KuCoin Ventures Weekly Report: Regulatory Tailwinds Meet Macro Headwinds: Unpacking the Double-Edged Sword of the SEC's New Crypto Rules and the Crypto M&A Wave Amid 'Higher-for-Longer' Rates

2026/03/25 10:33:02

1. Weekly Market Highlights

Decoding the New SEC/CFTC Crypto Guidance: A Historic Milestone in Crypto Compliance

The U.S. Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) have jointly issued interpretive guidance regarding the application of the Federal securities laws to certain types of crypto assets and certain transactions involving crypto assets under Release Nos. 33-11412. The document has been submitted to the Federal Register and is effective immediately upon publication.

Data Source: https://www.sec.gov/files/rules/interp/2026/33-11412.pdf

https://www.sec.gov/newsroom/press-releases/2026-30-sec-clarifies-application-federal-securities-laws-crypto-assets

This document, carrying committee-level authority, builds upon the "Project Crypto" initiative launched in 2025 ()and supersedes the Commission staff's Framework for "Investment Contract" Analysis of Digital Assets published in 2019. This joint action marks a deep harmonization of regulatory oversight between the two agencies, providing the market with a clearer compliance basis than previous staff-level statements.

Deconstruction of Core Rules:

-

Establishing Five Major Asset Classifications: For the first time, the document categorizes crypto assets into five classes based on their characteristics, uses, and functions: Digital Commodities, Digital Collectibles, Digital Tools, Stablecoins, and Digital Securities.

-

Officially Recognizing 18 "Digital Commodities": The document explicitly lists 18 tokens, including BTC, ETH, SOL, XRP, and AVAX, as digital commodities based on the Commission's understanding of their characteristics, terms, and functions as of the date of the release. These assets are not securities because their intrinsic value is derived from the programmatic operation of a functional crypto system and supply and demand dynamics, rather than from the expectation of profits from the essential managerial efforts of others.

-

Decoupling of Asset Characterization and Investment Contracts: The document clarifies the "separation" mechanism between a non-security crypto asset and the issuer's representations or promises (the investment contract. Even if a non-security crypto asset was initially offered and sold subject to an investment contract, the asset may separate from that contract under specific circumstances (e.g., once the issuer fulfills its promised essential managerial efforts, or publicly and unambiguously announces the abandonment of the project. If purchasers would no longer reasonably expect the issuer to continue engaging in such essential managerial efforts, the asset separates from the representations or promises. Once separated, secondary market transactions of the asset are no longer subject to federal securities laws. However, this mechanism is by no means a "get-out-of-jail-free card" for issuers. The document explicitly warns that even if an investment contract ceases to exist due to this decoupling, the issuer may still be subject to strict liability under the anti-fraud provisions of the federal securities laws for material misstatements, omissions, or failure to perform the promised efforts

-

Clearer Boundaries for On-Chain Activities: The document indicates that, under the circumstances described in the release, Protocol Mining, Protocol Staking, Wrapping, and certain Airdrops where recipients provide no consideration do not involve the offer and sale of securities. Therefore, participants do not need to register these transactions with the SEC. However, this determination remains dependent on specific structures and whether the elements of the Howey test are met in other contexts.

It is necessary to remain cautious, as Release Nos. 33-11412 is an "interpretive rule". While it is exempt from the Administrative Procedure Act's notice and comment requirements and can take effect immediately, it is not a statute enacted by Congress. This means it faces the risk of being challenged in court or overturned by a future administration. Furthermore, the document deliberately avoids certain complex gray areas; for example, it explicitly excludes the discussion of "restaking", nor does it deeply address the qualitative nature of DeFi governance tokens in DAO voting.

Overall, the joint SEC and CFTC document remains a landmark regulatory bridge, winning a precious window of development for a crypto market currently experiencing somewhat depressed sentiment. However, transforming this short-term certainty into a long-term, stable industry moat still requires waiting for true legislation at the congressional level (such as the CLARITY Act) to be enacted.

2. Industry Game: The "Perverse Incentive" in Information Disclosure

Although the clarification of rules brings overall benefits, its innovative "decoupling" mechanism has also opened a highly controversial Pandora's box. The document clearly points out that if the issuer experiences difficulties such as funding, technology, or market conditions, and publicly announces the "abandonment" of the project's development, no longer fulfilling its promised managerial efforts, the asset will no longer be subject to the investment contract (i.e., it sheds its securities attributes.

This could create a massive perverse incentive and moral hazard: in the past, if project teams took money but delivered nothing, they could face the iron fist of SEC securities fraud charges or class-action lawsuits; now, a widely publicized "project failure/abandonment statement" paradoxically becomes a "compliance shortcut" to wash the token's securities identity clean in the secondary market. Malicious or irresponsible project teams can use "technical bottlenecks" or "funding depletion" as excuses to legitimately halt development, leaving the secondary market with a token that has zero fundamental support but has achieved "compliance." Furthermore, to achieve "digital commoditization" of the token earlier, future project teams might deliberately adopt a "vague disclosure" strategy during the presale and whitepaper stages, avoiding the setup of clear milestones, fund usage, or profit expectations. This "compliance by lying flat" loophole will likely bring a wave of reform to the risk control and evaluation models of both primary and secondary markets.

3. Medium to Long Term: Hidden Dangers and Uncertainties Remain

We must remain cautious because the current document is administrative guidance. First, Release Nos. 33-11412 is an "interpretive rule," and while it bypasses the lengthy public comment period to take effect immediately(), it is not a statute enacted by Congress. This means it still faces the "administrative reversibility" risk of being challenged in court or overturned by the next administration in the future. Second, the document deliberately avoids some complex gray areas; for example, it explicitly excludes the discussion of "restaking"(), nor does it deeply address the qualitative nature of DeFi governance tokens in DAO voting.

Overall, the joint SEC and CFTC document remains a landmark regulatory bridge, winning a precious window of development for a crypto market currently experiencing somewhat depressed sentiment. However, transforming this short-term certainty into a long-term, stable industry moat still requires waiting for true legislation at the congressional level (such as the CLARITY Act) to be enacted.

2. Weekly Selected Market Signals

Middle East Risks Escalate Again, with Oil Prices and Rate Expectations Moving Higher in Tandem, Pressuring Risk Assets Lower

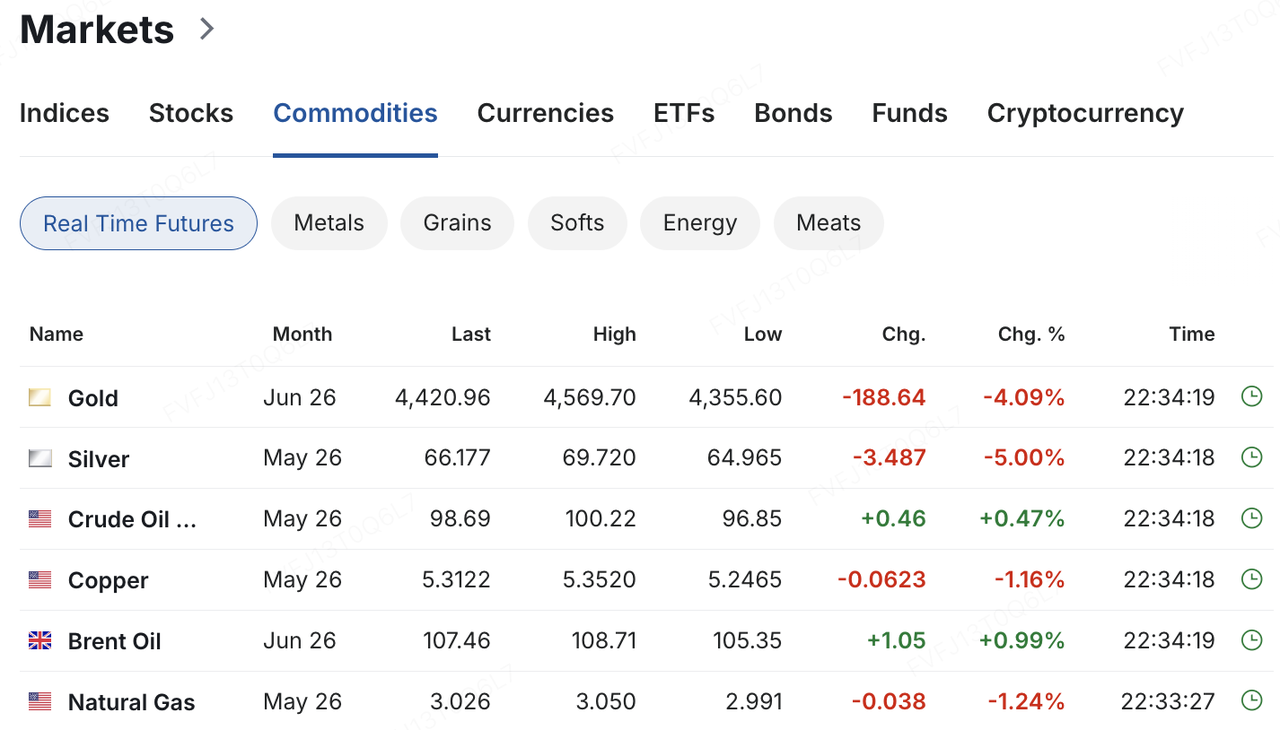

Over the weekend, the Middle East conflict once again shifted abruptly from a possible de-escalation narrative to a much more severe threat targeting critical infrastructure, prompting markets to start repricing the risk of a more prolonged energy supply shock. On March 22, Trump demanded that Iran fully restore navigation through the Strait of Hormuz within 48 hours, or face strikes on its power infrastructure. Iran subsequently responded that, if such action were taken, it would fully close the Strait of Hormuz and include energy and water infrastructure across the Gulf region in its retaliation. Against this backdrop, risk sentiment in Asian markets deteriorated sharply on Monday, with the Nikkei at one point posting a steep intraday decline and South Korean equities falling by nearly 6%. At the same time, Brent crude rose to around $112.9 per barrel, WTI approached $99 per barrel, the 10-year U.S. Treasury yield climbed to roughly 4.42%, and gold continued to weaken amid higher rate expectations and broader liquidity-driven selling.

Data Source: investing.com

At the core of current market pricing is no longer just a “geopolitical risk premium,” but an assessment of whether this energy shock is merely a short-term disruption or the start of a more persistent stagflationary drag. The Strait of Hormuz carries roughly one-fifth of global oil and LNG shipments. As long as markets continue to believe the conflict can be contained and shipping and supply can recover relatively quickly, the main impact on risk assets will likely be higher volatility rather than a full repricing. However, if the conflict lasts longer than expected and energy prices remain elevated, markets will need to simultaneously mark down global growth and corporate earnings while pushing back expectations for monetary easing by major central banks. Market discussion has already shifted from a one-off oil price disturbance toward the risk of a more persistent stagflation shock.

Against this macro backdrop, the previous countertrend recovery in crypto markets was also interrupted. Bitcoin had earlier risen to nearly a six-week high, approaching $76,000, but as oil prices surged, rate expectations turned more hawkish, and global risk assets came under synchronized pressure, BTC then reversed lower and fell back below the $70,000 level in the latter half of last week. As of the Asian session on March 23, BTC was fluctuating around the $68,000 range, while ETH had retreated to just above $2,000. Overall, the market has not repriced BTC as a geopolitical safe-haven asset. Instead, it continues to be treated more as a high-beta risk asset that remains highly sensitive to liquidity conditions and interest-rate expectations, with altcoins generally underperforming even more during this pullback.

Data Source: TradingView

On the flows side, institutional allocation appetite via ETFs has also begun to weaken at the margin. According to SoSoValue, U.S. spot BTC ETFs still recorded net inflows on a weekly basis last week, but turned to consecutive net outflows in the latter half of the week, suggesting that the prior rebound was not yet on a firm footing. By contrast, ETH ETFs shifted to net weekly outflows, ending their prior multi-week streak of inflows, indicating that under weaker risk sentiment and rising rate expectations, institutional allocation to ETH began to contract earlier.

Data Source: SoSoValue

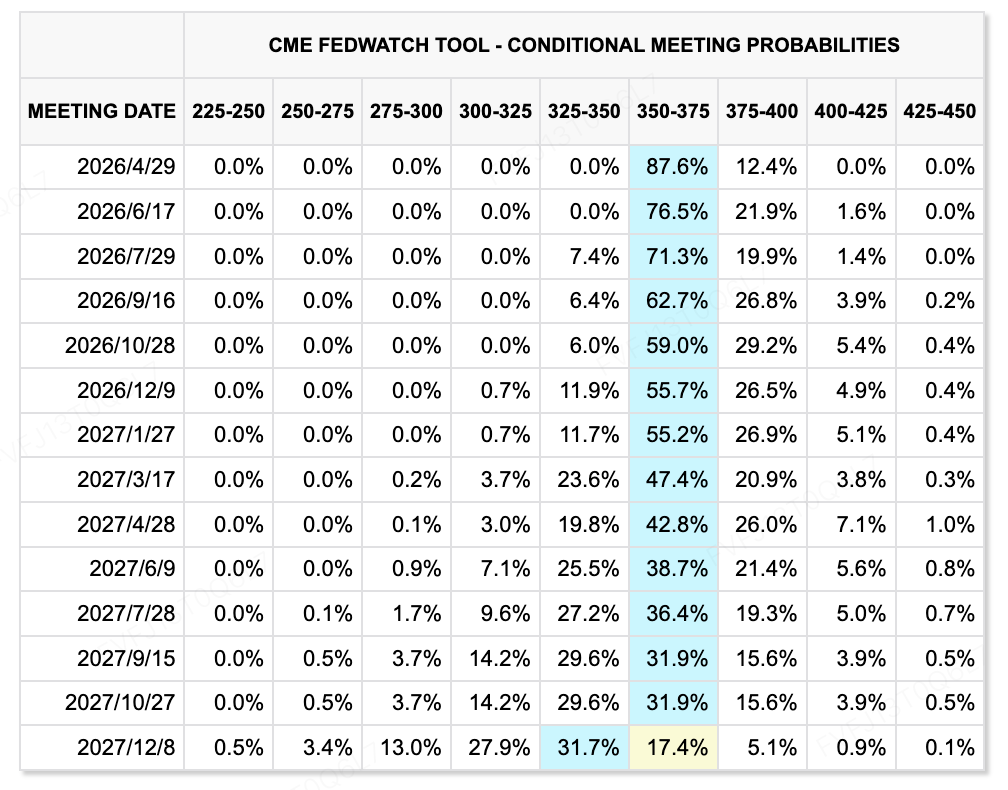

On the rates side, the key change this week is not whether the Fed will turn dovish immediately, but that the energy shock has meaningfully compressed room for easing expectations. At its March 17–18 meeting, the Federal Reserve left policy unchanged, keeping rates at 3.50%–3.75%, while raising its 2026 inflation forecast to 2.7%. Powell made it clear that higher energy prices would push up headline inflation in the short term, but that it was still too early to determine the lasting economic impact. At the dot-plot level, the Fed still retained a median expectation for one rate cut in 2026, but the rates market has turned materially more hawkish. Current pricing now broadly points to no rate cuts throughout 2026, and at certain points the CME FedWatch tool has implied that the first clearly priced-in cut may not arrive until late 2027. In other words, markets are not trading an “emergency easing” scenario; they are trading whether higher oil prices will force central banks to remain restrained, or even more hawkish, for longer. What will truly determine the next move in risk assets is no longer the meeting itself, but whether transit through the Strait of Hormuz can recover, how long oil prices stay elevated, and whether the Fed’s view that this energy shock is “temporary” can withstand reality.

Data Source: CME FedWatch Tool

Key Events to Watch This Week:

On the macro and geopolitical front, the energy shock remains the most important external variable this week. The escalation of threats over the Strait of Hormuz and regional energy infrastructure over the weekend has already pushed market focus back toward “second-round inflation” risks and a reassessment of central bank policy paths. Meanwhile, Denmark will hold parliamentary elections on March 24, Japan will release its February nationwide CPI on the same day, and the G7 foreign ministers’ meeting will take place in France on March 26–27. If oil prices remain elevated, market concern is likely to shift further from short-term risk premium repricing toward renewed worries about second-round inflation and a further rollback in expectations for global monetary easing.

On the earnings side, this week also marks a dense reporting window for China’s leading internet and consumer tech names. Xiaomi will report annual results on March 24, while Pinduoduo, Kuaishou, Pop Mart, and Meituan are also scheduled to release full-year earnings this week. Market focus will extend beyond revenue and profit figures themselves to management guidance on 2026 consumption recovery, advertising and e-commerce growth, hardware and new business investment, and the overall resilience of margins and profitability.

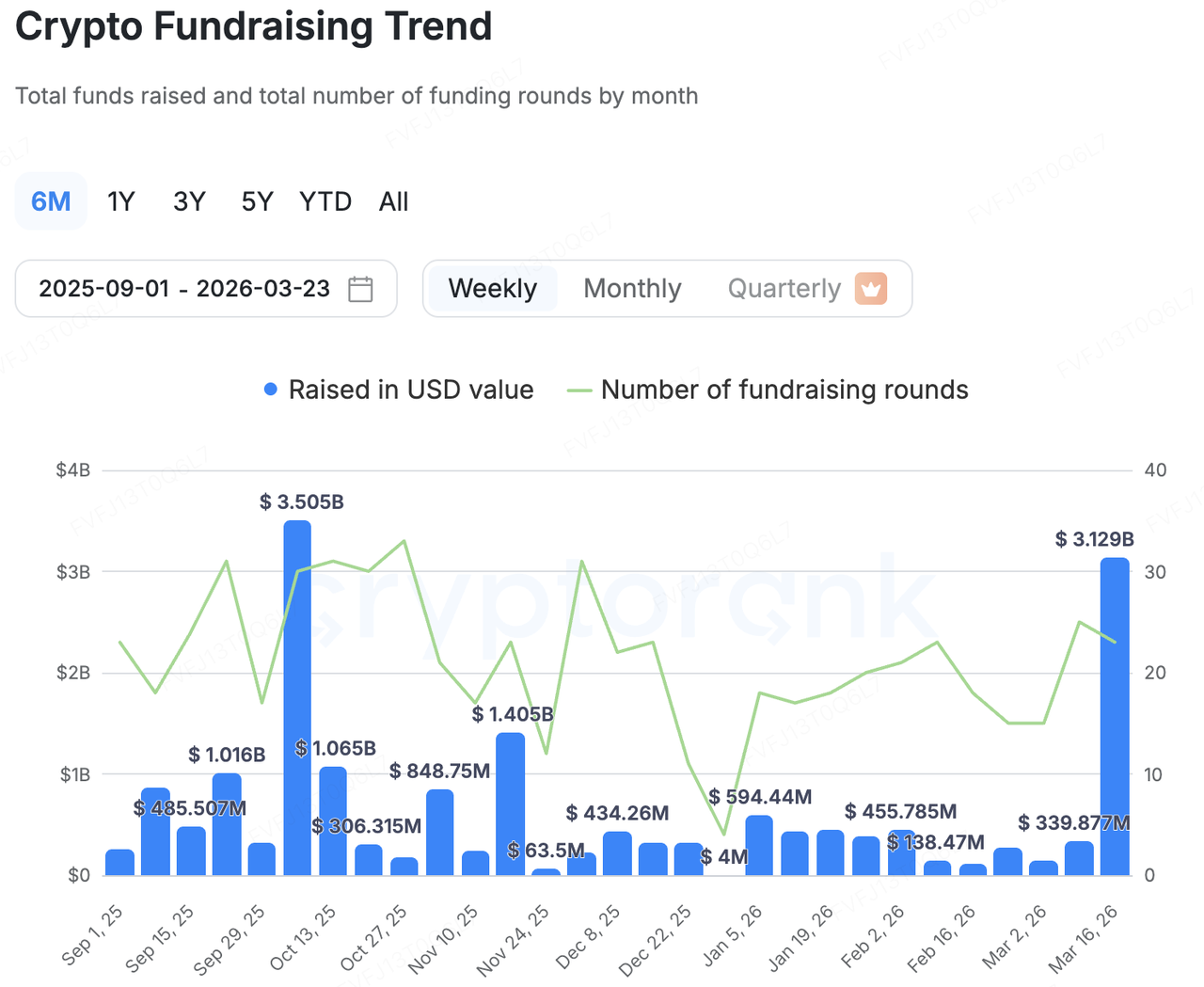

Primary Market Funding Observations:

Data Source: CryptoRank

In the primary market, under CryptoRank’s broad statistical framework, disclosed capital activity reached $3.129 billion this week across 23 transactions. However, capital distribution remained extremely concentrated, showing a clear pattern in which a handful of headline deals accounted for most of the weekly total. What truly drove the surge was not a broad-based recovery in early-stage venture financing, but rather a combination of M&A activity, large late-stage financings for mature platforms, and public-market refinancing tied to listed companies’ Bitcoin treasury strategies. Capital is increasingly flowing toward sectors and platforms that already demonstrate validated revenue, licensing infrastructure, distribution channels, or the ability to amplify valuation through capital markets.

BVNK acquired by Mastercard ($1.8 billion): The most representative transaction was Mastercard’s announcement that it will acquire stablecoin infrastructure company BVNK for up to $1.8 billion. The deal includes up to $300 million in earn-out payments and is expected to close by the end of 2026, subject to regulatory approval. Founded in 2021, BVNK currently supports fiat-to-stablecoin payment and settlement services across more than 130 countries and major blockchain networks, and holds licenses across multiple jurisdictions. Combined with its Series B round led by Haun Ventures in late 2024 and subsequent strategic investments, BVNK has clearly evolved from a crypto payment infrastructure startup into a key gateway asset for TradFi’s push into on-chain payments. For Mastercard, the significance of this acquisition goes beyond simply filling out its crypto business map; it provides a fast route to 24/7 settlement, programmable payments, and cross-border stablecoin rails, effectively integrating on-chain payments into its existing global payments network.

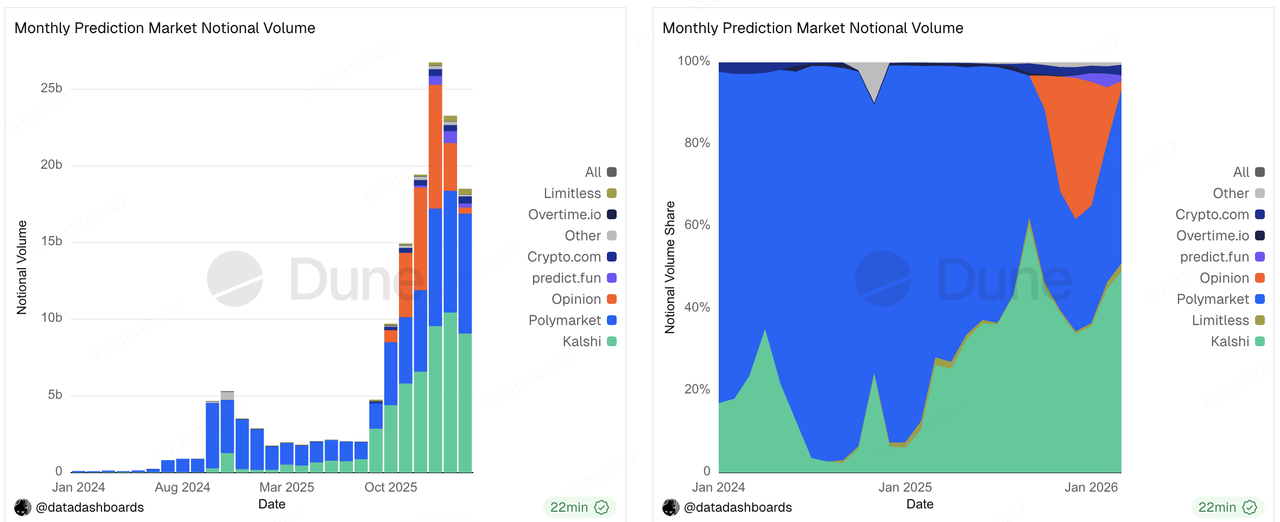

Kalshi completes Series E ($1 billion): Prediction market leader Kalshi raised more than $1 billion in a new round led by Coatue Management, bringing its valuation to $22 billion. From a business perspective, Kalshi is no longer simply a “crypto narrative” project, but an event-contract platform that has rapidly scaled across trading activity, institutional participation, and monetization. Media reports indicate that the company’s current revenue run rate has reached approximately $1.5 billion. At the same time, Kalshi’s valuation expansion is not without cost: it continues to face ongoing legal and regulatory pressure at the state level. It has recently been hit with a temporary restraining order in Nevada, while Arizona has also brought criminal charges, intensifying the conflict between federal regulatory preemption and state gambling enforcement powers. This financing round shows that the primary market remains willing to pay premium valuations for prediction market leaders with strong growth and heavy trading demand, but whether those valuations can continue to move higher will ultimately depend on whether the regulatory framework becomes clearer.

Data Source: https://dune.com/datadashboards/prediction-markets

Metaplanet completes post-IPO financing ($255 million): Tokyo-listed Metaplanet completed a third-party allotment worth roughly JPY 40.8 billion, together with its 26th series of stock acquisition rights. If fully exercised, the total potential financing size could rise further to roughly JPY 85.3 billion. The company has made it clear in its filings that it will continue advancing capital operations centered on its Bitcoin treasury strategy, targeting 100,000 BTC by the end of 2026 and 210,000 BTC by the end of 2027. This case reflects how both private and public-market capital are still actively pursuing the “BTC treasury” narrative, especially among listed platforms that have equity-financing access and can translate Bitcoin price sensitivity into equity valuation premium. These financings are not fundamentally a bet on traditional operating cash flow, but rather a bet that capital markets will continue rewarding listed vehicles that offer amplified BTC exposure.

Autonomous and Architech acquired by GSR ($57 million): Beyond large financings, M&A consolidation was also an important signal in the primary market this week. GSR acquired Autonomous and Architech for $57 million, aiming to integrate token issuance, organizational operations, financial infrastructure, token design, liquidity strategy, and treasury management into a unified capital markets service platform for crypto projects across their full lifecycle. This points to another clear market trend: rather than continuing to fund more point solutions, the market is increasingly packaging advisory, capital markets, treasury, and launch capabilities together, moving toward a more “crypto-native investment bank” model.

Brahma acquired by Polymarket (undisclosed): A similar consolidation logic was visible in Polymarket’s acquisition of Brahma. Since its founding in 2021, Brahma has processed over $1 billion in volume, with core strengths in smart accounts, execution, and DeFi infrastructure. Polymarket’s acquisition is not merely about adding a technical team; it is aimed at further abstracting away underlying blockchain complexity, reducing user friction across wallet creation, deposits and withdrawals, conversion, and payout processes, and pushing prediction markets further from a crypto-native product toward a platform accessible to mainstream consumers. From a capital markets perspective, this suggests that investors are placing increasing value on infrastructure teams that can package on-chain capabilities into smoother, more user-friendly product experiences.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not legal, compliance, financial, or investment advice, an offer, solicitation, or guarantee. We make no express or implied representations or warranties regarding its accuracy, completeness, or reliability, and disclaim liability for any resulting losses. Investments/trading are risky; past performance doesn't guarantee future results. Users should research, judge prudently, and take full responsibility. Please consult professional legal, tax, or financial advisors if necessary.