KuCoin Ventures Weekly Report: Evolution of Capital Entry Paradigms and Re-evaluation of High-Rate Expectations — The Crypto Institutionalization Wave and Sector "Stress Tests" Under AI and Macro Dynamics

2026/04/28 14:09:02

1. Weekly Market Highlights

Institutional Allocation Chain Continues to Take Shape: ETF Product Segmentation, Corporate Treasury BTC Accumulation, and Regulatory Negotiation Move Forward in Parallel

Over the past two trading weeks, the crypto market has not merely seen a price recovery. More importantly, the institutional allocation chain is continuing to take shape: ETF inflows have resumed, Wall Street products are evolving from low-fee spot exposure toward income-enhanced and staking-yield structures, and Strategy is continuing to accumulate BTC through capital market financing, turning corporate treasury adoption from a one-off purchase decision into a more systematic form of balance sheet management. On the data side, U.S. spot BTC ETFs recorded approximately $1.82 billion in net inflows over the two-week period, while spot ETH ETFs saw around $431 million in net inflows, indicating that mainstream institutional capital is still returning to the market through regulated products. At a deeper level, the way institutions access crypto is shifting from simple price exposure toward more complex income structures and balance sheet-driven allocation logic.

The product segmentation trend remains intact. Following Morgan Stanley’s launch of a low-fee spot BTC product, Goldman Sachs filed for a Bitcoin Premium Income ETF, which aims to generate option premium income through a covered call strategy while retaining BTC price exposure. According to Goldman’s filing, the fund does not directly hold BTC. Instead, it builds exposure through spot BTC-related products and their options, while enhancing income by selling call options. The significance of this design is not simply that it represents “another BTC ETF,” but that Wall Street is beginning to repackage BTC from a pure directional asset into an allocation tool that better fits the preferences of traditional income-oriented capital. Reuters also noted that this would be Goldman Sachs’ first Bitcoin ETF product, with a potential launch around late June after the standard review period, although the fee structure has not yet been disclosed.

Caption: Goldman Sachs’ Bitcoin Premium Income ETF seeks to generate option premium income through a covered call strategy. While retaining partial BTC price exposure, it enhances holding-period cash flow at the cost of sacrificing some upside potential. Strategy illustration adapted from Investopedia; product structure based on Goldman Sachs’ SEC filing.

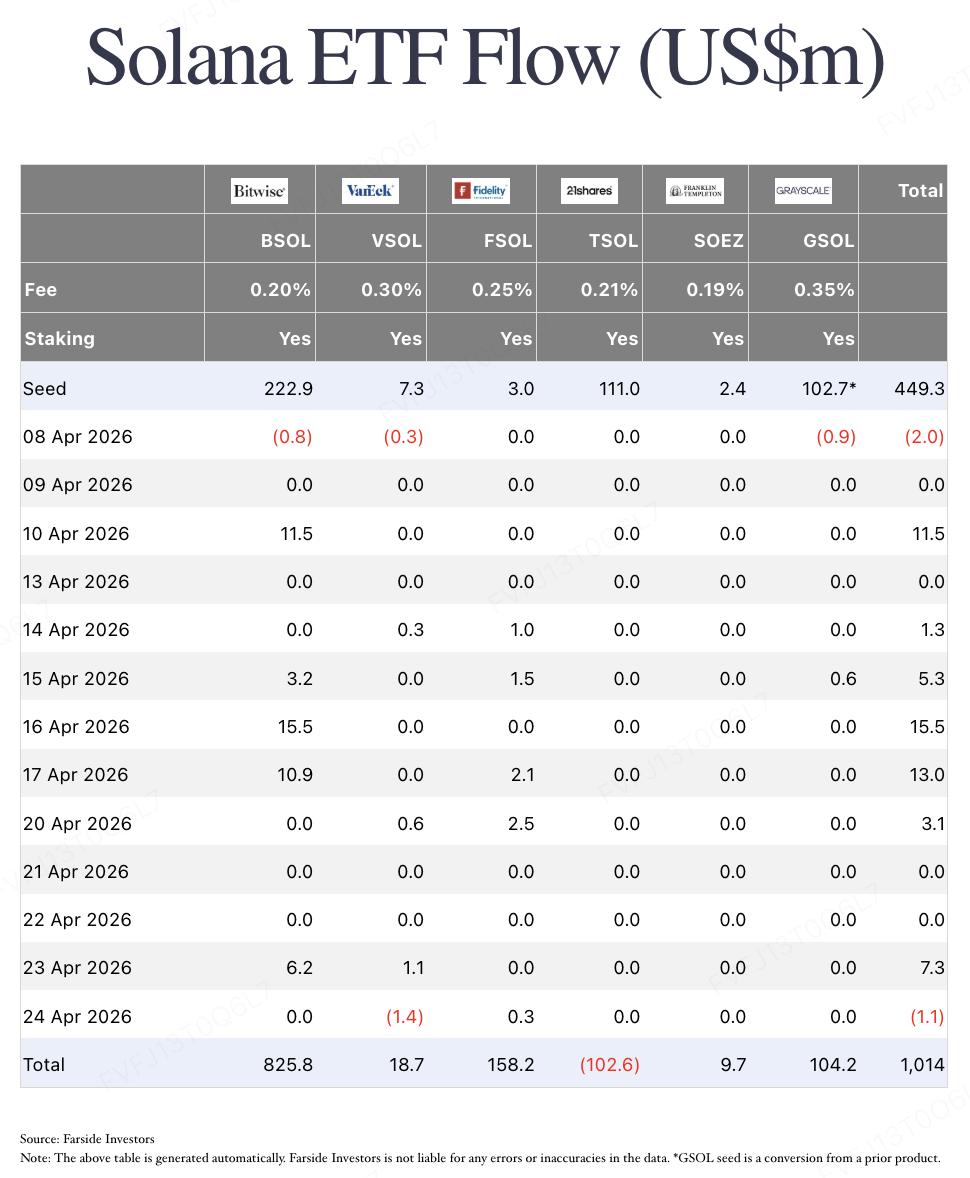

Altcoin ETFs continue to show signs of “marginal expansion.” The six U.S. spot SOL ETFs currently tracked by Farside are all marked as having staking functionality, suggesting that SOL products have moved beyond simple price exposure toward a “price exposure + on-chain staking yield” structure. 21Shares’ earlier update to the Hyperliquid ETF S-1/A filing also shows that the U.S. ETF toolkit is still attempting to cover assets with higher volatility elasticity and stronger native on-chain attributes. However, based on current fund flows, other crypto asset ETFs remain closer to “sentiment catalysts” than “mainstream capital magnets.” Over the past two trading weeks, SOL ETFs recorded around $44.4 million in net inflows, with cumulative net inflows of approximately $1.014 billion, still far below BTC ETFs in scale. At this stage, these products are mainly improving expectations, adding compliant access points, and expanding the range of assets institutions can reach. A stable institutional allocation loop will still require more time and stronger liquidity validation.

On the corporate side, the most notable development is Strategy’s continued integration of BTC purchases into balance sheet management. The company recently disclosed an additional purchase of 34,164 BTC for approximately $2.54 billion, bringing its total holdings to 815,061 BTC. Yet the more important point is not the purchase size itself, but the financing structure behind it. The funds mainly came from securities sold through at-the-market offering programs, including STRC variable-rate perpetual preferred stock and MSTR common stock. STRC can be understood as follows: the company issues perpetual preferred shares with floating dividend characteristics, investors receive relatively clear cash returns, and Strategy uses the proceeds to continue accumulating BTC. In effect, Strategy is institutionalizing the chain of “capital market financing — BTC purchases — balance sheet expansion,” turning corporate BTC accumulation from a one-time purchase into a financial engineering model that can continue operating.

This also makes Strategy’s signaling effect different from that of a typical corporate BTC buyer. It is not simply allocating idle cash to BTC. Instead, it is using multiple capital market tools, including common stock and preferred stock, to actively expand BTC as a core balance sheet reserve asset. ETFs represent institutional capital entering through regulated products, while Strategy represents corporate entities accumulating BTC through capital market instruments. The former improves BTC’s allocability, while the latter reinforces the narrative of BTC as a core corporate balance sheet asset. That said, this model also has constraints: preferred stock financing inherently requires ongoing dividend payments, and if BTC prices decline or MSTR’s premium narrows, the company’s financing efficiency and balance sheet flexibility could come under pressure.

Compared with the continued progress on the product and corporate fronts, the regulatory side remains in a state of “taking shape, but not yet landing.” Discussions around the CLARITY Act over the past two weeks have mainly been held up by issues including stablecoin yield, decentralized finance provisions, and vote coordination within the Senate Banking Committee. Galaxy’s update shows that the market had previously expected the committee to potentially schedule a markup by the end of April, but Senator Thom Tillis has leaned toward delaying it until May. Even if the bill clears committee review, it would still need to pass the full Senate, be coordinated with the Agriculture Committee’s version, be reconciled with the House-passed version, and ultimately move toward final approval. The legislative window is therefore not particularly wide. In other words, the core of the current U.S. regulatory debate is no longer simply whether crypto innovation should be supported, but how to redraw the boundaries among banking sector interests, financial stability, and on-chain financial innovation. This also means the current shift from “price recovery” toward “normalized allocation” still needs further validation: whether ETF net inflows can continue, whether income-enhanced and staking-yield products can withstand real liquidity and yield volatility tests, and whether the CLARITY Act can deliver clearer regulatory progress in May.

2. Weekly Selected Market Signals

Spillover of AI Dividends and Re-evaluation of Fed Rate Cuts: The Crypto Market Amid Steady Institutional Inflows and Sober Reflections on the Primary Market

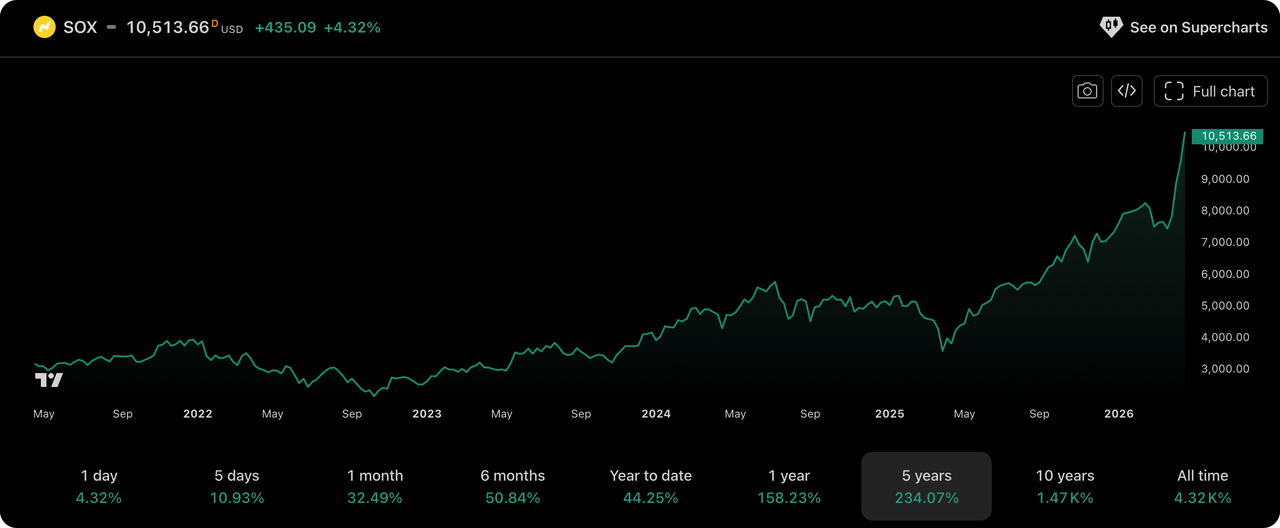

Recently, the global macroeconomic capital market has been dominated by two main forces: "AI-driven" narratives and "key macroeconomic data expectations." The U.S. stock market has performed exceptionally well, with financial reports from traditional financial giants further confirming the actual demand for AI infrastructure. Intel's latest earnings report once again validates the performance growth brought by AI commercialization, showing a trend of expanding from the core to the edge. This directly pushed the Philadelphia Semiconductor Index (SOX) to a record 18-day winning streak,historically breaking the 10,000-point mark.

Although Intel is relatively lagging in the data center GPU sector, it still maintains a dominant position in the enterprise and consumer PC markets. As the demand for AI computing power shifts from the cloud down to personal terminals, Intel has become the most direct beneficiary, bringing it massive revenue growth expectations. With the implementation of the "AI PC" concept, the Neural Processing Units (NPUs) integrated into its processors may become an important foundation for edge computing in terminal devices. Furthermore, while CPUs have limitations in AI training, their value on the inference side is increasingly prominent. Finally, under the current complex geopolitical landscape, Intel's maturing chip foundry business has also been endowed with a higher "security premium" and strategic value. Resonating with multiple factors such as narrative drivers, market expectations, and geopolitical demands, Intel is regaining a valuation reassessment in the capital market overall.

Data Source: TradingView

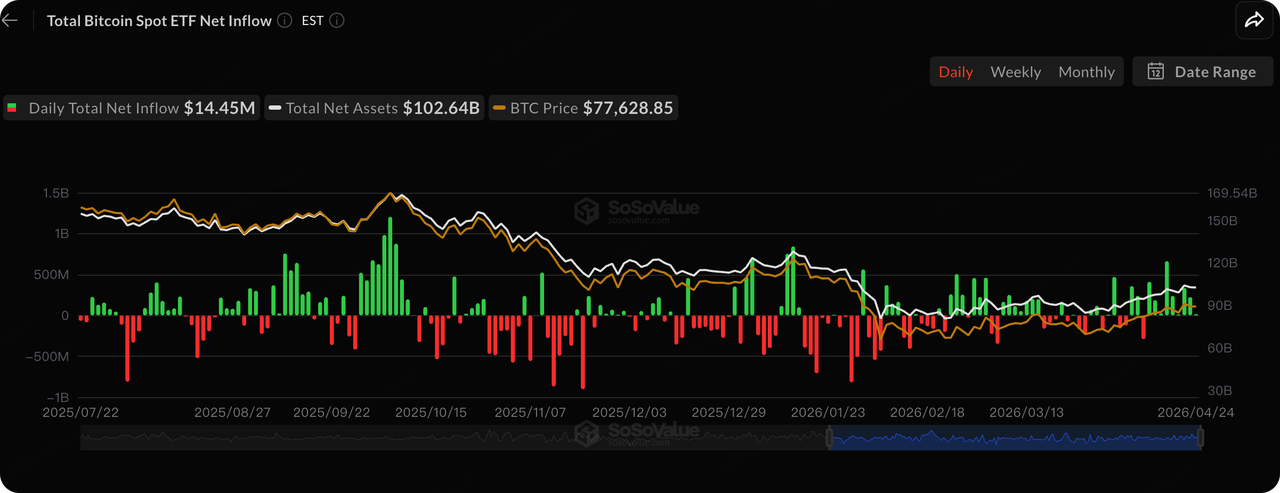

Meanwhile, global liquidity is entering a critical period of gaming. The market is highly focused on the upcoming Federal Reserve FOMC interest rate meeting this week (April 28 to 29). As traditional capital rebalances between tech stocks and safe-haven assets, stablecoins and compliant crypto assets are gradually becoming a new liquidity reservoir for institutional cross-asset allocation.

Data Source: SoSoValue

The most prominent feature of the crypto secondary market this week is the "continuous and steady injection of institutional funds":

-

Large Net Inflows into Spot ETFs: Crypto ETFs overall saw a net inflow of approximately $1.1 billion this week, showing particularly strong performance. Bitcoin ETFs took the dominant position, with Wall Street institutions like BlackRock continuing to buy. Notably, Ethereum ETFs also achieved 7 consecutive days of net inflows, releasing a positive signal that institutional asset allocation is expanding from solely BTC to ETH.

-

Institutional Purchasing Power Parallels High Premiums: The flagship enterprise MicroStrategy announced another purchase of 34,000 BTC this week, further consolidating its balance sheet strategy; in addition, Coinbase's spot premium has remained positive for 14 consecutive days, and Goldman Sachs has also filed for a Bitcoin ETF. The accelerated embrace by traditional capital has provided solid liquidity support for the overall market's valuation reconstruction.

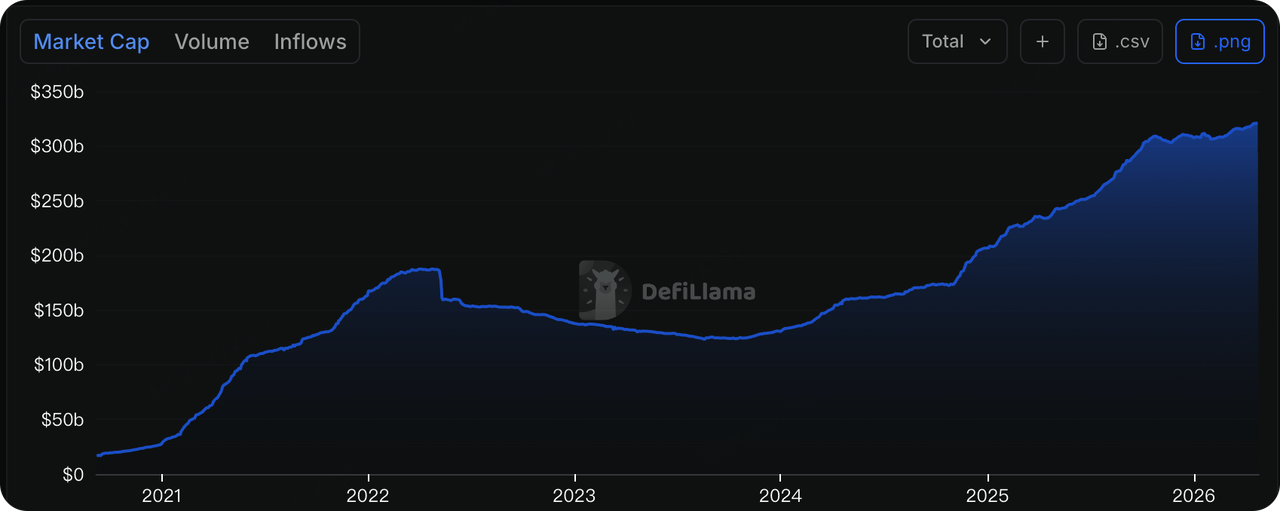

Data Source: DeFillama

Looking at the total market capitalization of stablecoins, the overall issuance since March has broken through the upper bound of the $310 billion range, entering a new upward channel. Currently, the overall issuance scale has reached approximately $320 billion. In particular, despite the strong wait-and-see and risk-aversion atmosphere in the overall crypto market, USDT's stablecoin issuance continues to maintain growth momentum. This reflects that the application scenarios of top stablecoins are further expanding, gradually penetrating into diversified ecosystems, thereby mitigating their endogenous reliance on single crypto asset cycles to some extent.

However, despite the fervent stablecoin narrative, the DeFi sector experienced severe stress tests this week. DeFiLlama data shows that on-chain hacking losses in April have exceeded $600 million. KelpDAO lost approximately $293 million, and Drift Protocol lost around $285 million; multiple DeFi protocols have suffered heavy blows one after another. Panic has led to a short-term TVL outflow of up to 23% (about $6 billion) in top protocols like Aave. Driven by risk aversion, funds are accelerating their transfer to perpetual DEXs equipped with real fee yields and token buyback models, seeking a safer haven.

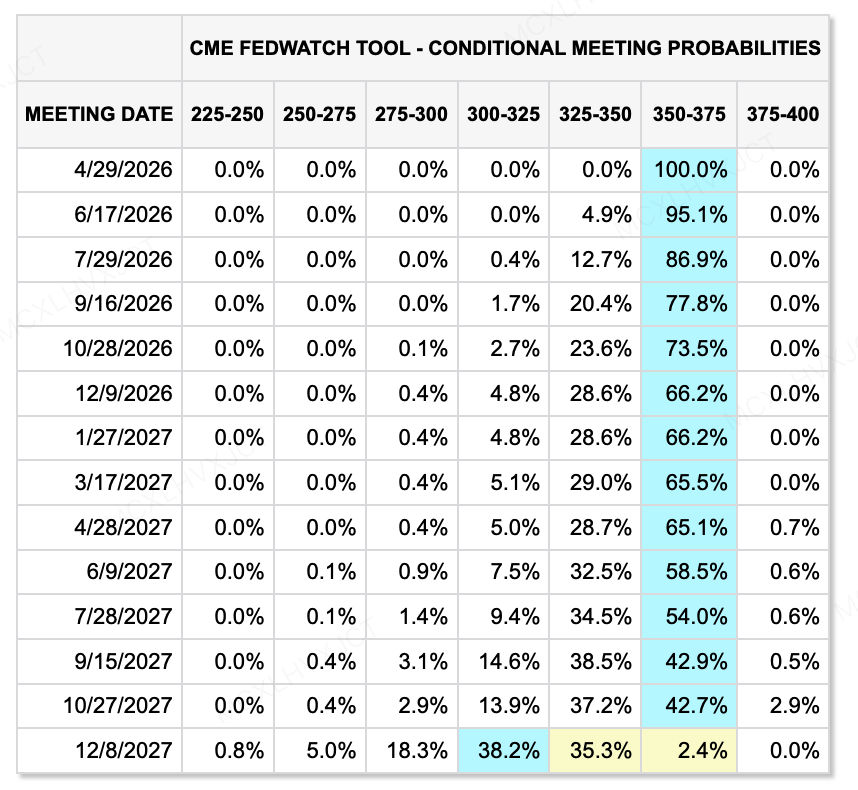

Data Source: CME FedWatch Tool

Combining the latest FedWatch data with recent statements from several Fed officials, global macro markets' expectations for "rate cuts" are undergoing a realistic re-evaluation, and "higher for longer" remains a broad consensus in the current market. For the upcoming FOMC interest rate meeting this week (April 29), the market predicts a 100% probability that rates will remain in the 350-375 basis points range. Even looking ahead to the end of 2026, the probability of maintaining rates in this range remains as high as 66.2%, which implies that the expected room for significant easing throughout 2026 is rather limited.

Furthermore, the term of the current Fed Chair, Jerome Powell, will end on May 15, 2026. If Kevin Warsh's nomination is successfully confirmed by the Senate, he is expected to officially take office after mid-May. The relatively hawkish policy stance of this new Chair candidate may add more variables to the future interest rate path. However, the situation is not entirely pessimistic. According to Kevin Warsh's views, the application of AI technology is expected to drive relatively rapid economic growth without triggering inflation, which might provide him a viable opportunity to reasonably push forward "rate cuts" in the future without relying entirely on the progress of quantitative tightening (QT).

Macro Events to Watch This Week:

Key focus points for the market in the new week:

This week is a veritable macro week. The focus of the capital market will be completely dominated by the Federal Reserve's interest rate meeting and heavyweight economic fundamental data.

-

April 28 - April 29: Federal Reserve FOMC Interest Rate Meeting and Rate Decision

-

April 30: Preliminary Annualized Rate of U.S. Q1 Real GDP

-

April 30: U.S. Initial Jobless Claims and other high-frequency employment data

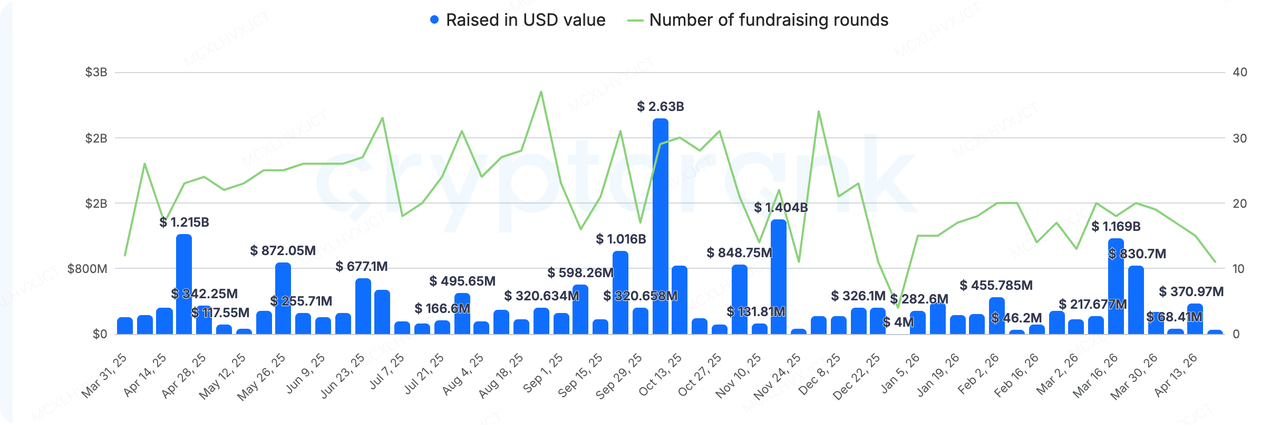

Data Source: CryptoRank

In the primary market, according to the broad statistical standards of CryptoRank, the total disclosed financing amount last week was approximately $51.98 million, encompassing 11 capital events, with both volume and value showing a certain decline. Overall capital and market attention continue to converge toward "hardcore infrastructure," while some application-oriented or uninnovative blockchain gaming projects are increasingly marginalized.

Cluster Protocol raised $5 million in this round, led by dao5, with participation from Paper Ventures and Mapleblock. The project focuses on utilizing FHE (Fully Homomorphic Encryption) technology to break through the pain points of data privacy. Meanwhile, the protocol has established an open-source community and a verification mechanism, attempting to incentivize global GPU computing power providers through a token reward system. However, the project also faces realistic tests ahead: from the perspective of actual engineering implementation and commercial cost, "FHE + AI Large Model Computing" still has a long way to go before achieving true large-scale commercialization.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.