familiar banking app: there's no need to download separate new software, as the wallet is integrated into the existing mobile-banking interface. Transfers between digital wallets at different banks happen instantly and free of charge for individuals, making the tool a convenient counterpart to the Faster Payments System — but with direct accountability resting with the central regulator rather than a commercial entity.

Which Banks and Companies Must Connect Starting September 1, 2026?

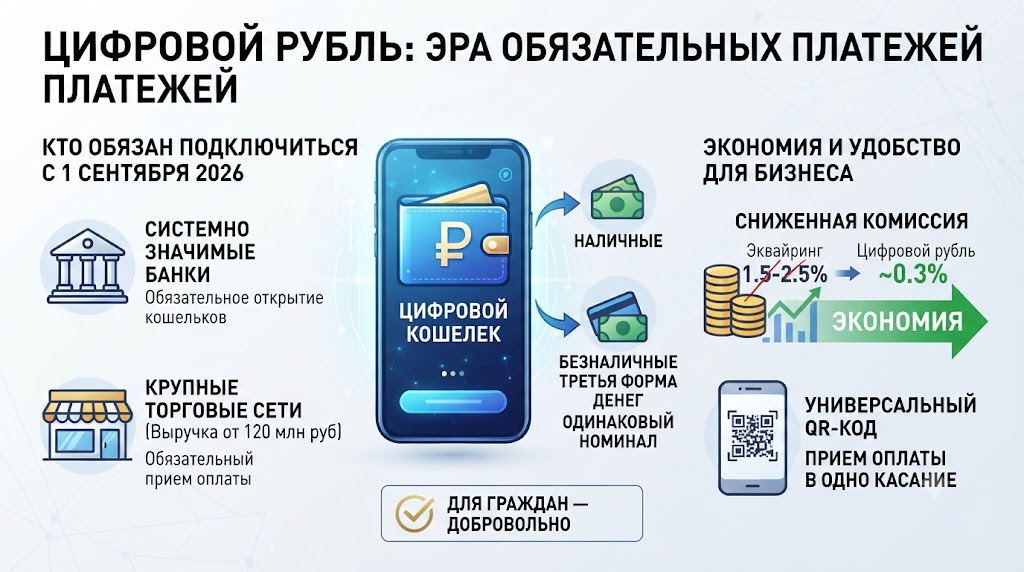

Systemically important banks and the large businesses tied to them are the first required to connect to the platform. The requirement applies to trading companies that had a merchant-acquiring agreement with one of these systemically important banks as of January 1, 2026, and have annual revenue of 120 million rubles or more. This is the group of participants Nabiullina was referring to when she noted full readiness for the September 1 launch.

The rollout schedule stretches several years ahead and is tiered by business size. Starting September 1, 2027, the requirement will extend to banks with a universal license and to companies with annual revenue from 30 million rubles — that is, mid-sized businesses. Small businesses and sole proprietors can connect voluntarily for now, with full coverage of the retail market, including small points of sale, planned closer to 2028.

For ordinary citizens, nothing mandatory is being introduced at this stage. Use of the digital ruble by individuals remains voluntary: a person can choose to open a wallet, transfer funds into it, and pay with digital rubles entirely at their own discretion, while the new law's obligations fall specifically on banks and merchants, who must technically enable this payment option for any customers who choose to use it.

An important practical point for businesses is that integration does not require replacing checkout hardware. In most cases, it's enough to update the point-of-sale software and enable acceptance of the universal QR code through the servicing bank, after which the till can accept payment via multiple methods — card, Faster Payments System, and digital ruble — without installing additional terminals.

Below is a quick summary of the connection timeline to make it easier to see when the requirement applies to a specific business.

| Date | Who Must Connect |

| September 1, 2026 | Systemically important banks; trading companies with revenue from 120 million rubles serviced by these banks |

| September 1, 2027 | Banks with a universal license; companies with revenue from 30 million rubles |

| September 1, 2028 | All remaining sellers regardless of revenue; small businesses connect voluntarily until this date |

This phased approach lets the regulator and the market gradually adapt the infrastructure without placing an instantaneous burden on every bank and trading network at once, and it gives small businesses extra time for voluntary testing of the tool before the mandatory stage arrives.

How Well Protected Are Data and Transfers in the Digital Ruble?

The Bank of Russia has consistently insisted that the digital ruble does not create a tool for "total surveillance" of citizens. Information about accounts, balances, and completed transactions is protected by banking secrecy law in exactly the same way as data on ordinary non-cash transfers via card or account — meaning access by third parties without legal grounds is formally excluded. The regulator emphasizes that the level of confidentiality for an ordinary user is practically no different from what applies today to card payments and mobile-banking transfers.

Nevertheless, this design has a flip side that the regulator itself does not hide. The unique digital code attached to each unit makes its movement history technically traceable in principle — meaning potentially accessible for analysis as part of investigations or other legal procedures. By comparison, cash remains the only fully anonymous means of payment, independent of any bank, government platform, or intermediary whatsoever. This is precisely why, among elderly people accustomed to cash transactions and among those who place a premium on financial privacy, the very idea of traceable digital money is often viewed with suspicion — as a potential erosion of economic freedom, even where formal guarantees of banking secrecy remain in place.

A separate and equally significant source of concern is the real-world status of the project's "voluntary" nature. Officially, use of the digital ruble by citizens is voluntary, and the law does not directly change that. But the Russian public has already accumulated experience watching initially optional digital services gradually become the de facto standard for receiving social benefits, paying for education, or interacting with government agencies — meaning formally voluntary mechanisms have over time turned into the only convenient, or even the only available, option. This is exactly why the public debate around the digital ruble extends well beyond purely technical questions of data protection and touches on the broader issue of balancing the convenience of digital money against an individual's right to financial privacy and anonymity in everyday transactions.

Against the backdrop of these concerns, the Bank of Russia also closed the public list of banks participating in the digital ruble pilot in July 2026 — Deputy Governor Zulfiya Kakhrumanova explained the decision as a response to heightened sanctions risks and a desire to protect specific credit institutions from targeted external pressure. According to her, 30 banks are currently connected to the platform, and testing continues on schedule — only the list of participants is no longer published.

Will It Be Possible to Pay With the Digital Ruble Offline?

As of today, fully autonomous offline payments with the digital ruble do not yet exist — this technology is still under active development rather than a finished solution ready for mass adoption. According to a statement by National Payment Card System (NSPK) CEO Dmitry Dubynin, made at a dedicated session of the Bank of Russia's Financial Congress on July 2, 2026, the company has been discussing full-offline options with the market for several years and regularly convenes banks within innovation discussion clubs to work through such a solution.

The nearest practical step is an offline mode specifically for QR payments: while a device is connected to the internet, it is preloaded with special cryptographic keys that allow a limited number of operations to be carried out without network access. However, to finalize the transaction, the device still needs to connect to the internet to complete the necessary authorization — meaning this is not a fully autonomous scenario but a temporary, operation-limited form of offline capability.

Further down the road, NSPK is considering creating a dedicated device or mobile app capable of exchanging data between transaction participants through alternative channels — such as NFC or Bluetooth — without touching mobile internet at all. According to Dubynin, moving toward such a fully autonomous solution is a matter of time rather than a fundamental choice: only that would deliver true convenience for payments made with the digital ruble and other modern payment services alike.

How Much Will the Digital Ruble Save Businesses and the State?

The fee for accepting digital-ruble payments through the universal QR code will run around 0.3% of the transaction amount — several times lower than traditional bank card acquiring, which currently costs merchants 1.5–2.5% per transaction. For retail businesses with high turnover and thin margins, this difference in fees directly affects bottom-line profit, particularly in segments built on mass, low-margin sales such as grocery retail or fast food.

Ilya Ivaninsky, director of the Center for Business Education and Analytics at Central University, estimated the total economic effect of digital ruble adoption at hundreds of billions of rubles in annual savings for the economy as a whole — driven by reduced acquiring costs, faster interbank settlements, and a shrinking share of cash circulation, which itself requires substantial banking infrastructure spending to service.

Beyond directly cutting fees, the Bank of Russia is also exploring more sophisticated use cases for the platform in business settings. One is smart contracts, capable of automatically executing deal terms and speeding up settlements between companies without constant intermediary involvement at every individual stage of a transaction. Another possibility under discussion is opening digital-ruble wallets not only on the Central Bank's own balance sheet but also on the balance sheets of commercial banks — one option for infrastructure development that, according to Nabiullina, requires detailed technical and operational work together with market participants.

Is It Worth Using Digital Assets on KuCoin While the Digital Ruble Is Rolled Out in Russia?

While a state-issued digital currency is only just moving toward mass use within a single country, millions of users worldwide have long relied on independent crypto assets to diversify their savings and take part in a global digital economy not tied to any one jurisdiction. KuCoin provides access to hundreds of crypto trading pairs, spot and futures trading tools, and staking — giving users more flexibility in managing digital assets than any single national platform bound by one country's regulatory framework.

To get started on KuCoin, it's enough to register, complete standard identity verification, and fund the account through one of the available methods. Built-in market-analysis tools and multi-layered fund protection help both beginners and experienced traders make more informed decisions when dealing with volatile assets. The ability to quickly move assets between spot and futures wallets makes the platform convenient for a range of strategies — from long-term portfolio building to active short-term trading on market swings.

This approach is especially relevant for anyone closely following the development of state-backed digital currencies like the digital ruble while also wanting tools on hand for working with independent crypto assets — two different, but not mutually exclusive, ways of using digital money.

Conclusion

The digital ruble is officially moving from the status of a long-running experiment to that of mandatory payment infrastructure: starting September 1, 2026, systemically important banks and large businesses with revenue over 120 million rubles are required to enable acceptance and transfers in the new form of national currency. For ordinary citizens, use remains entirely voluntary, and the currency unit itself represents a direct obligation of the Central Bank, which shields a user's funds from risks tied to the financial condition of any particular commercial organization.

At the same time, the unique technical traceability of each digital-ruble unit understandably raises questions about the balance between the convenience of the new payment form and the right to financial privacy — particularly among an audience historically accustomed to the anonymity of cash transactions. The project is also technically far from complete: fully autonomous offline payments, wallets held on commercial-bank balance sheets, and smart contracts for business are all still in development and practical testing, not a finished, mass-market product.

The economic case for the new tool already looks fairly compelling: a substantially lower fee compared with traditional acquiring, and potential savings of hundreds of billions of rubles per year, make the digital ruble attractive primarily to large-turnover retail businesses. How quickly and successfully the project expands to mid-sized and small businesses, and to the mass retail consumer, will depend on how convenient, predictable, and genuinely voluntary the tool proves to be in practice for all market participants.

Frequently Asked Questions

Are individuals required to switch to the digital ruble starting September 1, 2026?

No, use of the digital ruble by citizens remains entirely voluntary — the new obligations taking effect September 1, 2026 apply only to systemically important banks and large trading companies with revenue over 120 million rubles, not to individual consumers.

Will it be possible to pay with the digital ruble abroad?

Currently, the digital ruble operates exclusively within the Bank of Russia's platform inside Russia, and cross-border use cases are not part of the current rollout stage — that capability could only emerge at later stages of the project's development.

What happens to the money on my card if I don't open a digital wallet?

Nothing changes — ordinary cash and non-cash money will keep working exactly as before, since the digital ruble supplements existing forms of payment rather than replacing or eliminating them.

Does the Central Bank charge a fee for holding digital rubles in a wallet?

A fee applies only to payment transactions made through the universal QR code, at around 0.3% of the transaction amount, while simply holding funds on the Central Bank's platform carries no separate fee.

Why was the list of banks participating in the digital ruble pilot closed to the public?

The Bank of Russia closed the list of pilot participants due to heightened sanctions risks, aiming to reduce the likelihood of targeted external pressure on specific credit institutions, while the testing itself continues on the same planned schedule.