KuCoin Ventures Weekly Report: The AI Productivity Explosion and Pragmatic Insights from Humanoid Robots; Surging Risk-Off Sentiment Amid Trump's Tariff Policies and the Evolving Landscape of Prediction Markets

2026/02/24 14:15:02

1. Weekly Market Highlights

The Surge of AI Productivity vs. the Narrative Exhaustion of Crypto: Abandoning the Obsession with Grand Narratives and Returning to Pragmatic Business Fundamentals

This week, the crypto market was relatively flat internally, lacking truly breakthrough events or structural innovations compared to the surging external markets. When we turn our attention to the neighboring AI and hard tech sectors, the ongoing technological explosion and commercialization undoubtedly sound an alarm for some crypto entrepreneurs who remain immersed in outdated narratives. Under the scrutiny of global capital, a stark contrast between "real productivity" and "feeding off scraps of hype" is playing out.

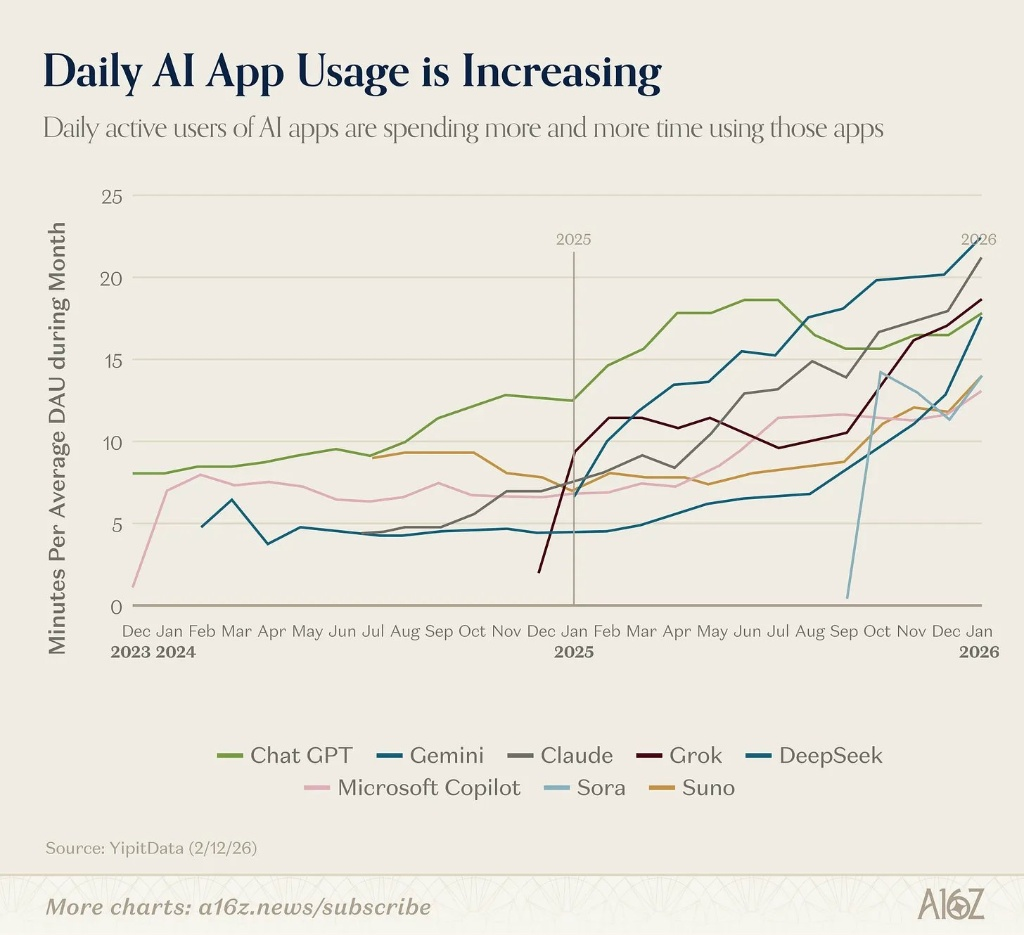

According to the latest data released by YipitData, the user stickiness of global core AI applications is experiencing a qualitative leap. The data curve intuitively reflects that not only are mainstream large models like ChatGPT, Claude, and Gemini showing a steep overall upward trend in average daily active user usage time (Minutes Per DAU), approaching or breaking the 20-minute mark; subsequent entrants like DeepSeek and the multimodal representative Sora have also shown an almost vertical explosive momentum. This proves that AI has indisputably embedded itself into the general public's real production workflows, with users investing tangible "time costs" into it.

On the other hand, what is even more terrifying is the iteration density and speed of generative multimodal models. From the industry release timeline over the past year, we can see that from Kling 2.0, Veo 3, Sora 2, to LTX 2.0, heavyweight visual and video models are undergoing arms-race-style upgrades almost every month. The consecutive releases of Kling 3.0 and Seedance 2.0 this month are the latest crystallization of this high-frequency technical iteration wave. Their breakthrough video generation capabilities have made traditional film and television industries, like Hollywood, feel substantial existential pressure.

Data Source: https://x.com/a16z/status/2024533996928209126

Regarding the recent news of humanoid robots performing perfectly synchronized Kung Fu moves and landing backflips on their knees without a single fall during the Chinese Spring Festival Gala—a showcase reaching a billion people—even mainstream Western media provided the following commentary:

Data Source: NBC News

-

Astonishing Iteration Speed and Pragmatism: CNBC stated bluntly in its report: "Who's laughing now?" Just over a year ago, some humanoid robots were still a laughingstock online for their staggering and clumsy movements; but today, they can perfectly execute complex physical actions. This engineering capability to bury one's head in frantic iteration instead of just spinning grand narratives is exactly what the current crypto space lacks the most.

-

From "Speculation Hype" to "Real Consumption": The robotics industry has, to some extent, moved past the stage of "telling stories" and "issuing pitch decks." Some manufacturers are actively delivering usable products to the market at highly competitive prices. Actual products have emerged, real sales data exists, and the public and enterprises are willing to spend money for "utility value" rather than buying in to "speculation for profit."

What crypto entrepreneurs should ponder deeply is the pragmatic path taken by these star AI and robotics teams:

-

Deepening their own advantages, refusing blind trend-following and overreach: Seedance did not attempt to challenge AlphaFold's position in the field of biological protein folding. Instead, relying on the ecological resources of its backer, the video content giant ByteDance, it pushed the "video generation" vertical to the extreme, even causing panic in Hollywood.

-

Not building "pseudo-infrastructure," focusing on niche scenarios: Consumer-grade AI applications like Manus and Character AI did not obsess over being "OpenAI killers" or attempt to "reconstruct underlying computing networks." They astutely captured long-tail demands in niche scenarios, building customized services and applications based on existing large model capabilities. This seemingly "not grand/low-level enough" route has brought them healthy, impressive real revenue and user retention, as well as considerable primary market valuations.

Looking back at the recent crypto market, at the crossroads where it intersects with AI concepts, we see more narrative stagnation, or even regression. Previously, the emergence of GOAT at least carried a layer of experimental interest as an "AI-autonomously issued Meme" (although similar concepts were explored as early as the TURBO project during the initial launch of GPT-4 in 2023). However, the recent OpenClaw scam has thoroughly exposed the crypto circle's dilemma amidst the AI wave—the so-called "AI concept" is degenerating into a fig leaf for concept-skirting, vaporware hype, and Ponzi schemes. While the AI and robotics developers next door are working day and night to drive a productivity explosion, they simply have no time for, and even instinctively repel, such crypto hype.

Furthermore, the grand rhetoric repeatedly chewed over within the industry, such as the "decentralized computing revolution" and "AI inevitably needs Crypto to solve trust issues," is appearing increasingly pale and far-fetched in the face of the absolute power of centralized AI computing and the exponential leaps in model capabilities. If the crypto market in the future only focuses on finding token-issuing gimmicks in the "leftovers" of the technological revolution, it is doomed to fail in earning the respect of the mainstream tech world and long-term capital.

As market observers and long-term companions of the crypto industry, we fully understand the anxiety and pessimism brought by the current sideways market, but it is precisely at this moment that clear strategic focus is needed. We hope that future Web3 entrepreneurs can learn lessons from the evolutionary history of AI and robotics:

-

Distinguish between "Technical Daydreaming" and "True Value Reconstruction": The crypto industry certainly possesses the capability to reconstruct traditional foundations. Stablecoins essentially challenging and participating in the reconstruction of the SWIFT cross-border payment system is the best proof, as it practically solves the real pain points of high friction, low efficiency, and high thresholds in traditional finance. However, we still need to be wary of the technical delusion of "decentralization for the sake of decentralization." In the mature business world, infrastructure like Amazon Web Services (AWS) and Cloudflare are already extremely efficient. Unless you truly have an absolutely crushing technical barrier (e.g., a technological explosion) in the underlying architecture, true disruption comes from filling rigid demand gaps or providing a "10x better" user experience, rather than tearing down highly efficient existing systems without any commercial basis.

-

Serve even one "Real, Small Demand" well: Abandon the self-indulgent carnival of pseudo-demands. Get down to earth and solve the pain points of a small circle, focus on real applications that can run actual businesses (such as empowering AI agent payments, optimizing cross-border settlements, etc.), and refocus on the long-unmentioned "Real Protocol Revenue" (Real Yield). This is far more pragmatic than churning out another 10,000-word whitepaper attempting to "disrupt OpenAI with a decentralized network." Only by doing so is it more likely to stand out in this round of capital reshuffling and gain true market recognition.

2. Weekly Selected Market Signals

Tariff and geopolitical uncertainty weigh on markets; risk assets struggle while safe havens rally

President Trump’s tariff agenda resurfaced as a key market catalyst last week, and investors’ first instinct was to “reach for safety.” In early Asian trading on Monday, spot gold surged on renewed safe-haven demand, briefly pushing up to around $5,170/oz; silver also strengthened, with gains accelerating. The U.S. dollar softened while the yen firmed, pulling USD/JPY back toward the 154 level. Asia-Pacific equities were mixed but broadly resilient (Japan was closed for a holiday and liquidity was thinner in parts of the region). Oil prices swung between geopolitical concerns and growth anxiety, with WTI hovering around $65–66/bbl.

The core driver of volatility remains policy uncertainty. On February 20, the U.S. Supreme Court ruled 6–3 that the sweeping tariffs previously imposed under IEEPA (the International Emergency Economic Powers Act) exceeded presidential authority, finding that the statute does not empower tariffs in that manner. However, the ruling did not remove uncertainty. The White House subsequently announced that Trump would invoke Section 122 of the Trade Act of 1974 to introduce a 10% temporary import surcharge for 150 days, scheduled to take effect at 00:01 ET on February 24. Shortly thereafter, Trump stated that the “global tariff” rate would be raised from 10% to 15%, pushing markets back into a “policy reversals → higher risk premia” pricing regime. Trade policy without clear boundaries or stable guidance tends to suppress corporate investment appetite and broader risk-taking, keeping cross-asset volatility elevated for longer.

Even so, U.S. equities did not fall in a straight line. After the Supreme Court decision, the major indices closed higher on Friday, with the S&P 500 up about 0.69% on the day. That “relief first, concerns later” pattern underscores the market’s ambivalence. Investors welcomed the possibility that reduced tariff uncertainty could help margins, yet the macro backdrop remains mixed: preliminary U.S. Commerce Department data showed Q4 2025 GDP growth slowing to 1.4% (annualized), while the Fed’s preferred inflation gauges (PCE-related measures) suggested a pickup in price pressures in December. The 10-year U.S. Treasury yield drifted back toward ~4.08% amid choppy trading. In addition, worries that tariff reversals could trigger refunds and widen fiscal shortfalls have further amplified discussions around a higher risk premium for U.S. assets.

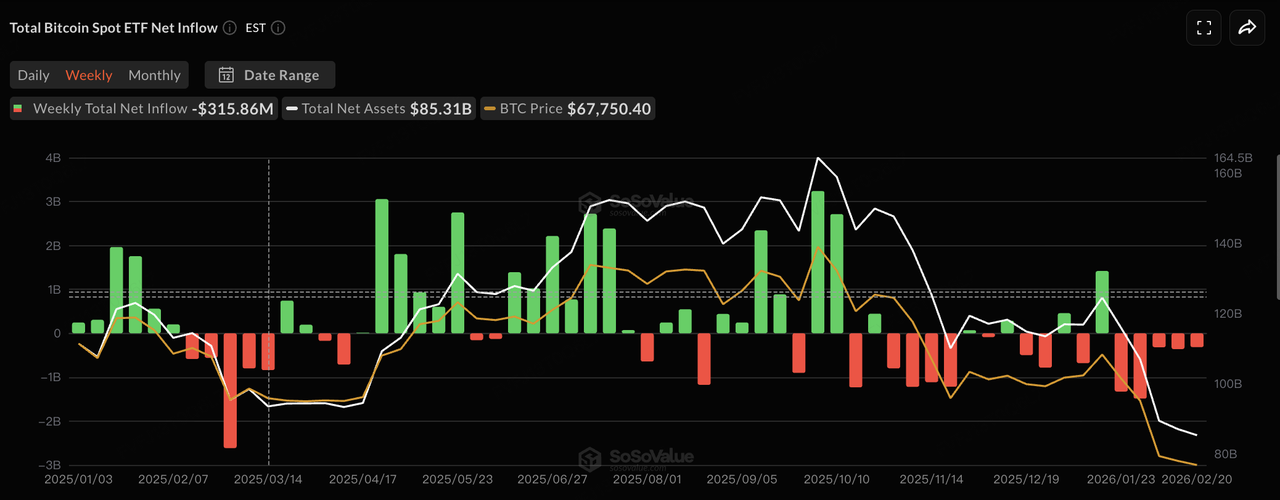

Data Source: TradingView

Meanwhile, sentiment in the crypto market remained fragile. Bitcoin spent last week oscillating between $65k–$70k, and as risk appetite softened again from the weekend into Monday’s Asia session, BTC briefly dipped below $65,000 (around $64,700). On the industry side, miners’ “cash-flow first” stance is increasingly notable. Bitdeer (BTDR) disclosed that as of 2/20 its corporate BTC holdings (excluding customer deposits) had fallen to zero, and that it sold all 189.8 BTC mined during the week while reducing reserves by 943.1 BTC on a net basis. With BTC off its year-to-date highs and mining profitability under pressure, Bitdeer has also been advancing fundraising and AI/HPC expansion plans. The combination of “aggressive coin sales + shifting capex toward AI” has sparked visible debate among miners, public-market investors, and the broader crypto community over its balance-sheet strategy.

Data Source: SoSoValue

ETF flows remain a weak spot. U.S. spot BTC ETFs have recorded five consecutive weeks of net outflows, suggesting institutional activity is still characterized more by tactical de-risking than sustained accumulation. As of last week, total spot BTC ETF net assets were roughly $85.31B. Ethereum is in a similar “weak flows—weak price” feedback loop: based on SoSoValue’s figures, as of 2/20 (ET), spot ETH ETF net assets stood at about $11.141B, with flows remaining choppy.

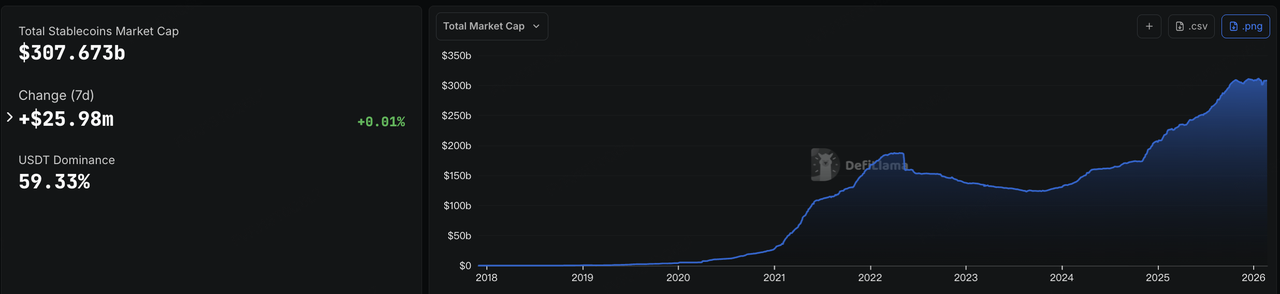

Data Source: DeFillama

On-chain liquidity has been relatively steady. Overall stablecoin market capitalization has continued to edge higher through February, and supply in regulated stablecoins such as USDC has shown marginal improvement. This looks consistent with a “risk-off parking trade,” where some capital stays on-chain in stablecoins while waiting to redeploy. The key question from here is whether these stablecoins continue to sit within on-chain venues (DEX/DeFi/on-chain payments) or rotate back to exchanges—either to translate into more direct buying power or to signal rising redemption pressure.

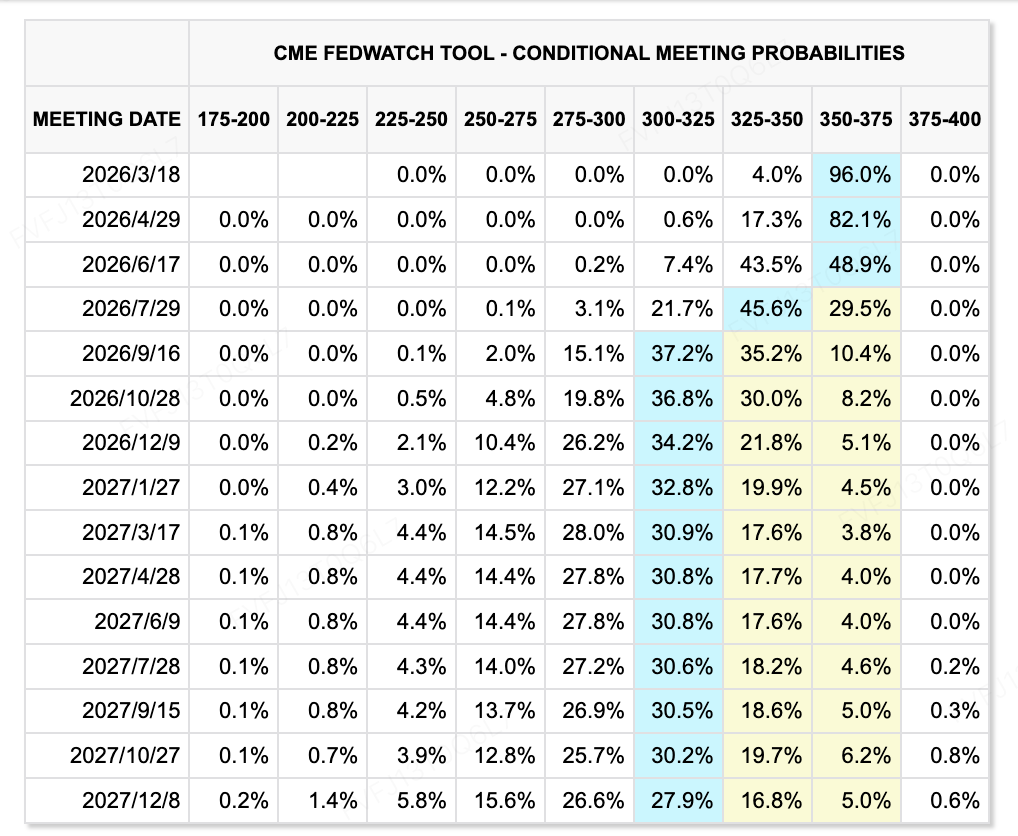

Data Source: CME FedWatch Tool

Rate expectations have not fully shifted away from the baseline view of two cuts before year-end, but the market has clearly pushed out the timing of the first cut. With growth data cooling while inflation prints remain relatively sticky, probabilities for earlier windows (e.g., June) have eased, and pricing increasingly points to July as the first realistic “decision point” to watch.

Key Events to Watch This Week:

Looking ahead, macro markets will face another “Trump moment,” while the AI complex is likely to re-anchor around NVIDIA earnings. Geopolitics could also reintroduce volatility around key dates: the third round of U.S.–Iran nuclear talks is scheduled in Geneva this week, and February 24 also marks one of the symbolic milestones around the Russia–Ukraine conflict (its fourth anniversary).

-

Feb 24: Trump delivers the State of the Union address; the White House’s temporary import surcharge (10%, 150 days) is scheduled to take effect (00:01 ET).

-

Feb 24: Apple holds its 2026 annual shareholders meeting; markets continue to track its AI strategy and on-device execution pace.

-

Feb 25 (after market close, ET): NVIDIA FY26 Q4 earnings and conference call—likely to influence risk appetite across the AI supply chain again.

-

Feb 26: U.S. Durable Goods Orders (January preliminary).

-

Feb 27: U.S. PPI (January).

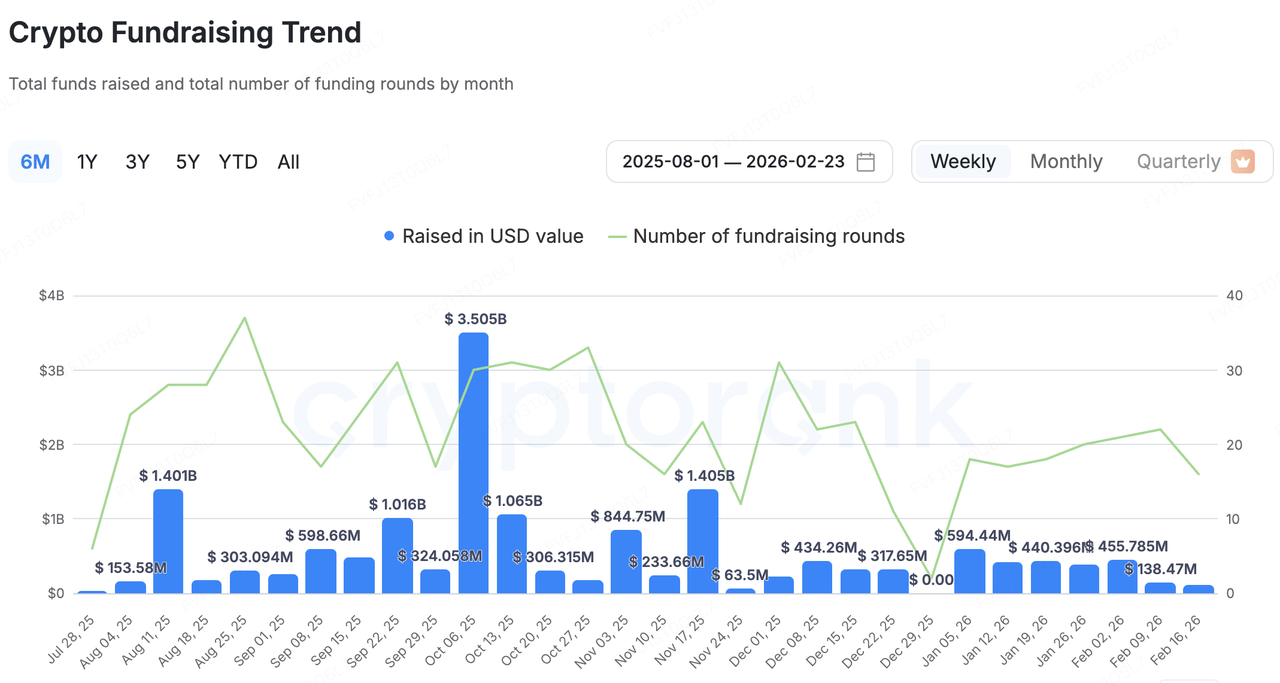

Primary Market Financing Observation:

Primary funding remained subdued last week, but structurally it felt more like “headline deals without broad-based inflows.” Deal count was not particularly low, yet most of the weekly total was driven by a small number of large rounds. At the same time, overall sentiment stayed cautious, and capital continued to gravitate toward projects with clearer growth levers, compliance pathways, or more deterministic business models—an increasingly visible “more selective, more concentrated” pattern in broader industry funding (notably in AI application deployment, fintech/compliance, and RWA-related infrastructure).

Data Source: CryptoRank

Under CryptoRank’s dataset, disclosed fundraising totaled $112.2M across 16 rounds for the week. The largest deal—Novig’s $75M—accounted for roughly 67% of the weekly amount. In other words, excluding the top transaction, remaining rounds were generally small, and the market’s “distributed narratives” did not translate into a meaningful improvement in funding conditions; weekly totals were largely supported by a handful of outsized checks.

Novig: In a market where Kalshi already holds an advantage in sports, Novig targets user migration via “zero retail fees + institutional monetization”

Novig raised a $75M Series B (led by Pantera) at an estimated ~$500M valuation. Importantly, Novig is not “discovering a new category.” Instead, it is entering a mature competitive landscape in which Kalshi already commands scale in sports-related contracts and holds CFTC DCM status (Kalshi received DCM designation in 2020). Novig’s bet is that stronger retail-facing product design and a more aggressive pricing proposition can unlock migration at the margin.

The most meaningful differentiation is retail experience and fee structure. Kalshi operates like a conventional exchange and charges trading fees (with a published fee schedule). Novig positions itself as a P2P order-book platform for sports traders, emphasizing commission-free retail trading / no traditional sportsbook “vig,” while monetizing more through fees charged to institutional participants. This “shift the cost burden from retail to the institutional side” is its most direct, easily perceived point of differentiation versus Kalshi. Novig’s branding and product language are also more explicitly “sports-native”—closer to rebuilding a sportsbook experience with exchange-style pricing rather than treating sports as just one category within a broader event-contract marketplace.

Risks are equally concentrated. First, DCM status is not a universal shield—even as a DCM, Kalshi has faced strong pushback at the state level (e.g., Nevada’s lawsuit seeking to stop sports-related contracts for state residents), implying Novig could encounter similar friction even if it progresses toward federal compliance. Second, Novig is still in a transition phase from a sweepstakes-style dual-currency framework toward a clearer regulatory identity; stability in compliance, payments, and risk controls will directly affect expansion speed. Third, sports trading ultimately becomes a liquidity and pricing game. With Kalshi’s head start and scale advantage, Novig will need verifiable depth and retention metrics to prove that “zero retail fees” can generate a durable liquidity flywheel; otherwise, rising acquisition costs and adverse retail experience against sophisticated counterparties could become binding constraints.

About KuCoin Ventures

KuCoin Ventures, is the leading investment arm of KuCoin Exchange, which is a leading global crypto platform built on trust, serving over 40 million users across 200+ countries and regions. Aiming to invest in the most disruptive crypto and blockchain projects of the Web 3.0 era, KuCoin Ventures supports crypto and Web 3.0 builders both financially and strategically with deep insights and global resources.

As a community-friendly and research-driven investor, KuCoin Ventures works closely with portfolio projects throughout the entire life cycle, with a focus on Web3.0 infrastructures, AI, Consumer App, DeFi and PayFi.

Disclaimer This general market information, possibly from third-party, commercial, or sponsored sources, is not financial or investment advice, an offer, solicitation, or guarantee. We disclaim liability for its accuracy, completeness, reliability, and any resulting losses. Investments/trading are risky; past performance doesn’t guarantee future results. Users should research, judge prudently, and take full responsibility.