KuCoin Ventures Weekly Report:Macro Storms and Compliance Breakthroughs: Kraken's Direct Fed Connection Ignites the Battle for Underlying Infrastructure, Geopolitical Conflicts Reshape Asset Pricing

2026/03/10 14:24:02

1. Weekly Market Highlights

Kraken's Direct Fed Connection and the CLARITY Act Maneuvering: Crypto Compliance Enters the "Underlying Infrastructure" Battle

Last week, on March 4th, the US crypto compliance process reached a highly indicative milestone. Kraken Financial, a Wyoming Special Purpose Depository Institution (SPDI) under Kraken, was officially approved for a master account by the Federal Reserve Bank of Kansas City. After five years of application and regulatory back-and-forth, Kraken has become the first crypto-native institution in US history to directly access core payment systems like Fedwire and FedACH.

In the past, crypto enterprises could only rely on third-party traditional banks (such as the previously collapsed Silvergate and Signature, as well as current institutional favorites like Cross River Bank and Lead Bank) to process clients' USD fiat deposits and withdrawals. Now, Kraken can bypass these intermediary banks and send and receive funds directly within the Federal Reserve's network. Skipping the intermediaries will significantly reduce the time and operational costs of fiat transactions. It also allows institutional clients to truly take a seat at the main table, paving the way for the subsequent on-chain atomic settlement of stablecoins and tokenized Real World Assets (RWAs).

However, this authorization does not mean the door has been completely thrown open. The Federal Reserve granted Kraken a "limited-purpose (skinny)" account, with an initial term of only one year. This account does not allow Kraken to enjoy the full privileges of traditional banks; for example, its balances at the Fed cannot generate interest yields, nor can it utilize the Fed's discount window and emergency lending facilities.

This direct-connection model inevitably threatens the vested interests of traditional banking lobbying groups. They have mounted fierce opposition and rebuttals, citing "opaque procedures" and the risk that "high crypto volatility could infect the national payment system." Meanwhile, the CLARITY Act (H.R.3633), aimed at establishing a clear regulatory framework for the crypto market, is still struggling to advance. Although the bill passed the House with bipartisan support in July 2025—clarifying the jurisdictional divide between the SEC and the CFTC—it currently remains stalled in the Senate Banking Committee due to core conflicts of interest, such as stablecoin yield distribution, and faces strong resistance from traditional banking lobbyists.

Therefore, for Kraken, this is both an opportunity and a major test. If any missteps occur during this upcoming one-year "pilot" period, it is highly likely that traditional banking lobby groups will seize upon them as leverage, triggering regulatory tightening or even driving new legislation to block future applications from crypto banks.

For US crypto institutions, compliance strategy has entered the next phase—shifting from simply "striving for policy friendliness" to a tangible "battle for underlying infrastructure." It is also crucial to remain wary of the market's overly optimistic sentiment regarding the rapid enactment of federal-level legislation like the CLARITY Act. During the current window of political maneuvering, the possibility of extreme shifts must be carefully considered.

2. Weekly Selected Market Signals

Geopolitical conflict is reshaping global asset pricing, while the oil surge revives stagflation concerns

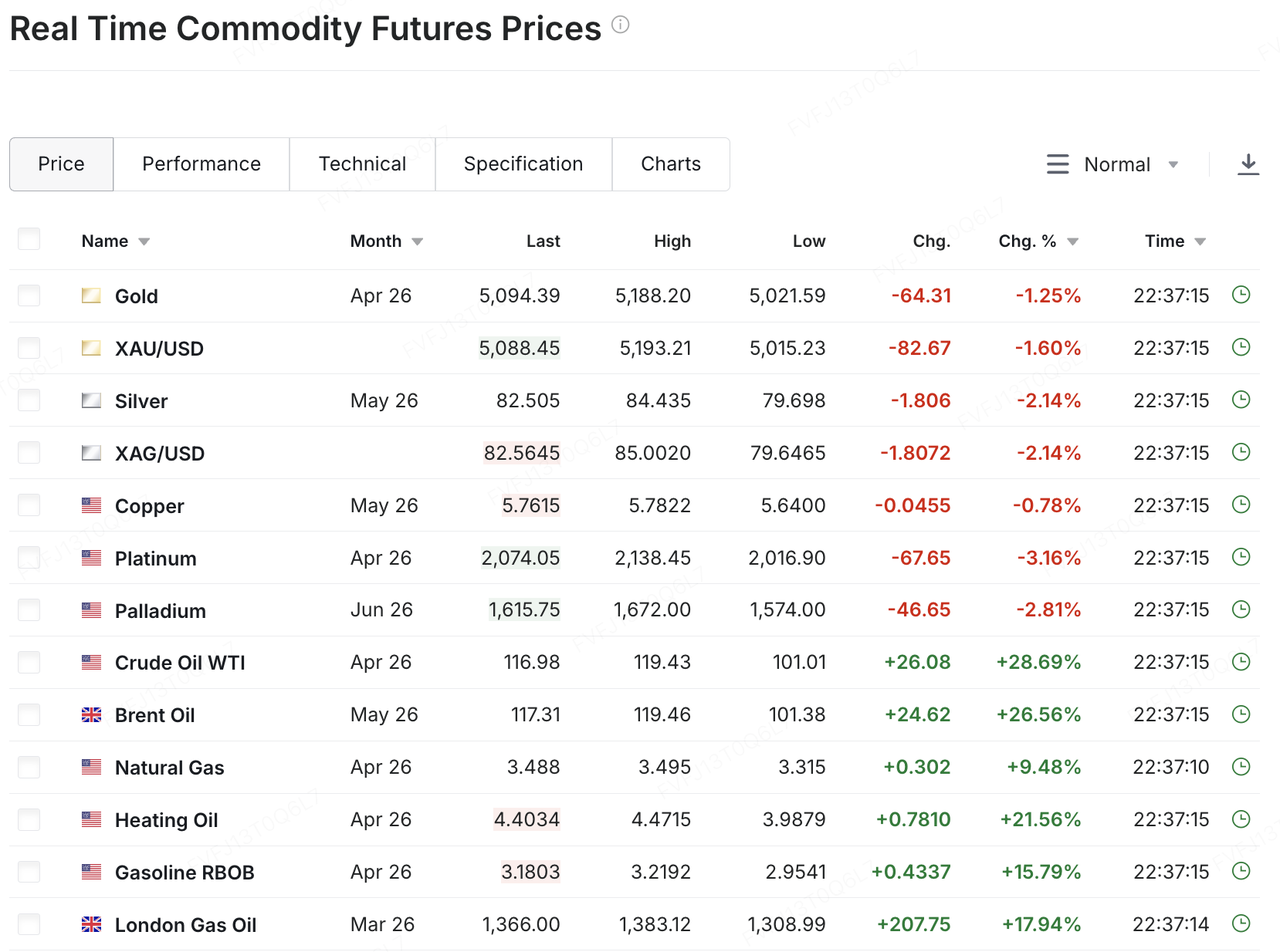

The latest escalation in the Middle East is rapidly changing the market’s core pricing logic. On March 9, international crude prices surged sharply, with both WTI and Brent futures breaking above $110 per barrel, driven by disruptions to shipping through the Strait of Hormuz, regional supply interruptions, and production cuts by several major oil producers. Although U.S. officials attempted to calm markets through policy messaging, recent price action suggests investors are no longer trading a simple “geopolitical risk premium,” but rather a more disruptive “energy supply shock.”

Data Source: investing.com

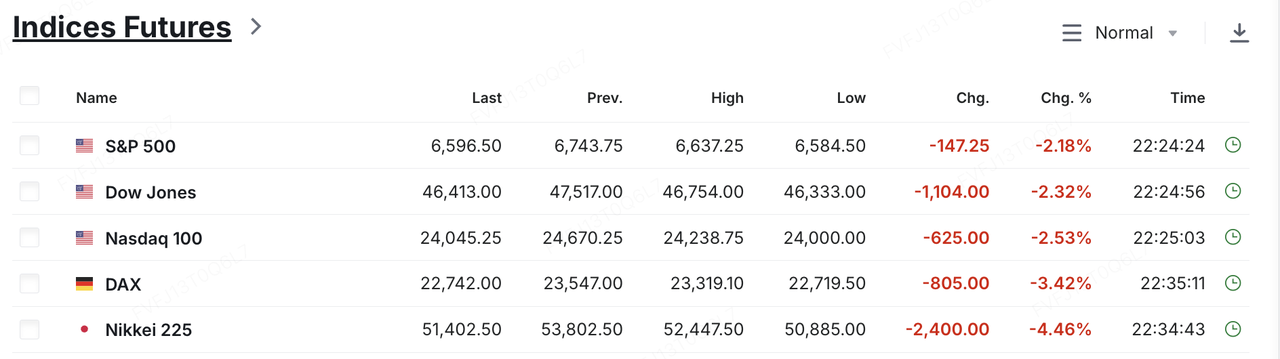

The sharp rise in energy prices has directly intensified concerns over a renewed inflation impulse and further downward revisions to growth expectations. U.S. equity futures came under broad pressure, with Dow futures falling more than 1,000 points intraday and both S&P 500 and Nasdaq futures down over 2%. Asian markets also opened sharply lower, with the Nikkei 225 falling more than 7% at one point and South Korea’s KOSPI down around 7.6%. From a market structure perspective, risk assets are increasingly being repriced within a more classic stagflation framework: on one side, higher oil and transport costs are reinforcing inflation stickiness; on the other, growth and earnings expectations are facing a second round of downward revisions.

Within traditional safe-haven assets, market behavior has also become more nuanced. The U.S. dollar continues to strengthen, sovereign bonds remain under pressure, and yields are moving higher. Gold has not fully benefited from geopolitical risk aversion and has instead softened under the combined weight of a stronger dollar and rising inflation expectations driven by oil. This suggests the market is becoming more concerned about a shrinking policy easing window than about seeking static safe havens. In other words, the market is shifting from a pure “risk-off” trade toward a repricing of how higher oil prices may alter the policy path and asset discount rates.

Against a backdrop of intensifying stagflation concerns, crypto has yet to shake off its macro risk-asset characteristics. BTC briefly fell to $65,688 intraday before recovering to around $67,175, nearly erasing most of last week’s rebound. Meanwhile, roughly $329 million in leveraged positions were liquidated across the market over the past 24 hours, highlighting how fragile short-term positioning remains and how sensitive the market still is to external macro shocks.

Data Source: TradingView

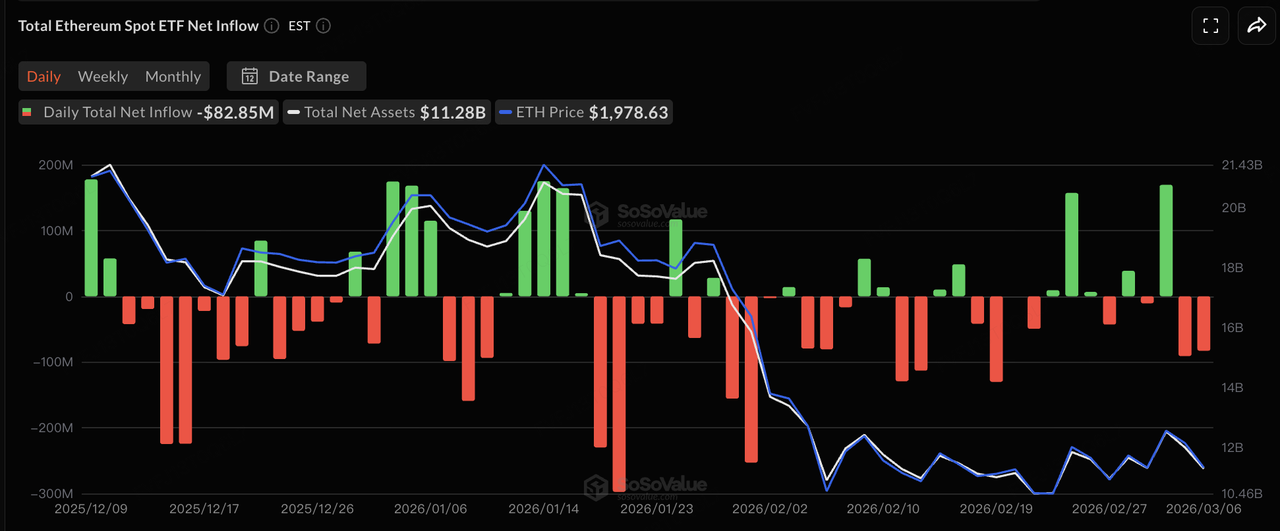

That said, institutional allocation has not turned fully pessimistic. U.S. spot BTC ETFs recorded strong net inflows over the first three trading days of last week. Although flows turned negative again in the second half of the week as the conflict escalated, spot BTC ETFs still posted approximately $568 million in net inflows for the week ending March 6, marking a second consecutive week of positive flows. Spot ETH ETFs also rebounded notably alongside the price recovery, recording around $169 million in daily net inflows on March 4, the highest level in nearly two months. Although momentum slowed over the following two sessions, weekly net inflows still came in at roughly $23.56 million. Overall, ETF flows have not yet broken the recovery trend, but neither have they entered an unconditional risk-on phase. Whether this improvement can continue will depend on actual follow-through flows after the U.S. equity market opens and on whether geopolitical tensions continue to deteriorate.

Data Source: SoSoValue

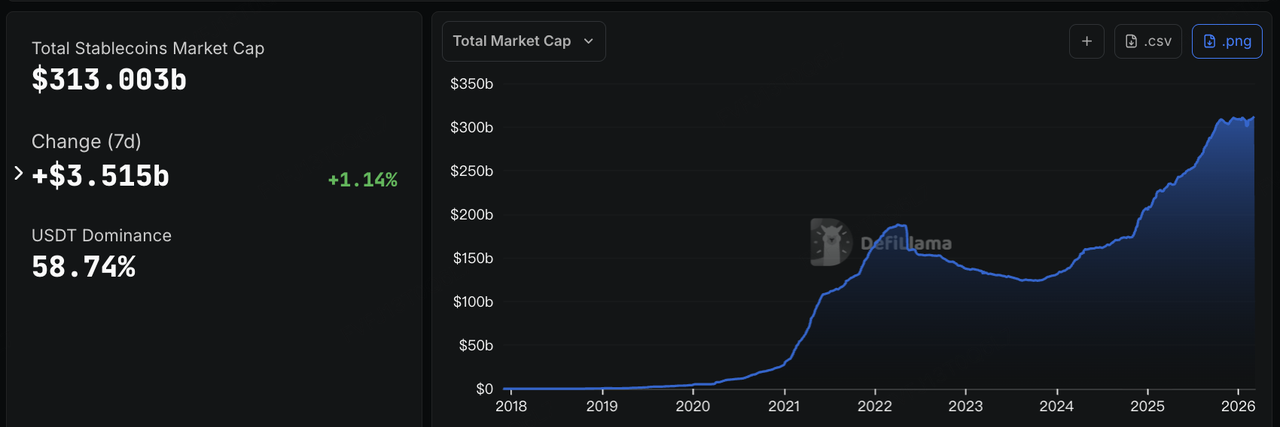

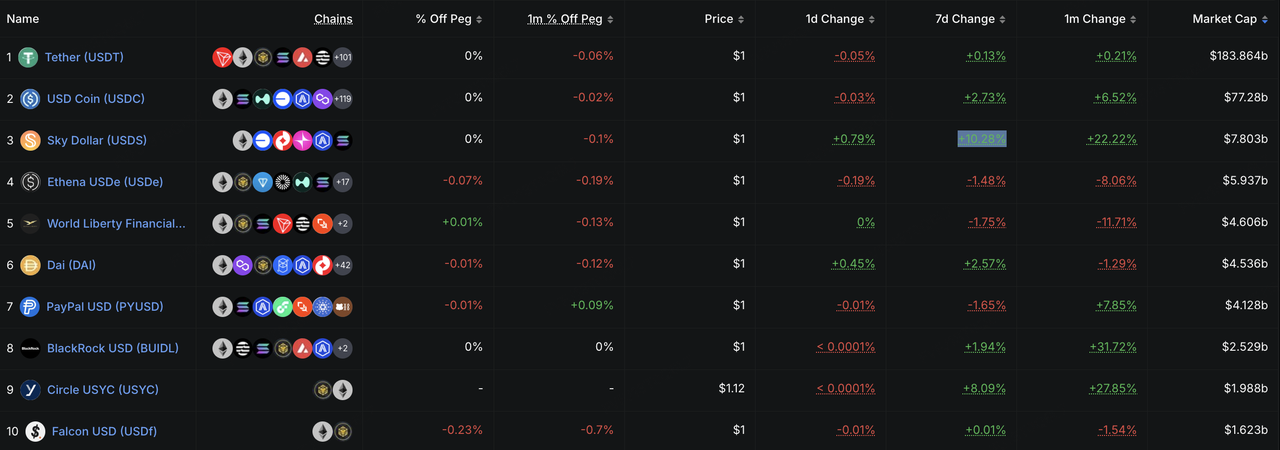

The stablecoin sector, meanwhile, continues to reflect a pattern of weakening risk appetite and capital rotating back into cash-like positions. According to DefiLlama, total stablecoin market capitalization has risen to around $313 billion, up roughly $3.51 billion over the past seven days. Among individual names, Sky ecosystem stablecoin USDS was one of the strongest-performing major stablecoins over the past week, with market capitalization rising to about $7.8 billion, up more than 10% week over week. Its expansion appears to be linked to governance changes implemented by Sky on March 2, including reduced token emissions, an expanded USDS credit infrastructure, the introduction of new Launch Agents, and optimized sUSDS yield. In the current market environment, capital appears to favor stablecoin assets that offer yield absorption capacity, stronger liquidity, and higher composability.

Data Source: DeFillama

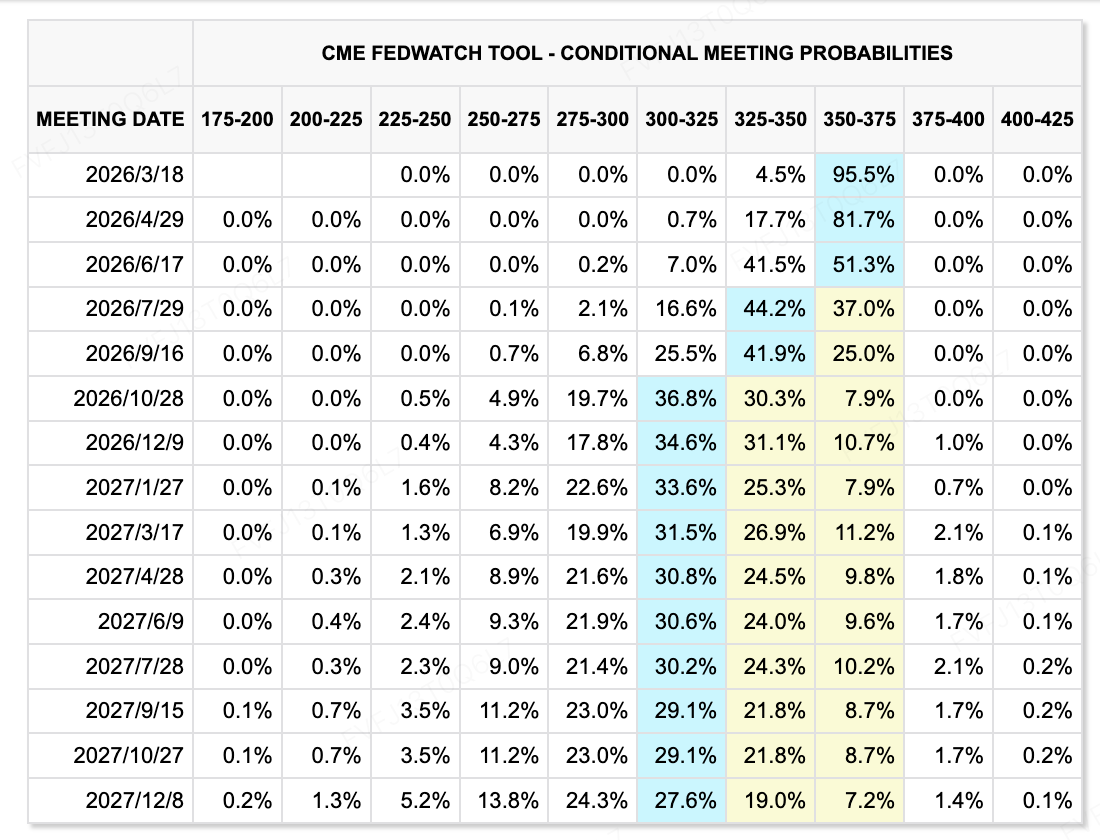

From a macro policy perspective, the Middle East conflict and rising oil prices are further compressing the Fed’s room for marginal easing. CME FedWatch still shows that the market’s base case remains no rate change at the March meeting. However, following the unexpected softness in February nonfarm payrolls and the rapid move higher in oil, expectations for the timing of subsequent rate cuts risk being pushed back again. For risk assets, the most unfavorable scenario is not simply higher inflation or weaker growth in isolation, but the policy constraints created when both emerge at the same time. That remains one of the key reasons recent market volatility has intensified.

Data Source: CME FedWatch Tool

Key Events to Watch This Week:

The Middle East is approaching a critical juncture. Iran may soon unveil new leadership, with an election-related meeting expected within the next 24 hours, while joint U.S.-European military exercises add to geopolitical uncertainty.

-

March 9–10: China is set to release a dense slate of February data, including CPI, PPI, trade, credit, and aggregate financing, offering an early test of the economy’s momentum at the start of the year.

-

March 11 and 13: The U.S. February CPI and the delayed January core PCE will be released in sequence, prompting markets to reassess whether the oil shock could materially alter the Fed’s policy path for the rest of the year.

Primary Market Funding Observations:

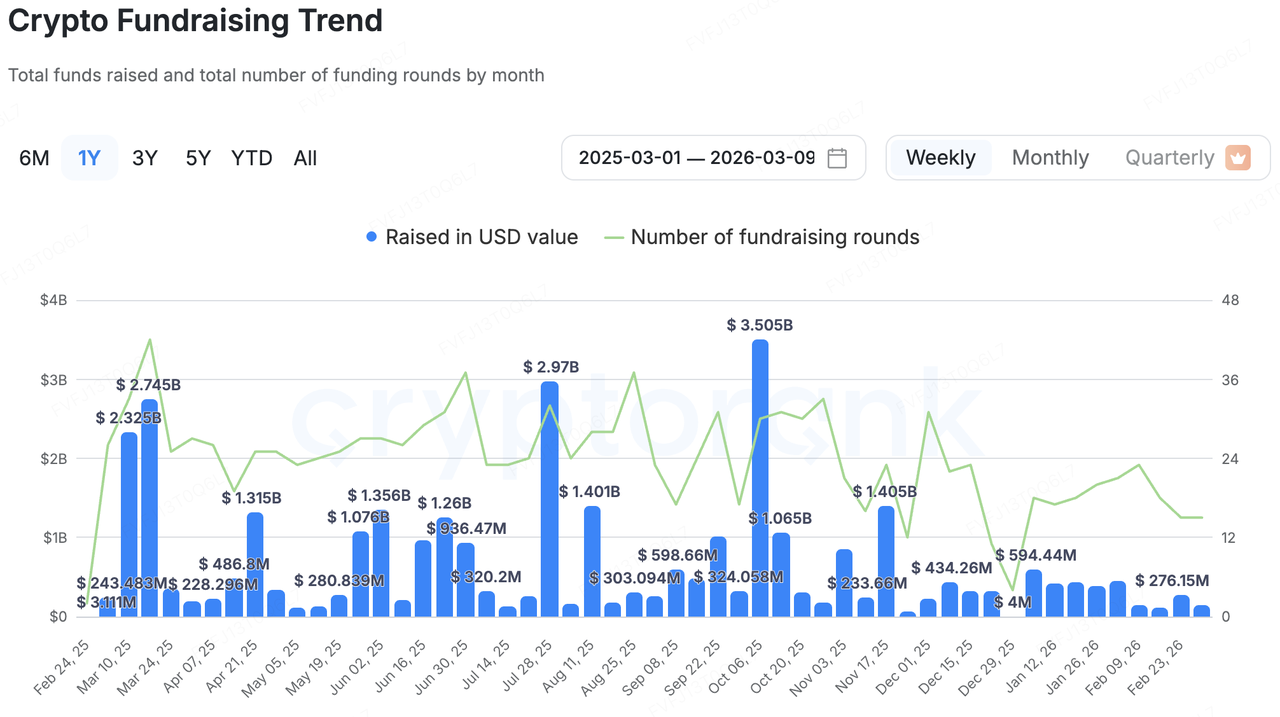

Data Source: CryptoRank

In the primary market, CryptoRank data shows $137 million in disclosed funding across 10 deals this week. Recently announced financings and M&A activity continue to cluster around payments, trading, and market infrastructure, reinforcing the trend of capital concentrating in sectors more directly tied to cash flow generation and real financial use cases.

One of the most closely watched developments was ICE’s strategic investment in OKX. Based on public disclosures, ICE has taken a stake in OKX and plans to deepen cooperation around digital asset market infrastructure, tokenized securities, and the digitization of traditional financial assets. The signal here goes beyond a simple “TradFi entering crypto” narrative; it also reflects a reassessment by leading infrastructure institutions of the long-term opportunity in on-chain trading and the digitization of securities.

Other funding includes:

-

QFEX: Raised $9.5 million in seed funding led by General Catalyst, with participation from Y Combinator and others. The project is positioned as a 24/7 high-leverage derivatives venue for traditional assets, including U.S. equities, commodities, and FX.

-

Axiym: Received a strategic investment from stablecoin issuer Tether, with the amount undisclosed. The focus is on embedding USDT into compliant treasury management and settlement infrastructure, particularly for cross-border payments and “Pay Now, Settle Later” use cases.

-

Predict.fun: Completed the strategic acquisition of Probable, an on-chain prediction platform originally incubated by PancakeSwap and YZi Labs, signaling further liquidity and resource consolidation within the BNB Chain prediction market segment.

The VC landscape remains increasingly bifurcated

a16z crypto is reportedly raising its fifth crypto fund with a target size of around $2 billion, aiming to complete fundraising in the first half of 2026. That is materially smaller than its $4.5 billion fourth crypto fund raised in 2022. In explaining the smaller size, a16z said it wants shorter fundraising cycles in order to stay more flexible and better aligned with fast-changing crypto narratives.

At the same time, Multicoin co-founder Kyle Samani has reportedly stepped back into an advisory role and shifted more of his focus toward AI, longevity, and robotics. Paradigm, meanwhile, is said to be preparing a new fund of up to $1.5 billion while also expanding its investment scope into AI and robotics.

In other words, leading institutions have not abandoned crypto, but capital is becoming more concentrated in stablecoins, RWA, payments, and other areas with clearer cash-flow visibility. Tolerance for highly narrative-driven Web3 projects with long monetization cycles appears to be declining.

This shift is also tied to the broader market drawdown. According to CoinGecko data, even after a partial rebound, total crypto market capitalization remains roughly $2 trillion below its peak of around $4.3 trillion last October, currently sitting near the $2.3 trillion range.

For investors, AI-related assets with faster revenue visibility, clearer compliance pathways, and more verifiable demand are becoming increasingly attractive alternatives, drawing capital away from crypto startups. For crypto founders, this means that narrative alone is becoming less sufficient to win investor attention; business models, cash-flow pathways, and defensive resilience are becoming increasingly important.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not financial or investment advice, an offer, solicitation, or guarantee. We disclaim liability for its accuracy, completeness, reliability, and any resulting losses. Investments/trading are risky; past performance doesn’t guarantee future results. Users should research, judge prudently, and take full responsibility.